News

ANICAV: Italy’s 2025 Export in slight decline

Italy is confirmed as world’s leading exporter of canned tomatoes but 2025 exports which reached €2.8 billion are down from the previous year (-8% in value and -2% in volume)

Anicav: “the first decline in 10 years is driven by the geopolitical situation and competition from countries that do not guarantee our quality standards”

General Manager Giovanni De Angelis: “The Made in Italy brand remains a clear added value, but in the long run, price pressure risks undermining our presence in international markets. A cohesive supply chain is essential to remain competitive.”

On the occasion of the third edition of National Made in Italy Day, ANICAV (the National Association of Canned Vegetable Industries) takes stock of the exports of one of the flagship products of Italian agri-food production. Historically a symbol of Italian identity, our canned tomatoes have followed the migration flows of our compatriots to reach every corner of the globe.

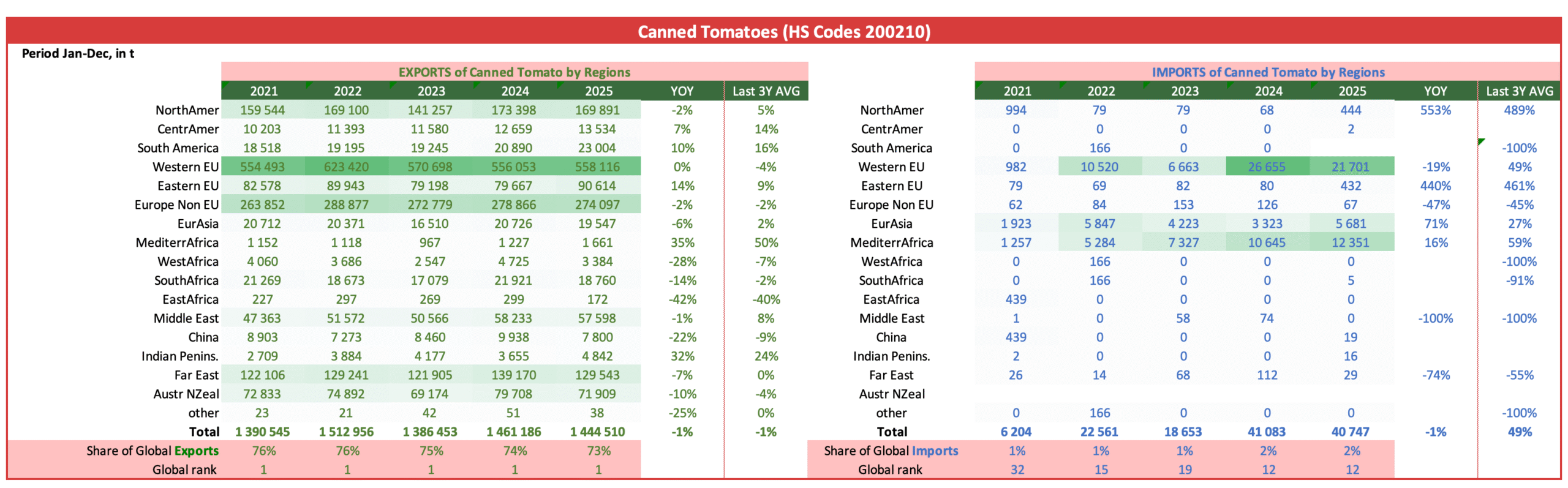

Italy remains the world’s leading exporter of canned tomatoes; however, the latest figures present a significantly less positive outlook than in recent years. In 2025, exports of all tomato derivatives recorded a decline in volume and, more notably, in value—dropping by 2% and approximately 8% respectively compared to 2024. This represents over 2.2 million tons of canned products for a total value of €2.8 billion. The majority (over 64%) consists of peeled tomatoes, pulp, and cherry tomatoes—high value-added products that were hardest hit by U.S. tariffs (-7.1% in value).

Key Markets and Destinations

- Europe: Remains the primary reference point, accounting for over 60% of export value, led by Germany, the United Kingdom, and France.

- United States: Represents the leading non-European export market with a 7.5% share.

- Japan: Ranks as the sixth-largest market globally for “red” preserves and the second-largest outside of Europe, following the USA.

“For the first time in over 10 years, we are seeing a decrease in exports in both value and volume,” stated Marco Serafini, President of ANICAV. “The reasons lie in the international geopolitical situation, shaped by numerous conflicts, and the protectionist policies of certain countries, particularly the United States. Furthermore, we face growing unfair competition from entities that cannot guarantee our standards of quality, safety, and sustainability, yet continue to flood the market with low-cost products. This is why we continue to call on the EU to introduce reciprocity requirements.”

“Italy remains the world’s leading exporter of tomato derivatives, but we must reflect on the current shifts in the landscape,” continues Giovanni De Angelis, General Manager of ANICAV. “Our tomatoes have always been an emblem of Made in Italy and our world-renowned culinary tradition, yet they are now under heavy threat from international competition that relies solely on price leverage. The gap between the price of our products and those of our competitors continues to widen, jeopardizing significant market shares that our entrepreneurs have secured over the years.”

“We simply cannot afford to lose further ground in terms of competitiveness. To prevent this, we need cohesion and dialogue among all stakeholders in the supply chain—especially as we approach a harvest season that promises to be extremely complex. The major unknown remains energy costs, which threaten to send production costs skyrocketing once again.”

Additional Information from our updated Country Profile on Italy (click HERE to see the whole profile)

The 2025 trade data for Canned Tomatoes confirms Italy’s unrivaled position as the global benchmark for the sector, with the country maintaining a dominant 73.4% share of world exports. Despite a complex agricultural campaign characterized by significant regional disparities, the Italian industry demonstrated remarkable resilience in international markets. This stability in export volume—which saw only a marginal year-over-year dip of 1% to 1.40 million tonnes—is particularly notable when viewed against the backdrop of a challenging production year.

A significant strategic shift is also visible in the geographical distribution of these exports. While traditional strongholds in the Western EU and North America remained steady, a robust 14% year-over-year growth was recorded in Eastern EU markets. This trend suggests a successful deepening of market penetration in emerging European economies, which has effectively offset a 7% decline in the Far East. Furthermore, the continued rise in imports from the Western EU, which shows a 49% three-year average growth, reflects a sophisticated industrial strategy. Italian processors appear to be managing a global inventory to balance domestic demand, ensuring that premium, 100% Italian-grown production is prioritized for the highest-value international markets.

Ultimately, the 2025 figures underscore a successful transition from volume-driven growth to a model of value-preservation. Canned tomatoes remain the cornerstone of the Italian trade balance, contributing heavily to the record $3.31 billion total sector value. By maintaining its #1 global rank and commanding a premium price point despite global inflationary pressures, the Italian industry has proven that the “Made in Italy” label remains an indispensable staple for global consumers, even in a climate of economic and environmental volatility.

Sources: ANICAV, TDM

{kind=link}