News

The New Delta: Egypt’s Expansion and the Italian Response

Under the New Delta Project (see previous coverage from August 2024), Egypt is developing a 112-kilometer artificial waterway to irrigate more than one million hectares of reclaimed desert. This system relies on advanced water treatment and reuse technology to sustain vast new tracts of arable land. Planned cultivation includes wheat, corn, and sugar beets, with industrial tomatoes emerging as a primary export-oriented crop.

With this project, the Egyptian government has two stated objectives: to increase the country’s food self-sufficiency and to strengthen exports to Europe, the Middle East, and Africa.

More recently, huge investments have been made by several Egyptian and foreign tomato processors:

- Balkan Agricultural, based in Bulgaria where it has one factory, is opening its massive €20M “golden license” factory, designed to process 350,000 to 400,000 tonnes of tomatoes annually, aiming for an output of 70,000 tonnes of paste, in 6th of October City by March 2026

- MAFI for Food Industries, an Egyptian-Emirati joint venture that is currently completing a massive $180 million (USD) agro-industrial complex in Sadat City (strategically positioned near the New Delta farmlands). It features five advanced factories on a 157,000 m² site to process tomato paste, citrus, and frozen fruits (IQF). Their primary tomato processing line fromCFT will be able to run at 60 tonnes per hour from June this year, with the target of processing 38,000 tonnes of tomatoes in 2026. Their aim is to use state-of-the-art Italian and European technology (AI-driven automation) to produce high-quality paste that meets EU standards but at a much lower production cost. Unlike older Egyptian firms that serve the domestic market, MAFI is 100% export-oriented. They are specifically targeting the B2B market in Europe, positioning themselves as a “seamless” alternative for European food brands. Their aim is to integrate agricultural production from 2027.

- Karry Food Industries, a major Saudi-backed investment in Egypt. They have a 50,000 m² facility in Sadat City. They recently partnered with CFT to install high-capacity tomato paste and fruit puree lines. Karry own their own lands in Al-Hammam and the West Delta (the heart of the New Delta project). They control the entire chain: seeds → cultivation → processing → export.

- Paste & Juice (P&J): while an established name, P&J has undergone a massive expansion to coincide with the New Delta’s irrigation phase. They recently doubled their capacity from 1,000 to 2,000 tonnes of fresh tomatoes per day. They utilize a “Traceability System” that tracks tomatoes from the reclaimed desert lands directly to the aseptic bag, satisfying the transparency requirements of major EU retailers. P&J already represents about 45% of Egypt’s total tomato paste production and export 95% of what they make.

- Sekem Group (via their ISIS organic brand) is working on reclaiming 50,000 hectares of desert through biodynamic farming. While Italy has historically held the “Premium Organic” tomato market, Sekem aims to prove that high-quality, sustainable tomato products can be grown in the Egyptian desert, directly threatening Italy’s “quality-over-quantity” defense.

While the “New Delta” marks a significant leap in Egyptian industrial capacity, the rapid expansion has prompted a strategic response from Italy.

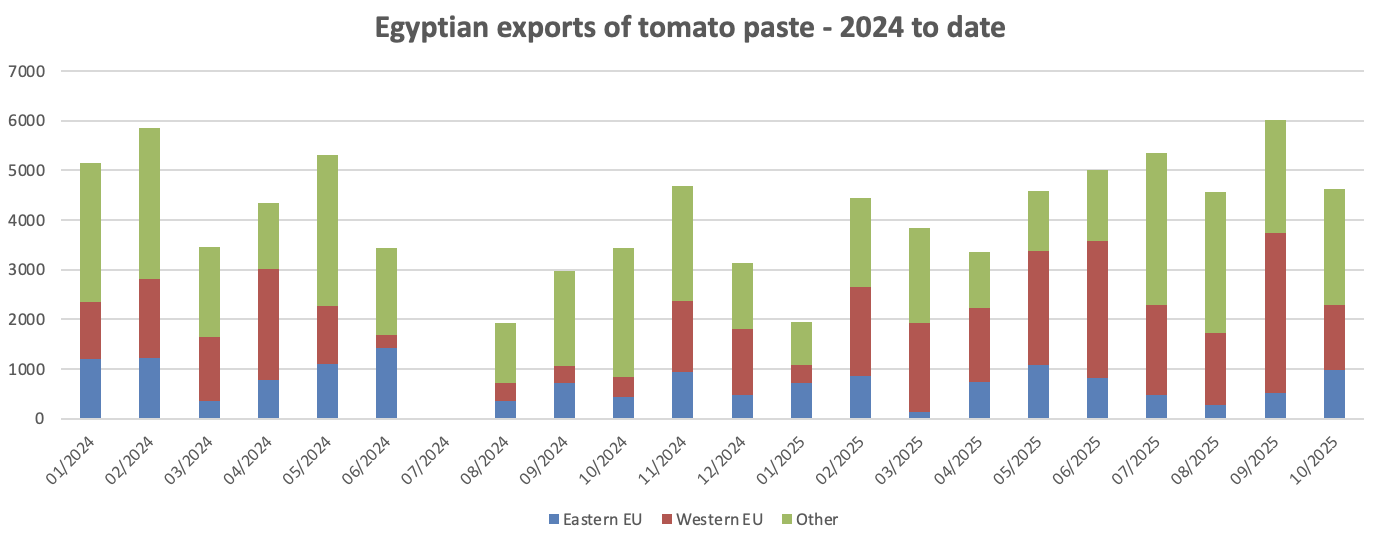

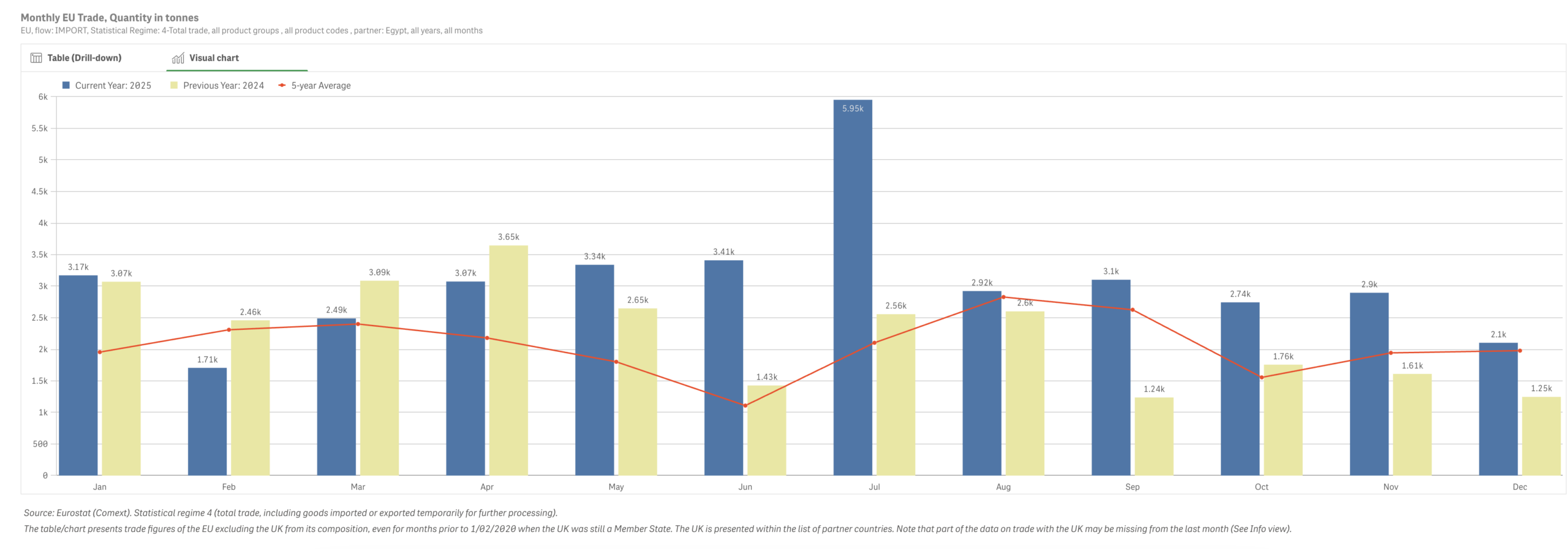

Eurostat data indicates a sharp shift in market dynamics: exports of processed tomato products from Egypt to the EU surged by 88% in the final six months of 2025. This growth is expected to accelerate as the one-million-hectare New Delta project moves toward full export capacity.

Italian stakeholders have identified several areas of “standard divergence” that complicate the competitive landscape:

- Environmental Standards: Producers highlight a lack of trade reciprocity. While Italy adheres to strict EU pesticide bans (such as Mancozeb and Chlorpyrifos), reports of these residues in imported finished products have raised phytosanitary concerns.

- Labor and Social Oversight: Significant differences exist in labor costs and oversight. The Italian industry operates under rigid EU social contracts, while the rapid expansion in Egypt has faced international scrutiny regarding informal labor and wage transparency.

- Production Parity: The lower cost-base in Egypt, facilitated by large-scale government-backed infrastructure, creates a pricing gap that challenges high-compliance European manufacturers.

In response, Italian industry bodies are advocating for universal standards within the EU Single Market. The objective is to ensure that all international competitors are held to the same safety, social, and environmental benchmarks as domestic producers, preserving the integrity of the “Made in Italy” supply chain in an increasingly globalized market.

Additional information: Egyptian exports (in Tonnes) – Source: TDM

European imports from Egypt (in Tonnes) – Source: Eurostat

Sources: Food Business EMEA, SIS Egypt, Karry, CFT, Paste & Juice, MAFI, Il Giornale

{kind=link}