News

The 2026 Argentine processing tomato season concluded with a complex mix of exceptional field performance and acute macroeconomic pressures. While the sector achieved record-breaking yields and superior fruit quality, it contracted in scale due to aggressive global competition, changing government economic policies, and a heavy marketplace overstock.

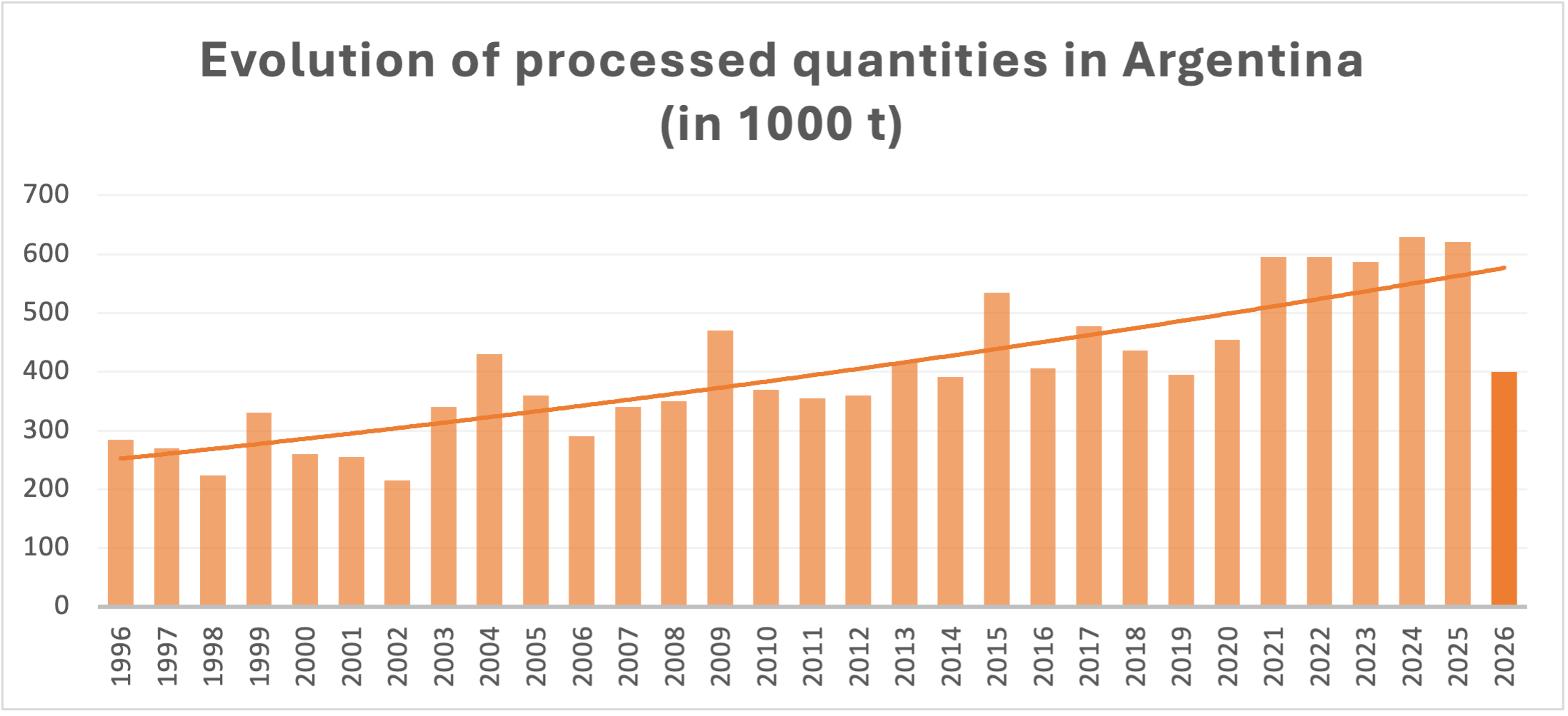

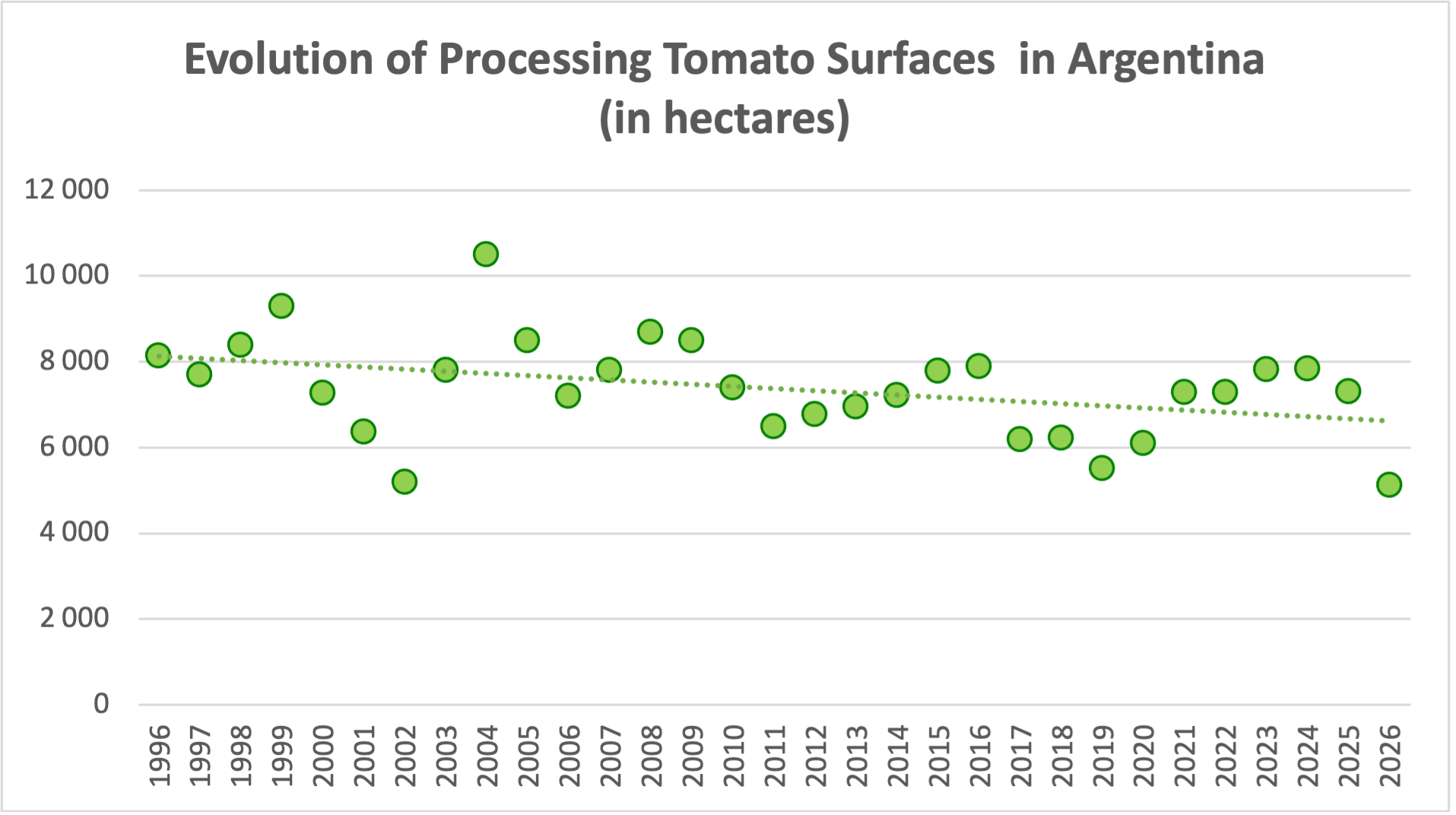

The harvest started mid-December and ended at the ended of April with a final national production currently estimated to be close to 400,000 tonnes, from approximately 5,120 hectares. This is a major reduction from the 620,250 tonnes processed in 2025, and the 550,000 tonnes from 6,000 hectares expected in October 2025.

While yields performed strongly in several key regions, lower-than-normal productivity in parts of Northern Argentina, mainly associated with crop management limitations, reduced the overall national output potential.

San Juan once again delivered an exceptional season, achieving record average yields for the second consecutive year. The province confirmed its position as the country’s highest-performing processing tomato region, supported by very favourable climatic conditions, strong technical management, and excellent crop uniformity. San Juan achieved record commercial yields for the second consecutive year, with averages exceeding 120 t/ha and top-performing fields reaching 200 t/ha.

Mendoza, under cooler growing conditions and with a later production cycle, achieved generally normal yield levels averaging 91 t/ha, with satisfactory crop performance and good fruit quality throughout the harvest period.

The growing cycle was characterized by hot, dry, and windy conditions. A mild preceding winter accelerated early-season pest pressure, though the dry summer suppressed major plant diseases. While severe mid-January hailstorms devastated roughly 400 hectares in Villa Aberastain (San Juan), the financial fallout was successfully mitigated by the Tomate 2000 program’s mutual solidarity hail fund.

The regional, cooperative framework of the Tomate 2000 program proved vital to the industry’s stability, commanding a record 68–69% share of total national output. Within the Tomate 2000 program, average yields reached a new record of 106 t/ha once again, mainly driven by the outstanding performance of San Juan, supported by solid results in Mendoza and the supervised production areas in La Rioja Province. The program continued to demonstrate higher productivity and greater yield stability compared to the broader national average. Fruit quality throughout the season was significantly better than during the previous campaign, with very satisfactory industrial performance observed across most production areas. Overall, the 2026 season evolved positively, combining strong yields in the main producing regions, improved fruit quality, and stable industrial supply conditions across most of the country.

This shows that the Tomate 2000 program further consolidates its strategic role within the Argentine processing tomato industry, continuing to represent a major share of the country’s total production and contributing decisively to national productive stability and overall crop performance.

Climate and pest management challenges are increasingly being addressed through a zonified production planning strategy. The regional structure of the Tomate 2000 program allows production to be distributed and coordinated according to the specific climatic and agronomic characteristics of each area, improving stability and reducing risk exposure.

Although hail events have been particularly severe during the last two campaigns, the mutual solidarity hail fund developed within the Tomate 2000 program has proven to be a very effective soft-risk management tool, helping growers remain financially and operationally within the system after major climatic events.

Mechanization levels continue to increase progressively across the sector. At the same time, the gradual normalization of energy tariffs is encouraging investments in renewable energy sources, especially solar energy. Significant efforts also continue to improve drip irrigation management and water-use efficiency.

The current economic framework implemented over the last two years has facilitated the importation of new technologies and agricultural equipment, improving access to innovation. However, financing remains limited and continues to be one of the main constraints for further modernization.

At the industrial level, current economic conditions are encouraging factories and marketing departments to focus more strongly on value-added products and product differentiation strategies. In parallel, energy tariff normalization is also creating incentives for investments in renewable energy solutions within processing facilities.

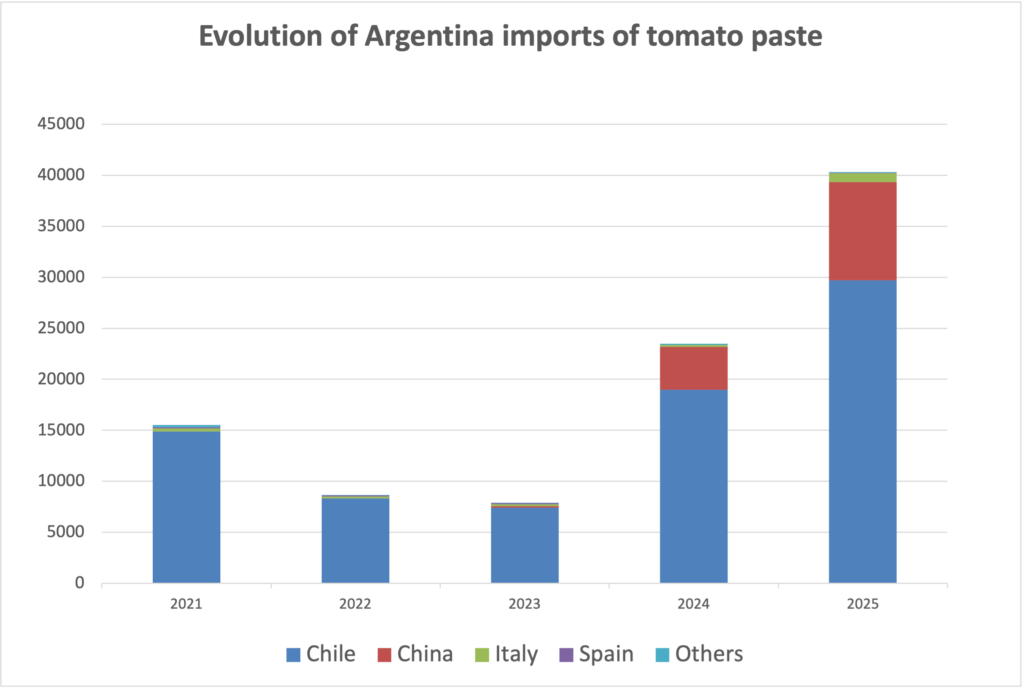

There is a strong competitive pressure from imported tomato paste, particularly from Chile and China. Back when the tonne of Chilean paste was at 1.400 dollars or so it was worth it to grow the tomatoes locally, but since the price has been around 1.080 it is cheaper for the factories to import processed tomatoes. Argentina is not very efficient at the moment for processing tomatoes and still has a very high tax structure.

The Argentine peso currently remains relatively strong and stable, and this is expected to continue over the long term due to increasing foreign currency inflows from major export sectors such as grain production, oil and gas developments (particularly Vaca Muerta), and mining activities, which are projected to become major sources of national income over the next decade.

Commercially, inventories throughout the supply chain have started to move more actively, including factory stocks, although consumption recovery remains relatively slow. Domestic retail tomato products currently remain more competitive than imported finished products, and the economy is undergoing a gradual corrective deflationary process aimed at stimulating consumption.

The recent approval of the RIGI (Large Investment Incentive Regime) by the national government is being perceived as a major structural signal aimed at attracting long-term investment into Argentina. The regime offers significant fiscal, customs, regulatory, and foreign-exchange stability incentives for large-scale productive projects, particularly in sectors such as energy, mining, infrastructure, and industrial development. Although its direct impact on the processing tomato sector may still be limited in the short term, it is helping improve investor confidence and encouraging a more stable environment for technological modernization, energy projects, and productive expansion.

In parallel to the RIGI framework, smaller-scale investment incentive programs for SMEs are also beginning to emerge, seeking to facilitate modernization and competitiveness for regional industries and medium-sized productive operations. At the same time, new labour flexibility reforms introduced by the national government aim to reduce labour-related costs, simplify hiring conditions, and improve operational competitiveness. Together, these measures are being interpreted by the productive sector as part of a broader transition toward a more investment-oriented and efficiency-driven economic framework.

Although production costs remain relatively high under the current exchange-rate conditions, the present macroeconomic environment provides greater stability and predictability, allowing better long-term planning for both growers and processors.

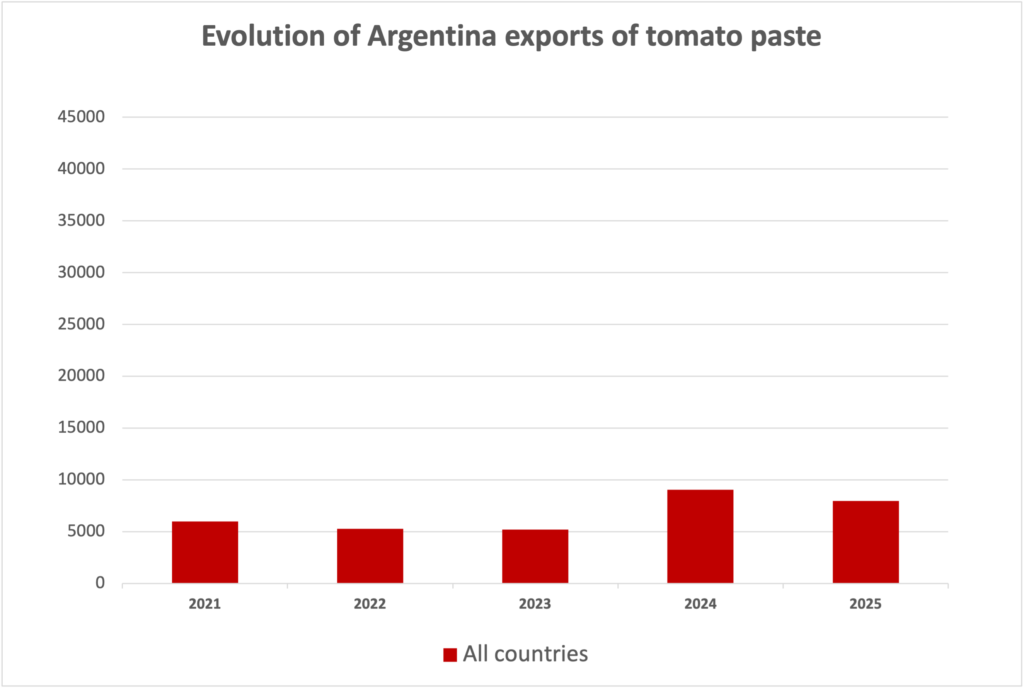

In this context, improving efficiency, reducing production costs, and maximizing productivity per kilogram processed will continue to be key strategic factors for the competitiveness of the Argentine processing tomato sector in the coming years. For the next season, it will depend greatly on the price of Chilean paste. If the price stays so low, the production level will probably remain low around 400.000 tonnes, but if it goes back up the factories will have incentive to contract more growers. The internal consumption is around 650.000 tonnes so Argentina should remain a net importer for the time being.

Sources: WPTC, Tomate 2000

{kind=link}