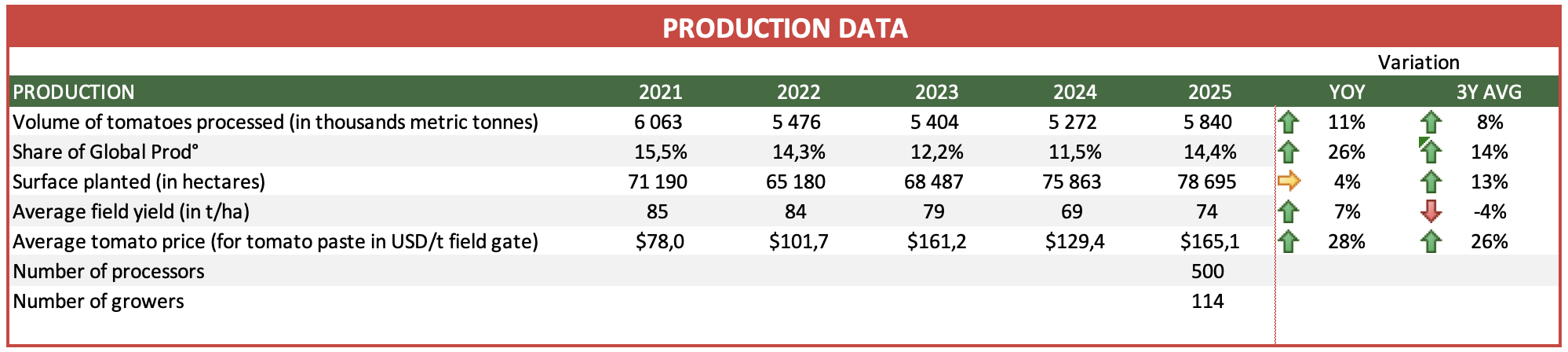

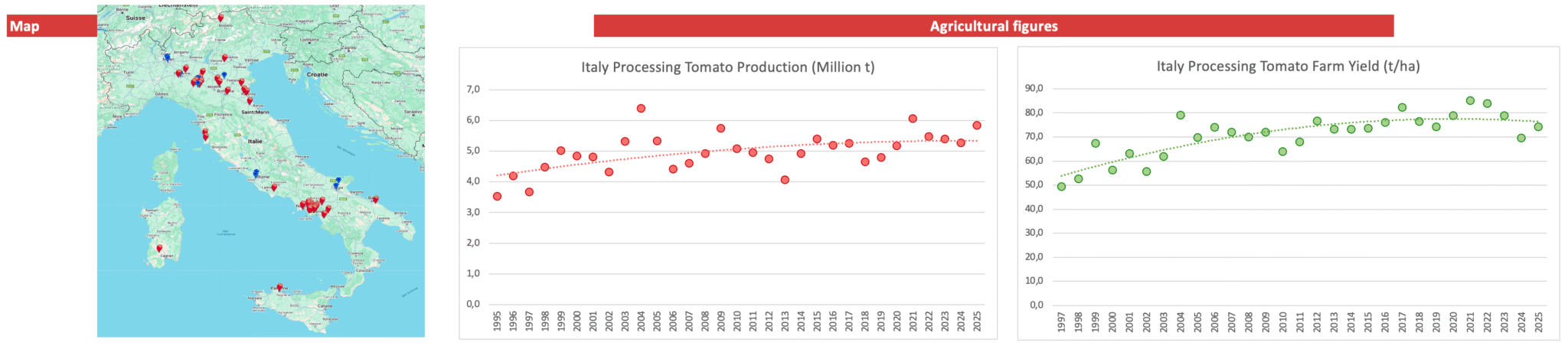

Italy processes over 5 million tonnes of tomatoes annually, making it Europe’s largest and the world’s second or third-largest processor.

Approximately half of the total production is grown in Northern Italy, mainly around Parma, Piacenza, Ferrara, and smaller zones north of the Po River. In this area, about 36 thousand hectares of tomatoes for processing are cultivated every year with the involvement of about 2 thousand agricultural producers (grouped in 13 producer organisations) and 25 processing plants (belonging to 20 different companies) for the processing of about 2.5 million tonnes of tomatoes from which mainly concentrates, pulps and purees are produced. The climate is generally favourable, with strong day-night temperature differences enhancing fruit colour but risks include drought, hailstorms, and heavy rains which can reduce production as happened in 2024. Production is fully mechanized and with drip irrigation with yields averaging 75 t/ha. The whole production is either integrated (90%) or organic (10%) with a strong interprofessional organization, OI Pomodoro da Industria Nord Italia, assisting the growers and processors. About a third of the volume is processed into tomato paste, a quarter into passata, with a whole range of other products, either directly into final packaging or in bulk.

The Centre and South of the country account for the over half of national production, with Puglia alone contributing 40%. In this area, about 34 thousand hectares of tomato are cultivated with the involvement of 20 producer organizations and 43 processing companies for the processing of about 2.8 million tonnes of tomatoes. The main production zone is around Foggia, where tomatoes are grown for paste and canned peeled tomatoes processed mainly in the Campania region, south of Napoli. The region is favourable for tomato production but can experience extreme climate conditions with some spring frost, hot summers with little rain, and strong winds that reduce disease but increase water demand, and there are now more frequent issues with water-use restrictions. Farms vary in size, from small 2-3 ha plots to large 100+ ha farms where yields can exceed 100 t/ha, while they are averaging 90 t/ha. Over 90% of the harvest is mechanized, with manual harvesting remaining mainly in Campania for San Marzano tomato protected origin label. The companies in the South of the country are mostly specialised in the production of tomato products in small packaging, directly intended for retail sales, including the traditional wholepeel tomatoes (over 30% of the volume), but also other canned tomatoes, passata and tomato paste.

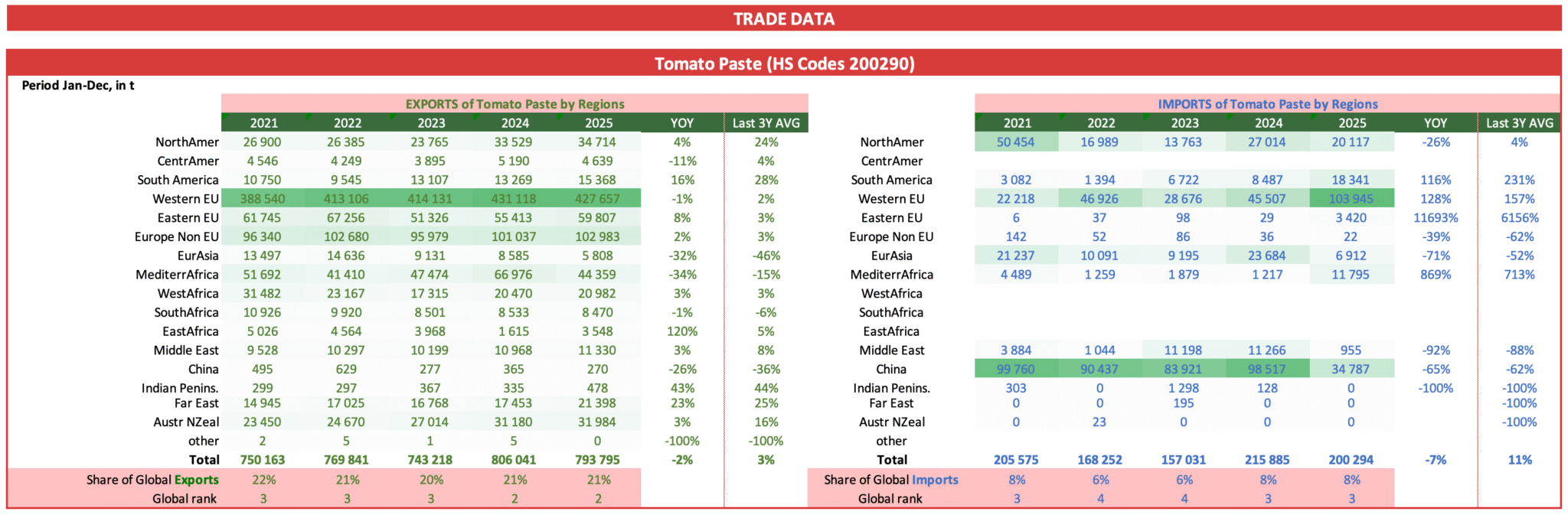

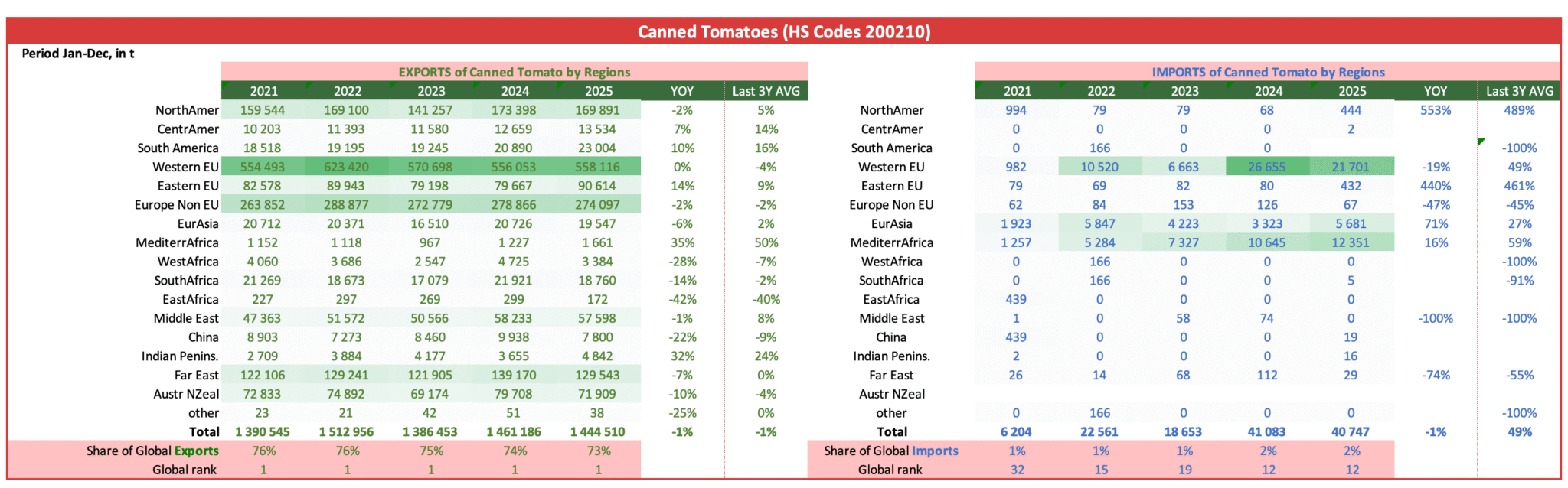

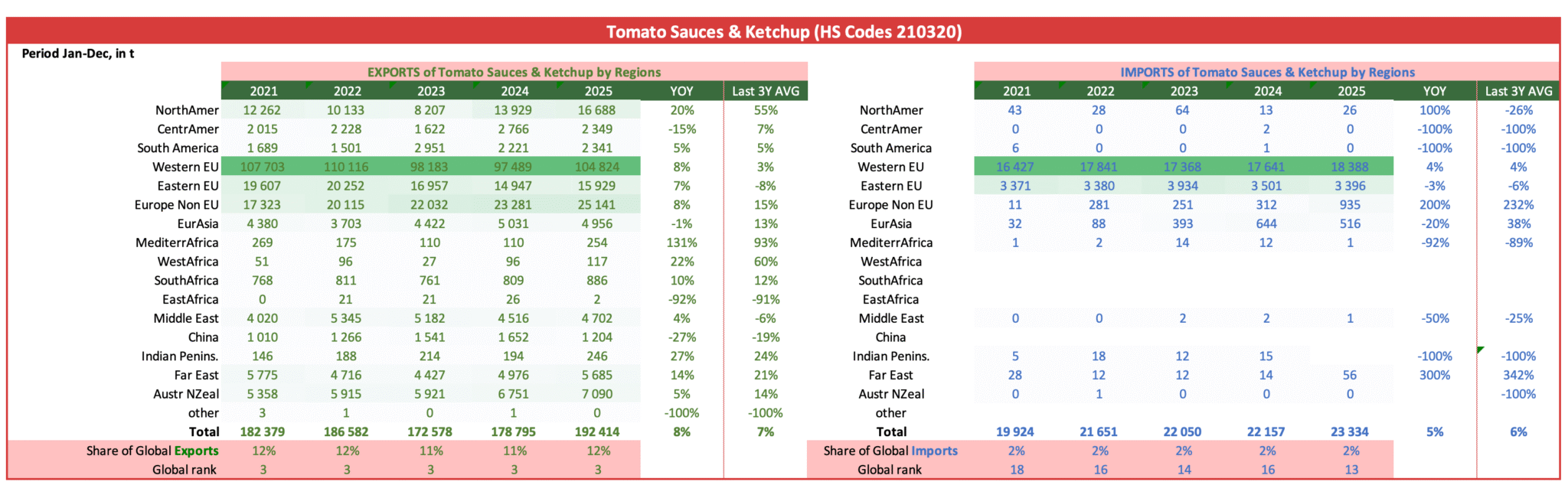

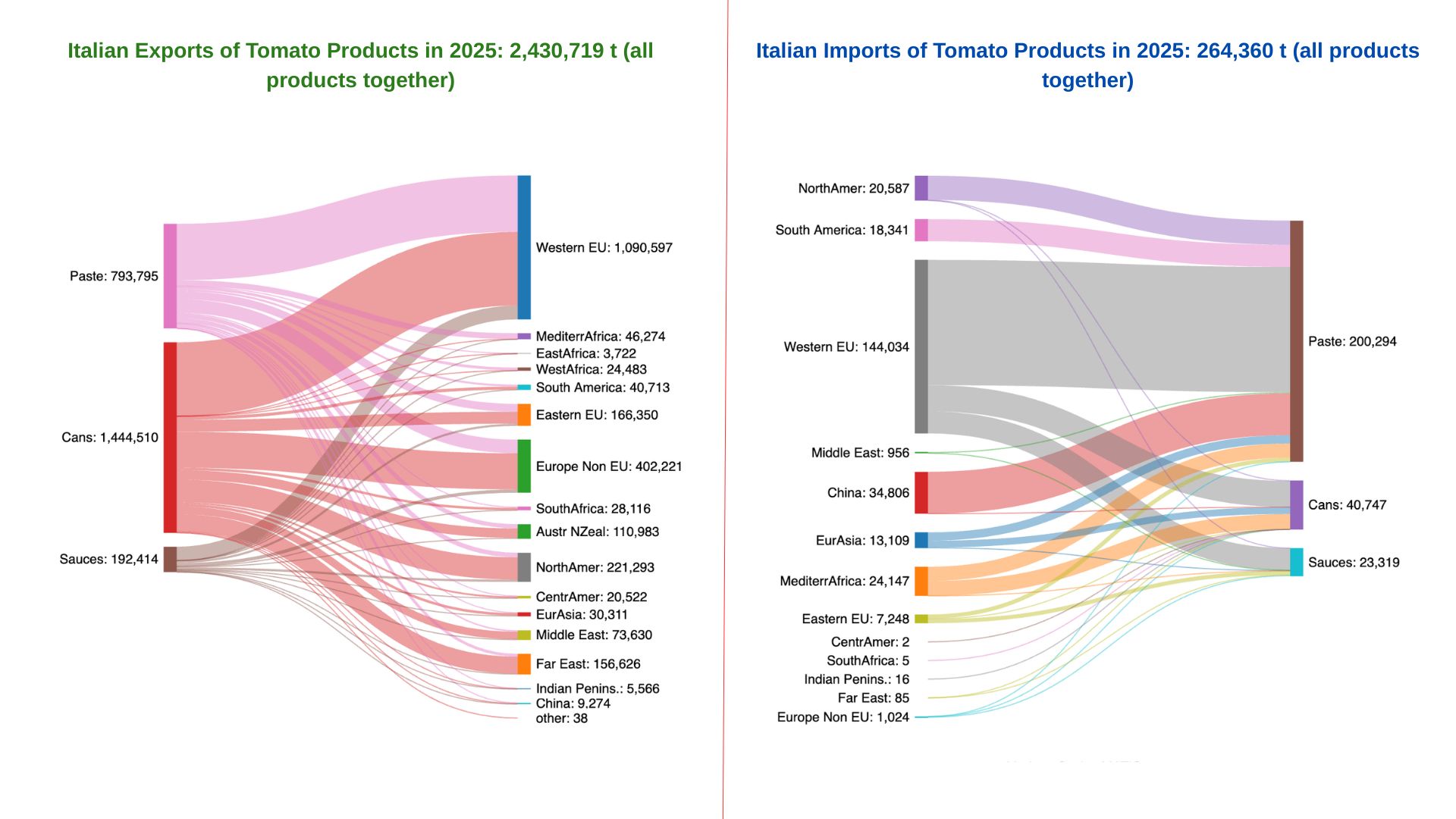

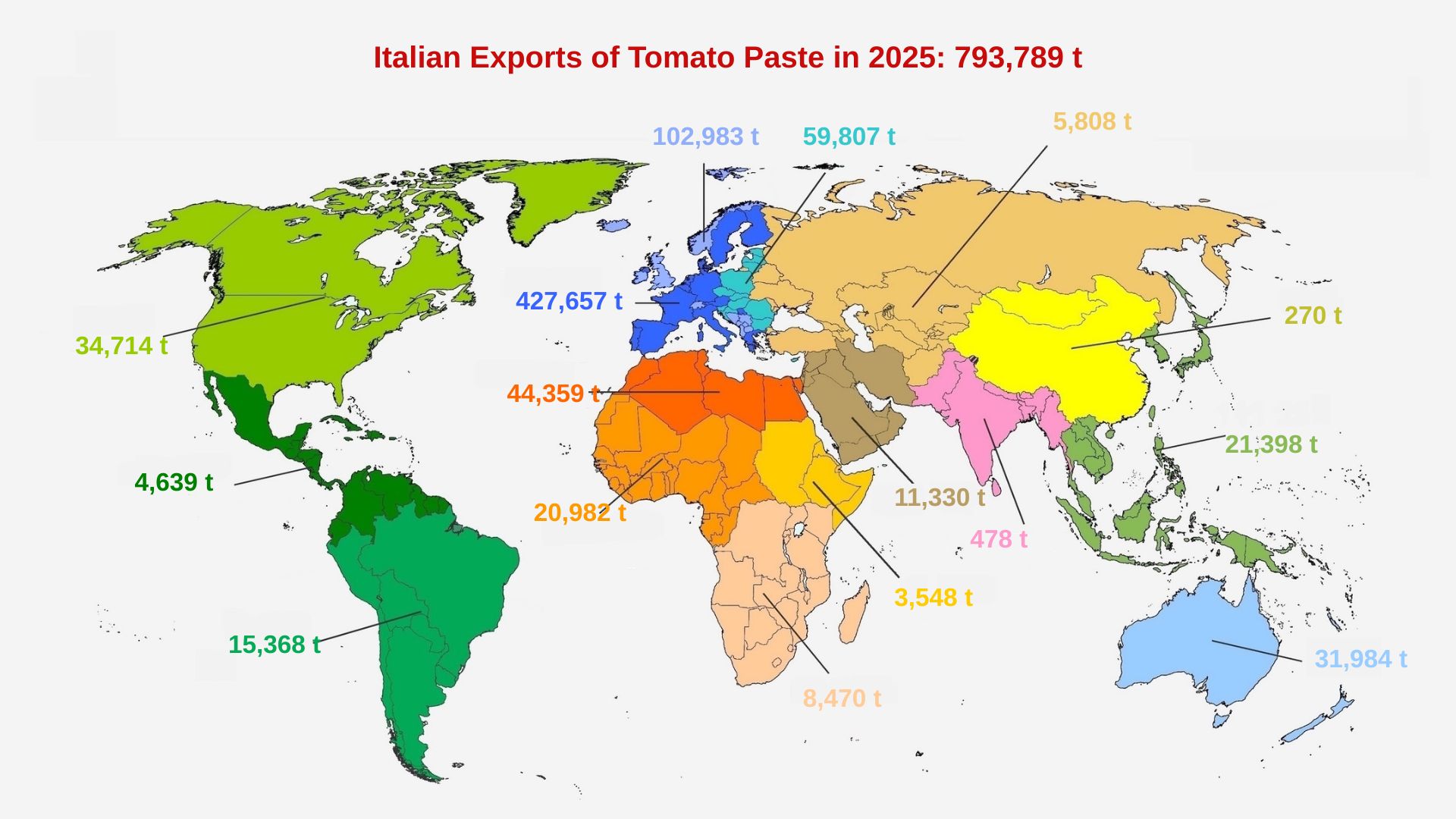

Italy benefits from a large domestic market, with strong brands and a strong image for quality which makes it popular also abroad. It is by far the largest exporter of canned tomatoes, with about 1.5 million tonnes annually, and the second of tomato paste with about 750 000 tonnes.

Italian tomato processors are represented within AMITOM and WPTC by ANICAV (private companies) and by Confcooperative (cooperatives).

(click on any of the images to expand it)