News

Global Processed Tomato Market: Foodservice vs. Retail Distribution – Part 3

Part Three: Development Prospects

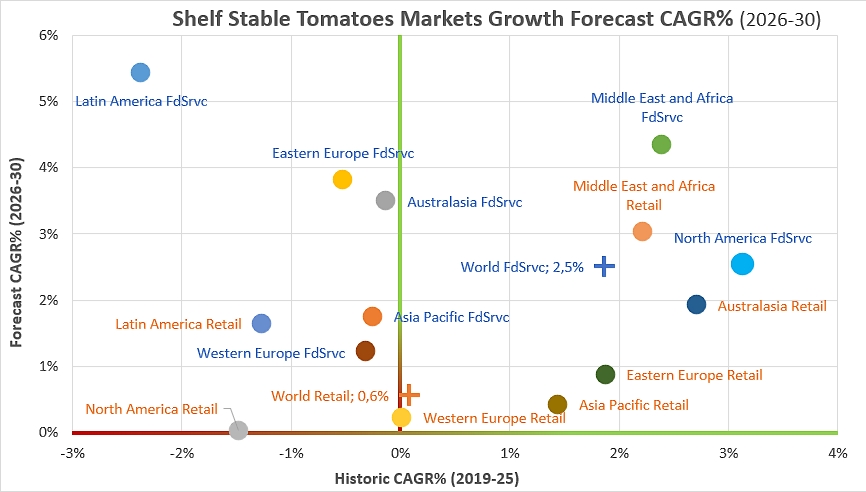

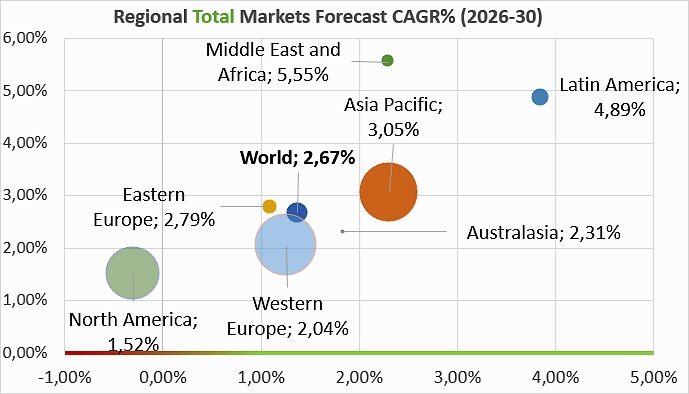

The prospective analysis to 2030 outlines a clear reversal of forces in the global processed tomato market, positioning out-of-home dining as the primary growth driver ahead of a retail network entering its maturity phase. Driven by a projected global growth of 4.0%, the professional channel is expected to orchestrate a spectacular catch-up, particularly stimulated by the dynamic markets of Asia-Pacific and North America. This redistribution of roles, which varies across product categories, signals a historic narrowing of the commercial balance between domestic and out-of-home consumption.

Prospects by distribution channel

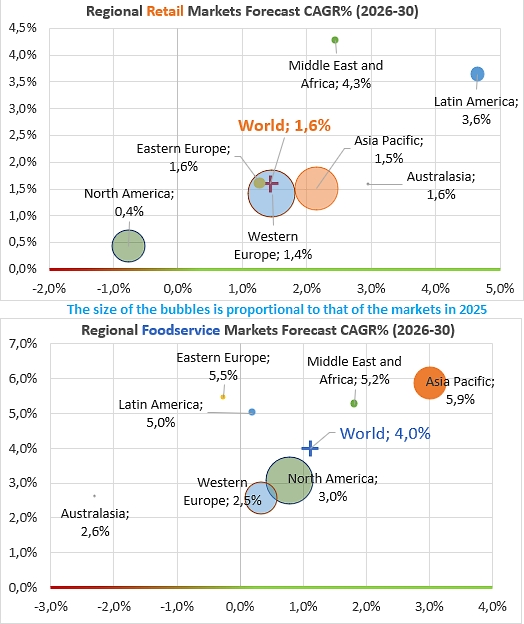

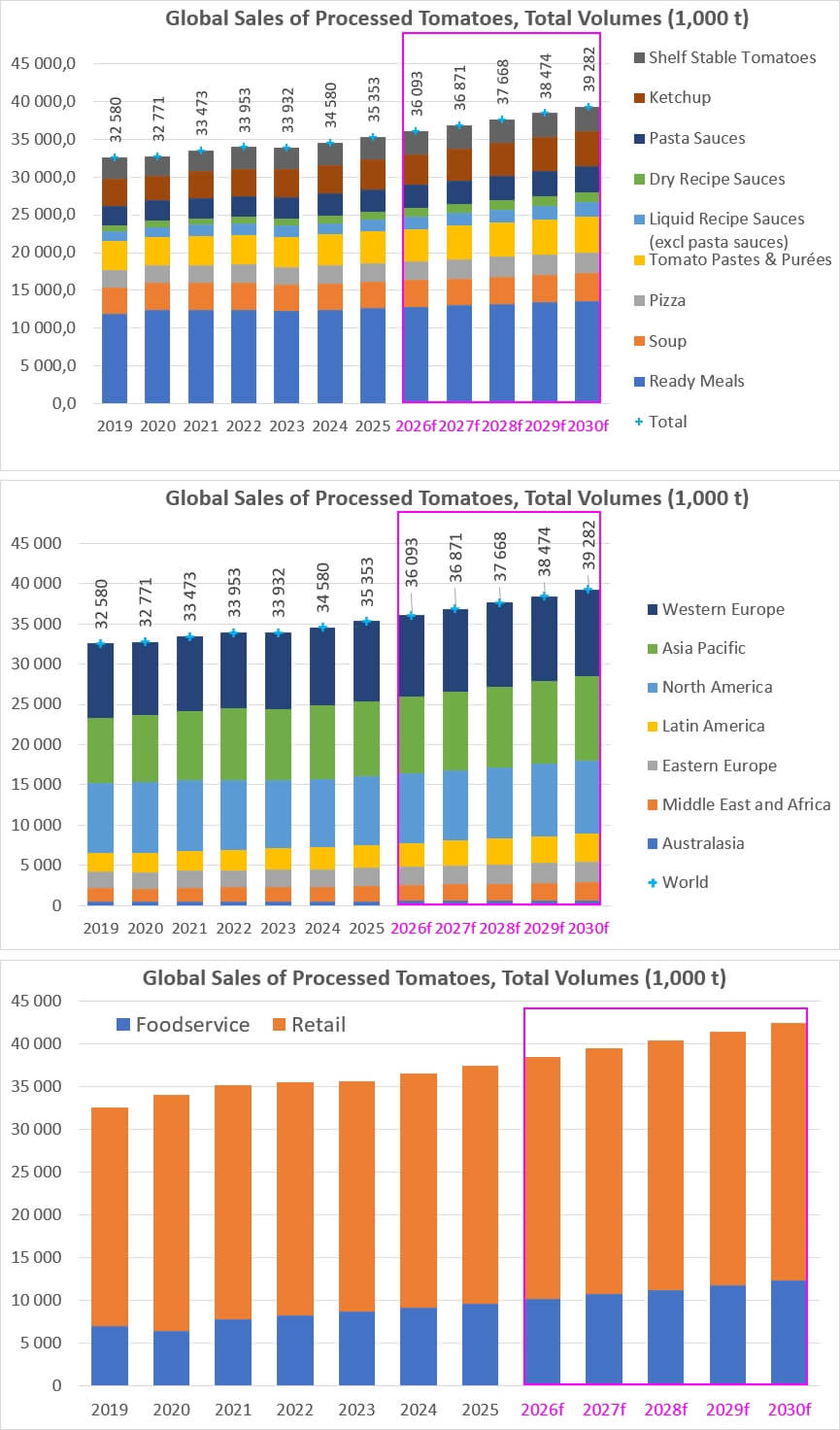

The global industrial tomato derivatives market shows a steady growth trajectory over the decade, with a notable acceleration in volumes projected between 2026 and 2030. Globally, demand in retail sales channels is expected to rise from 27.86 million tonnes in 2025 to 30.17 million tonnes in 2030, following a compound annual growth rate (CAGR) that progresses from 1.4% over the historical period to 1.6% over the forecast period. In parallel, the out-of-home dining segment displays a much more aggressive future dynamic on a global scale: after a modest increase of 1.1% per year over the 2019–2025 period, global volumes in this sector are projected to leap from 7.49 million tonnes to 9.11 million tonnes by 2030, driven by a robust forecast CAGR of 4.0%.

This asymmetry in growth rates leads to a gradual narrowing of the balance between foodservice and retail sales by 2030. In 2025, the retail sector largely dominates the market, absorbing more than 78% of global volumes (27.86 million tonnes compared to 7.49 million in out-of-home dining). By 2030, although retail distribution retains its supremacy in absolute terms with 30.17 million tonnes, the foodservice share will progress significantly to reach 9.11 million tonnes, thereby reducing the historical gap under the effect of the general recovery of out-of-home dining.

An examination of the regional data collected by Euromonitor shows that the Asia-Pacific region is emerging as one of the major drivers of this evolution, particularly for the out-of-home dining sector. In this region, the retail sector is expected to grow from 7.50 million tonnes in 2025 to 8.08 million tonnes in 2030 (CAGR declining from 3.0% over the historical period to 1.5% over the forecast period), while the foodservice sector is projected to expand spectacularly at an annual rate of 5.9%, bringing volumes from 1.82 to 2.43 million tonnes. In Western Europe, the market remains very large but more mature; the retail sector is expected to maintain its leading position there, progressing from 8.13 million tonnes in 2025 to 8.72 million in 2030 (1.4% CAGR), while the balance tends to narrow with foodservice sales expected at 2.05 million tonnes in 2030 compared to 1.80 million in 2025.

The American continent also reveals highly contrasting balance profiles. North America confirms its specificity with a very pronounced reliance on out-of-home dining, which already represented 2.62 million tonnes in 2025 and is expected to reach 3.03 million in 2030 thanks to a solid 3.0% CAGR, contrasting with the near-stagnation of its retail sector (5.94 million tonnes in 2025 and 6.06 million in 2030, representing 0.4% growth). In Latin America, products purchased in retail stores and consumed at home remain dominant, but both channels display excellent health; retail sales are growing firmly from 2.41 to 2.89 million tonnes (3.6% CAGR), while local foodservice is reviving after a stagnant period, jumping from 0.45 to 0.58 million tonnes under the effect of a projected annual growth of 5.0%.

Finally, the Eastern Europe and Middle East/Africa zones complete this overview with strong catch-up movements in out-of-home dining. In Eastern Europe, the balance overwhelmingly favoring the retail sector (1.97 million tonnes in 2025) is beginning to rebalance, driven by a very dynamic forecast CAGR of 5.5% for foodservice, bringing volumes in the latter sector to 0.35 million tonnes in 2030 after years of historical contraction. In the Middle East and Africa, the dynamic is remarkable across all channels: retail sales register the strongest upcoming global growth for this sector with an annual growth rate of 4.3% (expected to bring volumes from 1.45 to 1.78 million tonnes), but out-of-home dining is also projected to grow strongly to reach 0.56 million tonnes in 2030, supported by an average annual pace of 5.2%.

Regional Outlook (3 examples)

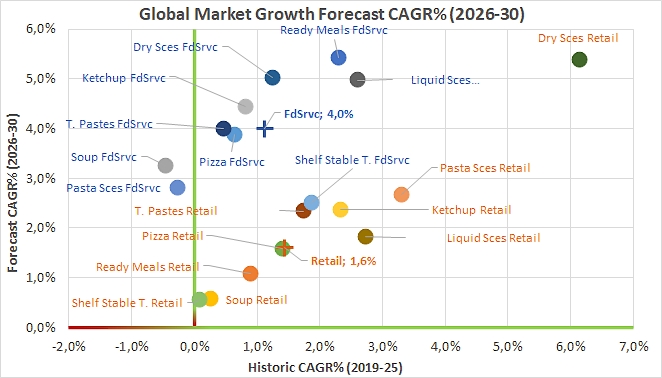

An analysis of regional growth prospects for various tomato derivative products confirms the spectacular reversal of dynamics already identified across distribution channels. While the historical period (2019–2025) had largely benefited retail sales, forecasts to 2026–2030 now position foodservice as the primary growth driver.

Between 2019 and 2025, retail sales significantly outperformed. Driven by the health crisis and the forced boom in at-home consumption, this channel saw the majority of its flagship categories—such as ketchup, pasta sauces, or liquid sauces—record solid historical growth rates of between 2.0% and 3.5%. Conversely, penalized by health restrictions, out-of-home dining remained globally stagnant over this period, with many product categories posting rates close to zero or even negative.

For the 2026–2030 period, the trend is expected to completely reverse: Foodservice is projected to record a robust overall compound annual growth rate (CAGR) of 4.0%, driven in particular by the dynamism of ready meals, ketchup, and tomato paste destined for professional users. In contrast, the retail sector is expected to see a sharp slowdown, settling at a modest annual average of 1.6%, with almost all of its volume segments dropping below the 2.5% mark for future growth. This global contrast thus sets the stage for the regional trajectories we will analyze for the three largest consumption basins (Western Europe, Asia-Pacific, North America).

- Western Europe

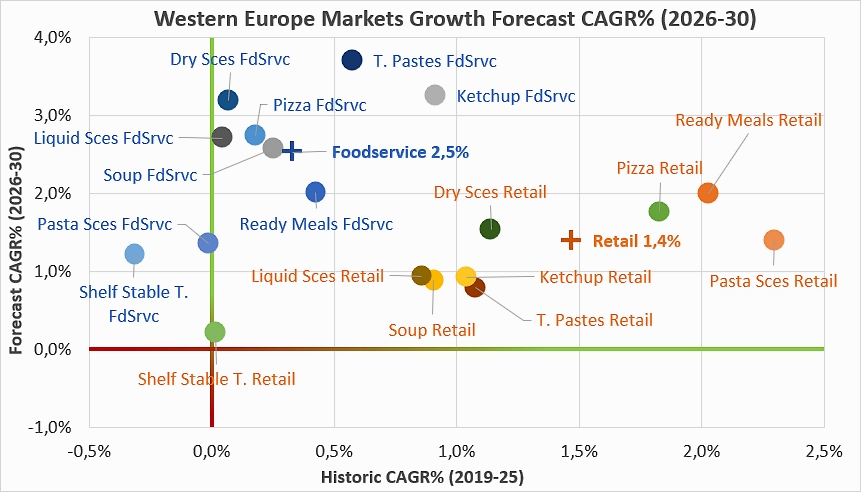

According to Euromonitor data, the tomato derivatives market in Western Europe remains structurally dominated in volume by retail sales. In 2025, this sector represented a massive volume of approximately 8.13 million tonnes, compared to only 1.80 million tonnes for out-of-home dining. Over the historical 2019–2025 period, retail sales posted a resilient compound annual growth rate of 1.5%, driven notably by ready meals, which reached 2.85 million tonnes in 2025, and pasta sauces at 0.50 million tonnes. Conversely, the foodservice channel experienced a period of marked stagnation, with historical growth of barely 0.3%, heavily impacted by the sharp drop in its volumes in 2020.

Prospects for the 2026–2030 period, however, show a clear change in dynamics, characterized by a vigorous catch-up in the foodservice sector. This channel is expected to see its compound annual growth accelerate to reach 2.5% per year, allowing its volumes to cross the 2.05-million-tonne mark by 2030. This revival relies heavily on high-volume categories such as tomato pastes and purées, whose professional use is projected to grow by 3.7% per year to reach nearly 0.49 million tonnes in 2030, as well as on ketchup in foodservice, projected at 0.35 million tonnes by the end of the period thanks to a sustained growth of 3.3%.

Meanwhile, retail sales in Western Europe are expected to enter a phase of maturity and stabilization over the 2026–2030 period, with a compound annual growth rate slowing slightly to 1.4%. Despite this deceleration, this channel will continue to capture the bulk of market volumes, with a cumulative total of 8.72 million tonnes expected in 2030. Ready meals will remain the undisputed pillar of self-service with a projected volume of 3.15 million tonnes, maintaining a stable growth of 2.0%, while the majority of other flagship retail categories, such as ketchup or soups, are expected to see their future progression flatten below the 1.0% per year mark.

- Asia-Pacific

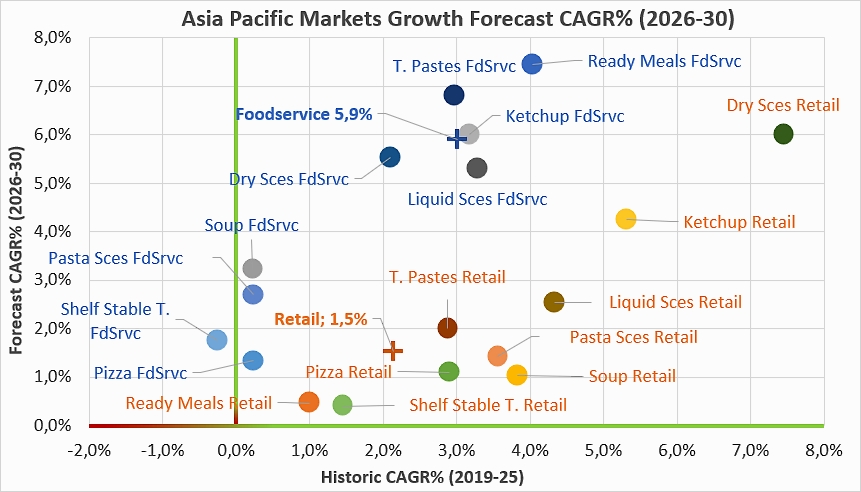

The retail sales channel displays a clear volume predominance in the Asia-Pacific tomato derivatives market, heavily driven by a single segment: in 2025, retail represented a total of 7.50 million tonnes, supported by nearly 5.12 million tonnes of ready meals. Over the historical 2019–2025 period, retail sales grew at a resilient compound annual rate of 2.1%, while foodservice posted more modest volumes but with a robust growth of 3.0% per year, reaching 1.82 million tonnes in 2025.

Prospects for the 2026–2030 period reveal a spectacular acceleration of commercial and institutional foodservice in the region. This sector stands out as the undeniable engine of the region’s future growth, with a projected compound annual rate of 5.9%, which should allow it to reach 2.43 million tonnes in 2030. This boom is primarily fueled by the explosion of professional ready meals, whose volume will increase by 7.5% per year to rise from 0.51 million tonnes in 2025 to 0.73 million tonnes in 2030, as well as by liquid sauces and ketchup destined for foodservice.

Conversely, the retail sales channel is expected to experience a sharp slowdown by 2030, growing at a modest compound annual rate of 1.5% (to reach 8.08 million tonnes in 2030). This notable flattening is directly correlated with the near-stagnation of its main pillar: the category of ready meals sold in retail stores is projected to see its future growth plummet to just 0.5% per year (5.24 million tonnes in 2030). The dynamic of the retail sector is anticipated to rely more heavily from now on on categories like ketchup, maintaining a solid progression of 4.3% per year to reach nearly 0.68 million tonnes in 2030.

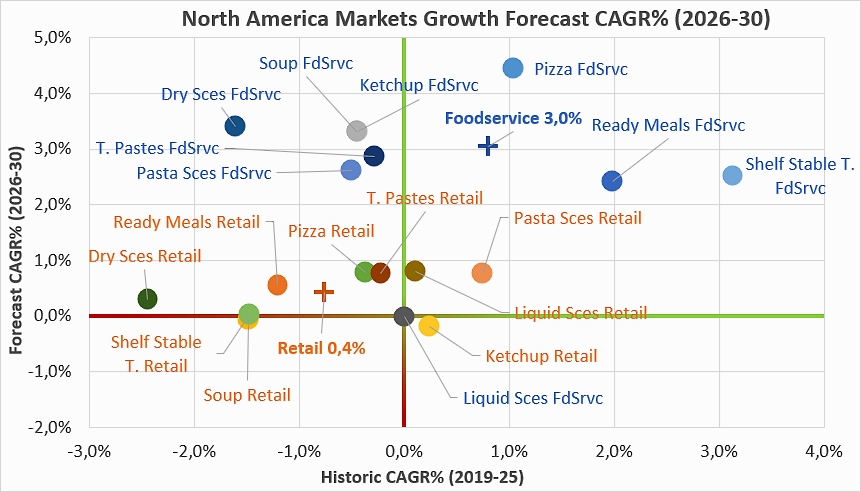

- North America

North America displays a unique market profile, characterized by a substantial historical volume in the retail sales channel but also by a future dynamic very clearly to the advantage of the foodservice sector. In 2025, retail represented a total volume of 5.94 million tonnes, relying primarily on ready meals (2.24 million tonnes), soups (1.08 million tonnes), and pasta sauces (0.91 million tonnes). Over the historical 2019–2025 period, however, the retail sector experienced a marked recession with an average annual decline of 0.8%, impacted by the structural decline of ready meals, soups, and pizzas. Conversely, foodservice paradoxically resisted better, posting a timid historical growth of 0.8% per year to reach 2.62 million tonnes in 2025, heavily supported by canned tomato sales, which amounted to 0.91 million tonnes.

As with the regions already mentioned, prospects for the 2026–2030 period mark a clear shift in favor of foodservice, which establishes itself as the region’s true growth engine. This sector is expected to expand at a robust compound annual growth rate (CAGR) of 3.0%, allowing it to cross the 3.03-million-tonne mark by 2030. This future dynamism is expected to touch almost all product categories, with a marked acceleration for soups (+3.3% per year to reach 0.70 million tonnes), pizzas (+4.5%), and ketchup (+3.3% to reach 0.59 million tonnes in 2030), while canned tomatoes will pursue steady growth at a pace of 2.5% per year to exceed one million tonnes (1.03 million tonnes).

In contrast, the retail sales channel in North America is expected to experience a phase of near-stagnation over the 2026–2030 period, with a marginal compound annual growth rate of only 0.4%, reaching a total of 6.06 million tonnes in 2030. Almost all flagship segments of the retail sector are projected to display growth rates below 1.0%: ready meals would grow by a modest 0.5% per year (up to 2.30 million tonnes in 2030), pasta sauces would stabilize at 0.8% (0.94 million tonnes), while ketchup (-0.2%) and soups (-0.1%) are expected to continue their slow decline.

Compared to Western Europe and Asia-Pacific, North America stands out for a much more pronounced lethargy in its retail sales channel (+0.4% future growth compared to around 1.5% for the other two regions). Furthermore, while retail sales of ready meals are running out of steam in Asia-Pacific (+0.5%) but holding up well in Europe (+2.0%), they remain extremely stable—though at a very low growth level—in North America (+0.5%). Finally, the projected growth of the North American out-of-home dining sector (+3.0%) positions itself at an intermediate level: it surpasses the cautious maturity of the European market (+2.5%), but lags far behind the phenomenal explosion observed on the Asian continent (+5.9%).

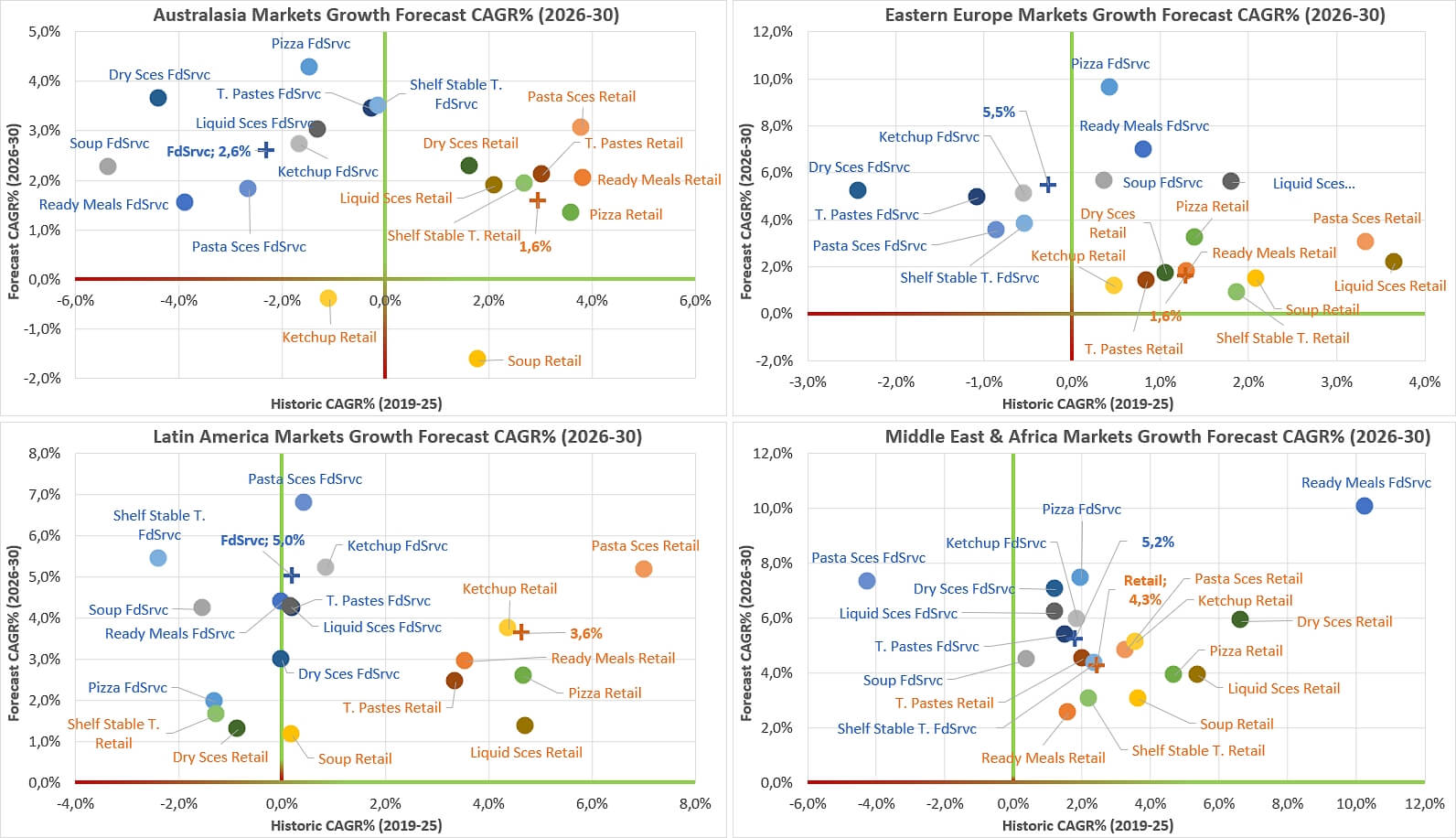

Charts illustrating growth projections for the other regions (Australasia, Eastern Europe, Latin America, and Middle East-Africa) are presented in the supplementary information at the end of the article.

Regional Outlook by Product, Foodservice & Retail (4 examples)

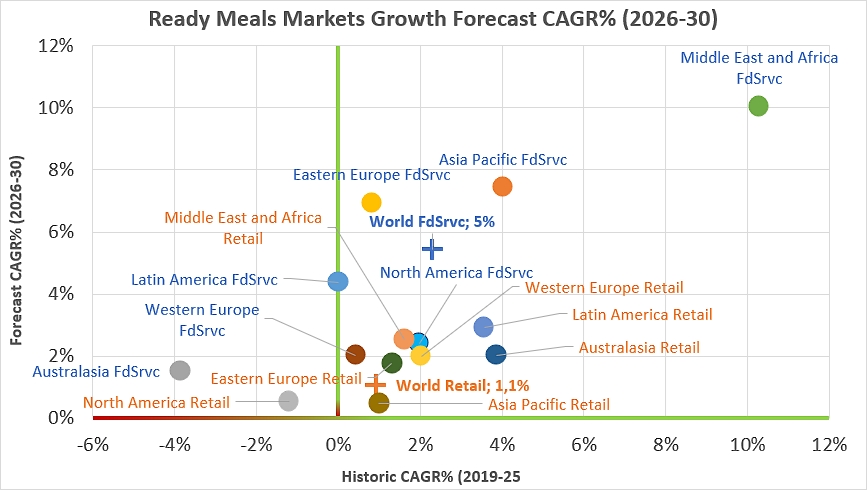

- The global ready meals market is characterized by a massive structural imbalance in favor of the retail trade sector, which historically eclipses the out-of-home dining segment in terms of volume. In 2019, retail sales already represented more than 11.1 million tonnes, compared to only 810,000 tonnes for foodservice. This divergence widened during the 2020 health crisis: while volumes collapsed in foodservice to 653,000 tonnes due to lockdowns, retail sales leaped to over 11.7 million tonnes, capturing the bulk of home consumption.

However, post-pandemic dynamics also reveal a clear reversal in growth trends. The foodservice sector shows a robust recovery and a more aggressive projected trajectory. Between 2026 and 2030, its compound annual growth rate (CAGR) is expected to accelerate to 5.4%, reaching 1.21 million tonnes by the end of the decade. Conversely, the retail sector is expected to enter an advanced phase of maturity, with an anticipated annual growth limited to 1.1% over the same forecast period, culminating at 12.37 million tonnes in 2030.

Geographically, Asia-Pacific stands out as the true engine of this transformation. For the foodservice sector, this region drives global growth with a spectacular expected expansion rate of 7.5% per year, which should bring volumes to around 731,000 tonnes in 2030. Asia-Pacific also dominates the retail sales sector with over 5.1 million tonnes as early as 2025.

Western Europe and North America display more mature profiles. In Western Europe, retail sales maintain steady growth of 2.0% (targeting 3.1 million tonnes in 2030), while North America shows signs of saturation in the retail trade, recording a historical decline before stabilizing at a timid growth rate of 0.5% per year. Thus, although the retail sector maintains its dominance in terms of volume, out-of-home dining, revitalized by Asia-Pacific and Eastern Europe, now dictates the pace of innovation and expansion in the global market.

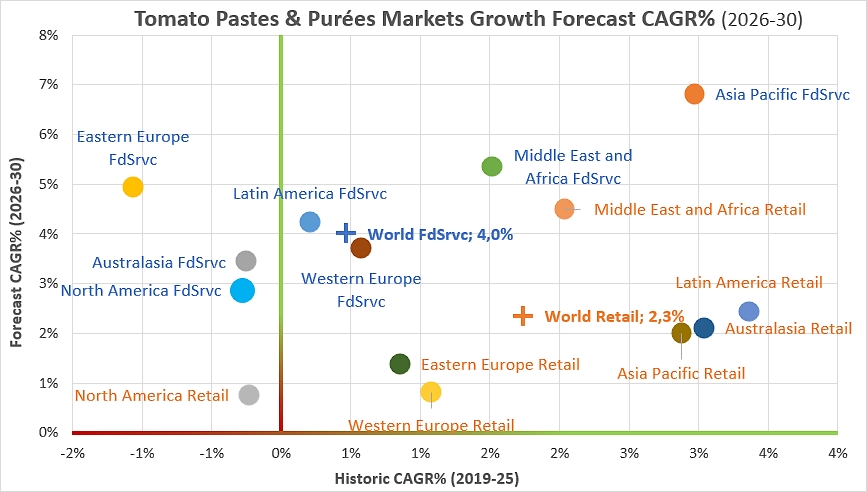

- Euromonitor data show that the global market for tomato pastes and purées rests on a balance structurally dominated by the retail trade sector, although the projected growth dynamic tends to rebalance in favor of out-of-home dining. In 2019, the total volume absorbed by retail sales amounted to 2.65 million tonnes, compared to 1.18 million tonnes in foodservice. The 2020 health measures widened this gap: while facility closures caused foodservice sales to drop to 0.83 million tonnes, retail sales of pastes and purées rose to 2.84 million tonnes, driven by the explosion of home cooking.

This historical duality is evolving toward a new configuration by 2030. After a stabilization period (2019–2025) marked by a timid annual increase of 0.5%, the foodservice sector is poised to become the primary growth engine of the global market for pastes and purées. Between 2026 and 2030, its compound annual growth rate (CAGR) is expected to reach 4.0%, allowing volumes to settle at 1.47 million tonnes in 2030. Meanwhile, the retail trade should pursue a steadier but slower upward trajectory, with a projected annual increase of 2.3%, likely to bring the sector to 3.29 million tonnes by the end of the decade.

Geographically, consumption behaviors reveal sharp regional disparities. Western Europe remains a major historical pillar, with a strong entrenchment of the retail trade, which mobilized 1.03 million tonnes in 2025, complemented by a solid foodservice sector at 0.41 million tonnes. Concurrently, the Middle East and Africa region is establishing itself as a high-growth zone for tomato pastes and purées, particularly for retail sales, which reached 0.87 million tonnes there in 2025 and show a future growth forecast of 4.5% per year. In Asia-Pacific, on the contrary, foodservice dictates the tempo with a spectacular future progression of 6.8% per year, which should almost double its volumes between 2019 and 2030. On a global scale, retail channels retain the bulk of the volumes, but it is indeed out-of-home dining that is driving the global sectoral recovery.

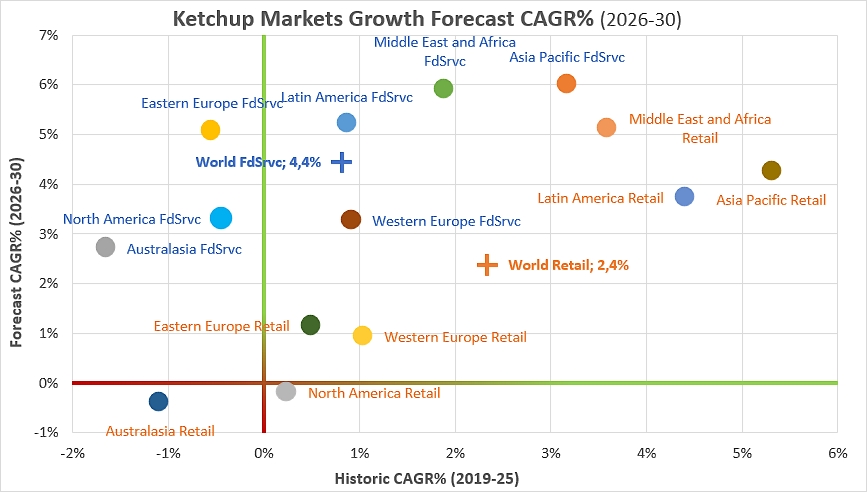

- The global ketchup market presents a more balanced distribution between the retail trade sector and out-of-home dining than the other products in the Euromonitor panel, even though ketchup sales in retail trade retain the majority of volumes. In 2019, global ketchup commercialization in retail sales represented 2.04 million tonnes, compared to 1.50 million tonnes in foodservice. The upheavals of 2020 caused a sharp distortion: the closure of restaurants sent the latter sector plunging to 1.07 million tonnes, while home consumption stimulated retail sales, which rose to 2.25 million tonnes.

The post-crisis recovery, however, resulted in a marked return of the foodservice sector, which now shows a much more vigorous growth dynamic for the end of the decade. Over the forecast period (2026–2030), global out-of-home dining is expected to post a sustained compound annual growth rate (CAGR) of 4.4%, allowing the sector to reach 1.96 million tonnes in 2030. Meanwhile, the retail sector is projected to pursue a more linear and moderate expansion of 2.4% per year, settling at 2.64 million tonnes by the end of the period.

Analysis by major regions highlights the central role of North America, a historical pillar of the market, which consumed 0.50 million tonnes in foodservice and 0.41 million tonnes in retail sales as early as 2025. However, the mature markets of North America and Western Europe are heading toward a stagnation of ketchup sales in retail trade, with future growth rates below 1%, or even close to zero.

The true engine of geographical expansion is shifting toward Asia-Pacific. This zone combines a strong increase in retail sales (4.3% projected CAGR to reach 0.68 million tonnes in 2030) and a spectacular acceleration of its foodservice sector, estimated at 6.0% per year over the forecast period. The Middle East and Africa region follows a similar trend, with expected annual growth rates exceeding 5% for both segments. Thus, the future dynamic of global ketchup relies heavily on the rise of out-of-home dining and the increased penetration of emerging markets.

- The global canned tomato market stands out due to a historically very tight volume balance between the out-of-home dining sector and the retail trade sector. In 2019, both segments displayed relatively close volumes, with 1.34 million tonnes in foodservice and 1.52 million tonnes of canned tomatoes in retail sales. The year 2020 caused a major distortion by temporarily reversing the balance of power: health restrictions sent foodservice volumes plunging to 0.91 million tonnes, while household consumption stimulated retail commercialization, which leaped to 1.66 million tonnes.

Since this shock, the canned tomato market has rebalanced and is now heading toward a lasting dominance of the foodservice sector in terms of both volumes and growth dynamics. Over the historical 2019–2025 period, the retail sector remained virtually stagnant, with a compound annual growth rate (CAGR) of just 0.1%. Forecasts for the 2026–2030 period confirm this advanced maturity trend for the retail trade, whose global annual growth is expected to cap at 0.6%, reaching 1.57 million tonnes in 2030. Conversely, the quantities of canned tomatoes sold in foodservice are projected to grow at a steadier pace of 2.5% per year, bringing volumes to 1.70 million tonnes by the end of the decade.

Geographically, North America stands out as the leading global pillar of this market, spectacularly driven by foodservice. In 2025, the North American out-of-home dining sector alone already represented 0.91 million tonnes and is expected to cross the one-million-tonne threshold (1.03 million) by 2030, maintaining a future annual growth of 2.5% while its retail sales sector will completely stagnate at 0.0%.

Western Europe constitutes the second major historical market, with 0.32 million tonnes in foodservice and 0.68 million tonnes in retail sales in 2025; this market displays high stability, with very timid future growth prospects for both channels. The true geographical growth drivers are located in Latin America as well as in the Middle East and Africa, where the foodservice sector projects expansion rates of 5.4% and 4.3% per year, respectively. In short, the future of global canned tomatoes rests on the solid foundation of American foodservice and the rise of out-of-home channels in emerging economies.

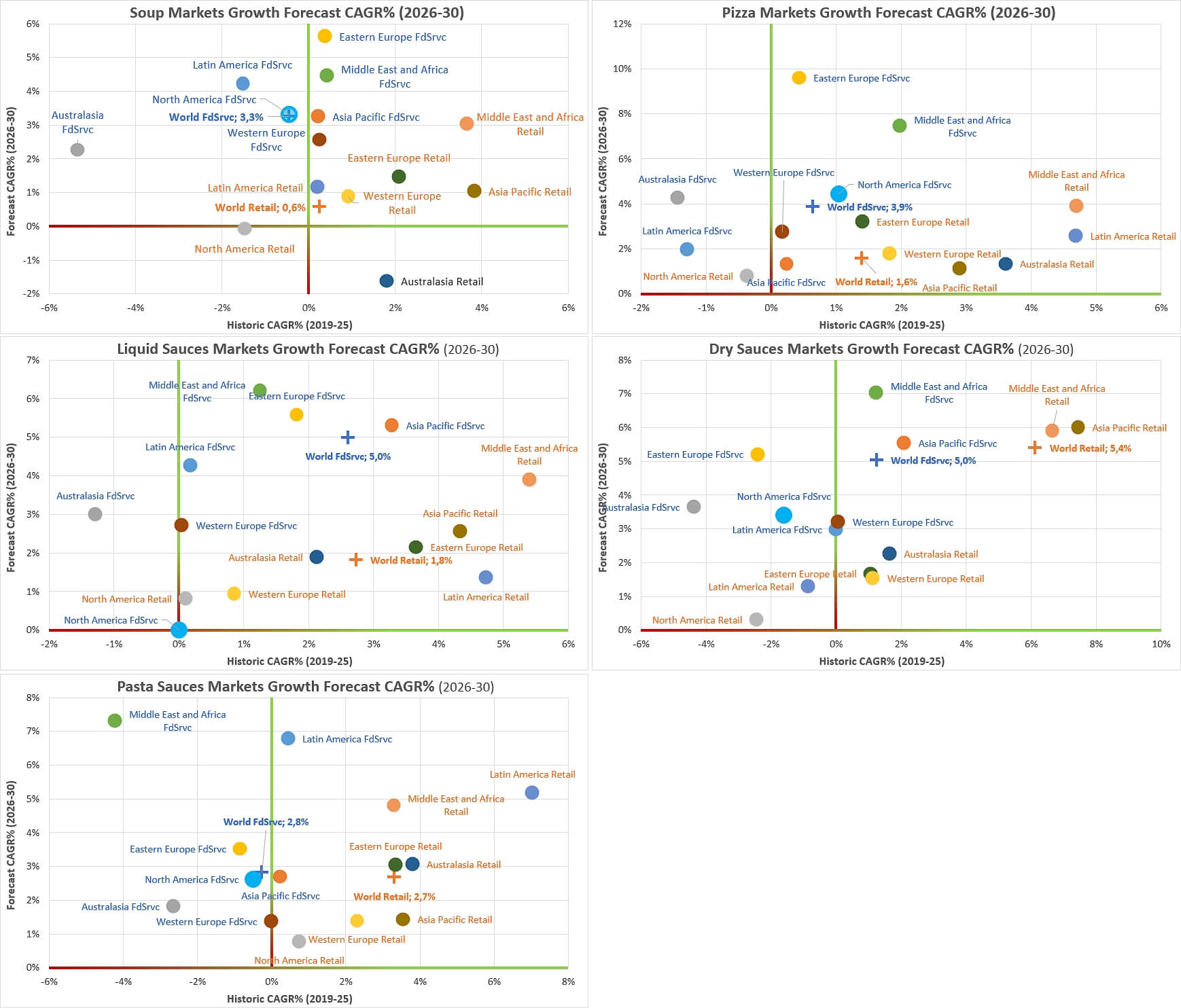

Charts illustrating growth projections for the other products (Soup, Pizza, Liquid Sauces, Dehydrated Sauces, and Pasta Sauces) are presented in the supplementary information at the end of the article.

Some complementary data

Evolution of Global Sales of Tomato Derivatives, by Product, Region, and Distribution Channel.

Growth Outlook by Region, for the Different Products (Australasia, Eastern Europe, Latin America, Middle East & Africa)

Growth Outlook by Product, across the Different Regions (Soup, Pizza, Liquid Sauces, Dry Sauces, Pasta Sauces)

Volume Growth Outlook, across the Different Regions

For details on the Euromonitor product categories, click here.

Source: Euromonitor

{kind=link}