News

Global Processed Tomato Market Volume Trends

The following is an analysis of Euromonitor data for the global processed tomato market, covering market volumes from 2019 to 2030. This report highlights the shifting dynamics between mature and emerging markets, distinguishing between historical performance and future projections.

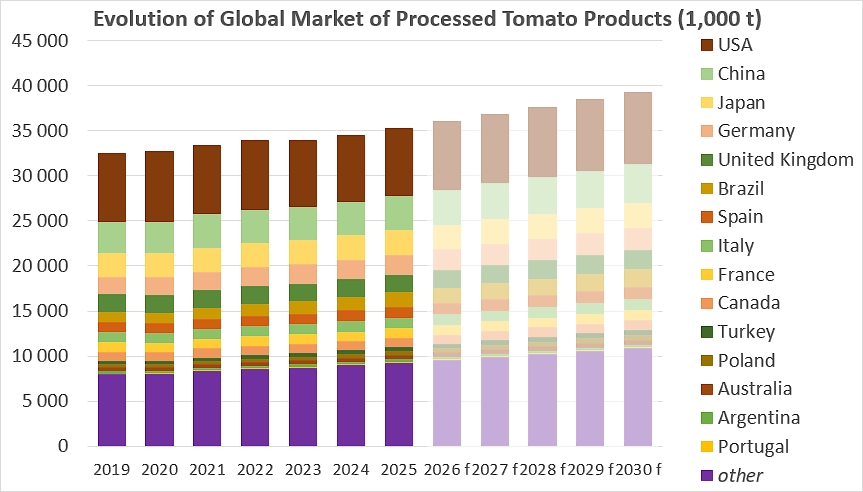

According to figures collected by Euromonitor, the global market for tomato products and various products containing processed tomatoes (see details below) shows steady and resilient growth, rising from 32.58 million tonnes in 2019 to a projected 39.28 million tonnes in 2030, representing an overall increase of approximately 20.6%. After a period of slight stagnation between 2022 and 2023, where consumption stabilized around 33.9 million tonnes, forecasts point toward a sustained recovery starting in 2024. This dynamic is rooted in strong geographical concentration, as the top five consuming countries—the United States, China, Japan, Germany, and the United Kingdom—alone accounted for more than 50% of the global market in 2025.

Market Composition and Evolution

Last year, the United States maintained its position as the undisputed leader with a 21% market share. Despite a sharp slowdown recorded at the beginning of the decade, falling to 7,446 thousand tonnes in 2023, US consumption is expected to rise again to cross the 8,023 thousand-tonne mark by 2030.

Meanwhile, China is asserting itself as the sector’s primary growth engine: its consumption is projected to increase by over 850,000 tonnes over the period, reaching 4.29 million tonnes in 2030. However, the most spectacular acceleration is credited to Brazil, where demand is expected to grow by 82% between 2019 and 2030—rising from 1,100 to 2,003 thousand tonnes—reflecting a profound transformation in local dietary habits.

Major Consumption Hubs

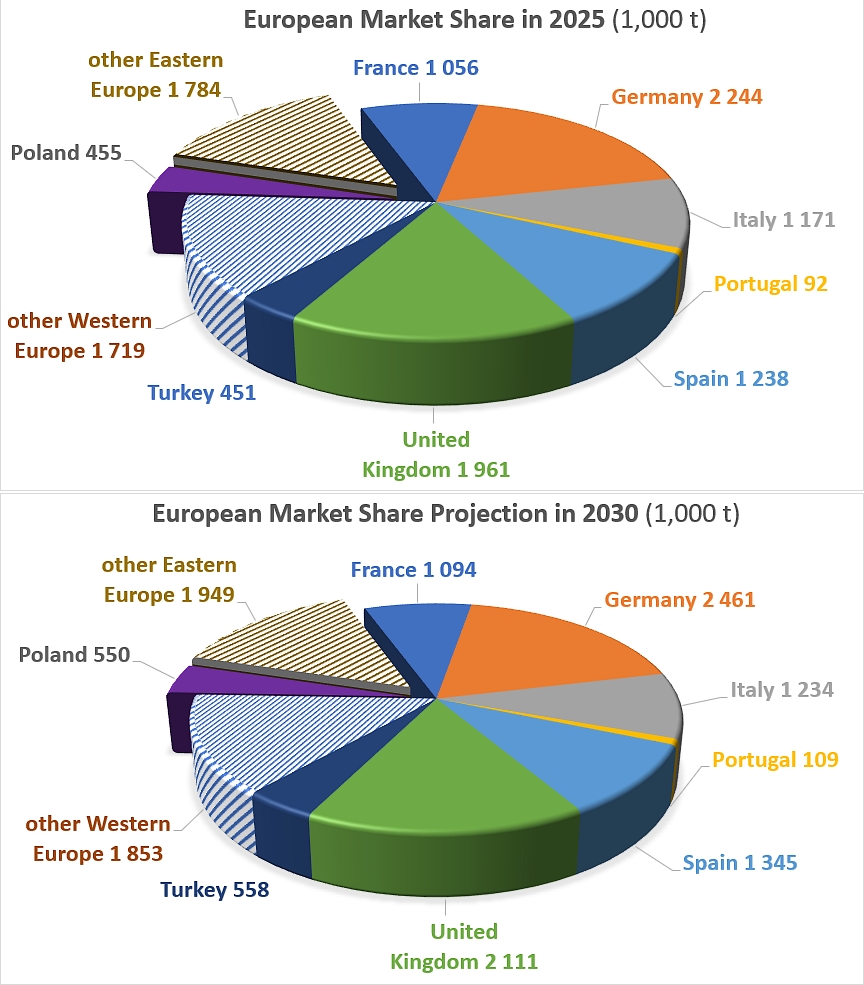

In Europe, trajectories diverge based on market maturity. With total quantities of 2.2 and 1.2 million tonnes of tomato derivatives consumed in 2025, Germany and Spain are driving regional growth with increases of approximately 26% from 2019 up to 2030. Conversely, France and Italy, with volumes between 1.1 and 1.2 million tonnes, show very moderate growth, respectively close to 3% and 9% on the same 12-year period. Other countries, such as Poland and Turkey, demonstrate remarkable strength with projected increases of 52% and 51% by 2030. On the other hand, saturated markets like Japan and Canada show nearly flat curves, with consumption now primarily driven by demographics. The “Rest of the World” category carries significant weight in the global balance, expected to draw 10.861 million tonnes—or 27% of the global total—in 2030, an increase of nearly 36% over the 2019-2030 period.

Europe, taken in its broadest sense, constitutes a major and diversified consumption bloc, accounting for approximately 20% of the global volume projected at 39.28 million tonnes in 2030. This bloc ranks as the second-largest consumption hub behind the United States (8.02 million tonnes) and ahead of China (4.29 million tonnes).

Within this European set, Germany is expected to hold the leading position in 2030 with a volume of 2.46 million tonnes, ahead of the United Kingdom, which is stabilizing at 2.11 million tonnes. Southern Europe remains a central consumption hub: Spain (1.34 million tonnes) and Italy (1.23 million tonnes) should maintain high levels, ahead of France at 1.09 million tonnes. The landscape of 2030 is completed by significant markets such as Turkey (0.56 million tonnes) and Poland (0.55 million tonnes), as well as Portugal (0.11 million tonnes), confirming that European demand is expected to remain solidly anchored despite the emergence of other powers like Brazil (2 million tonnes).

Market Shares

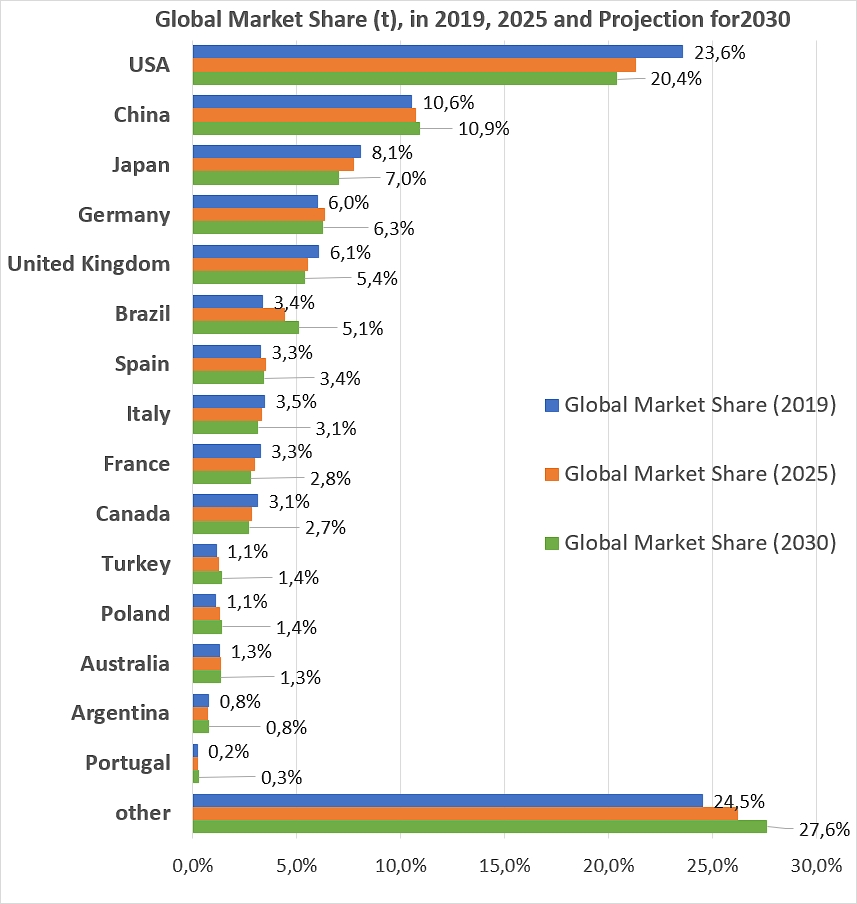

On a broader level, market share analysis highlights a global rebalancing in favor of emerging zones, marked by the relative decline of the United States, whose dominance is expected to shift from 24% to 20%. This 4-point drop suggests that, despite significant volumes, the world’s leading consumer is losing ground to the geographical diversification of demand.

Brazil emerges as the great winner of this period, increasing its market share from 3% to 5%, a progression illustrating its new status as a sector heavyweight. Meanwhile, the “Other countries” category could gain 3 points to reach 28% of the total, confirming market fragmentation and the spread of consumption to new regions.

China, while remaining the market’s second pillar, sees its share stagnate at 11%, indicating that its internal growth is evolving at the same pace as the global average without shifting the balance of power in its favor. Conversely, mature markets like Japan and the UK could experience an erosion of influence, each losing approximately 1 market share point over the period.

In continental Europe, the development prospects of historical pillars such as Germany (6%), France (3%), Italy (3%) and Spain (3%) demonstrate remarkable resilience by strictly maintaining their relative positions. This stability suggests that these markets, though mature, retain a solid consumption base in the face of expanding new international players.

Finally, the bottom of the rankings remains unchanged with actors like Portugal, Argentina, Australia, Poland, and Turkey, whose weight oscillates between 0% and 1%. These countries are expected to remain peripheral markets on a global scale, as their cumulative consumption fails to alter the global hierarchy dominated by the USA-China-Europe trio.

Global Market Acceleration

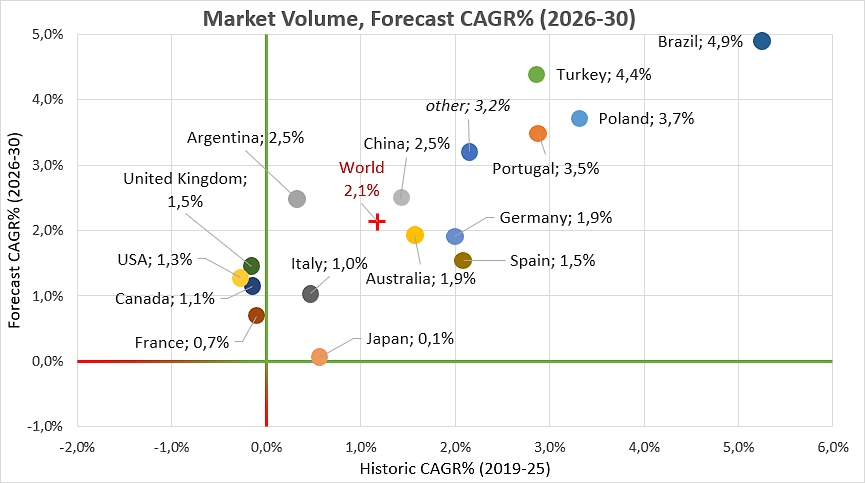

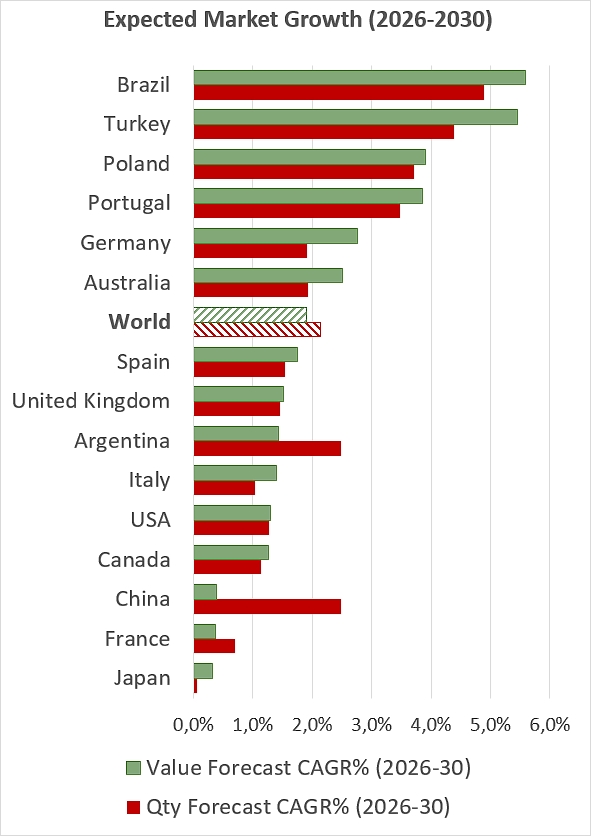

Analysis of Compound Annual Growth Rates (CAGR) reveals an acceleration in global demand, with the pace of progression expected to intensify from 1.2% during the historical period (2019-2025) to 2.1% for projections at the end of the decade (2026-2030). This global dynamic is driven by the awakening of large mature markets like the USA and Canada, which, after a slight decline of -0.1%, are expected to return to positive growth between 1.1% and 1.3%. The United Kingdom shows an even more marked recovery, jumping from 0.1% to 1.5%, confirming a renewed vitality for these historic economies.

Brazil stands out as the undisputed growth champion across the entire global market: although its development pace is slowing slightly from 6.0% to 4.9%, it maintains the strongest annual progression in the panel and asserts itself as the market’s new engine. Simultaneously, the dynamism of emerging markets remains steady, with Turkey accelerating to 4.4% and Poland maintaining a very high level of 3.7%, both far exceeding the expected global average (2.1%). China follows a similar upward trajectory, with its annual growth rate rising from 1.8% to 2.5%.

In contrast, a marked slowdown is observed in Western Europe and Japan, where markets appear to be entering the end of a cycle. France and Italy remain confined to very low growth rates, fluctuating between 0.7% and 1.0%, while Spain and Germany could see their momentum slow to 1.5% and 1.9% respectively. Within this broad spectrum, Japan shows the weakest outlook, close to zero, with a projected rate of only 0.1%, highlighting near-total saturation. Finally, the “Other countries” category confirms the trend toward global consumption diffusion by accelerating from 2.6% to 3.2%.

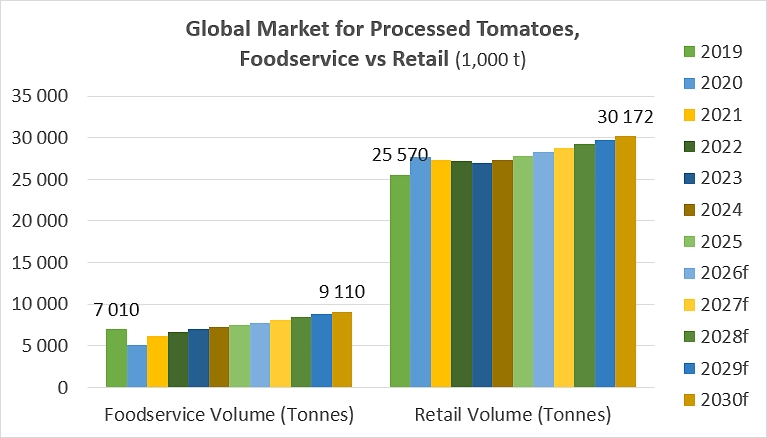

The Rise of Foodservice

The analysis of global figures also reveals a profound shift in consumption patterns, marked by a transition from the historical dominance of at-home consumption to the growing influence of professional foodservice. In 2019, the market was balanced with retail accounting for 78.5% of global volumes; the 2020 disruption momentarily upended this structure, driving the retail share to 84.4% while foodservice channels receded to around 15.6%. However, the sector’s resilience is striking: the massive shift toward home-cooked meals allowed the total market to remain stable, proving that tomato derivatives are essential staples whose overall volume does not falter, but simply relocates.

Looking ahead to 2030, the dynamic reverses radically in favor of Foodservice. This segment is expected to show spectacular acceleration with a projected annual growth rate (CAGR) of 4.0% between 2026 and 2030—more than double the pace expected for retail, which is limited to 1.6%. This differential can be explained by increasing urbanization and the rise of out-of-home dining in emerging economies, where processed tomatoes have established themselves as a core ingredient for fast-food and themed restaurant chains. Consequently, the relative market share of foodservice is expected to reach 23.2% by 2030, representing a gain of nearly eight percentage points from its pandemic low.

This evolution reflects a “professionalization” of the industry. While the retail market reaches maturity with modest, linear progression, more technical channels are becoming the true engine of growth. By the end of the decade, within a market expected to total more than 39.2 million tonnes, foodservice sales will absorb an increasingly significant portion of global production, mirroring a lifestyle where final product preparation is more frequently delegated to chefs and industrial kitchens rather than the end consumer.

Premiumization or Commoditization?

Comparing growth in volumes and revenue for the 2026-2030 period reveals contrasting pricing strategies and market dynamics by region. At the global level, a relative balance is observed with a CAGR of 2.1% in quantity versus 1.9% in value, suggesting slight pressure on unit prices worldwide.

In developed and mature economies, value growth tends to exceed volume growth, indicating a move upmarket or the pass-through of inflation. In Germany, the gap is particularly striking at 2.8% in value versus 1.9% in quantity, signaling increased market valuation. This phenomenon is identical in Australia (2.5% vs 1.9%) and, more moderately, in Italy (1.4% vs 1.0%) and Spain (1.7% vs 1.5%). In the United States, both indicators are perfectly aligned at 1.3%, reflecting great stability in real prices.

Conversely, some countries show volume growth significantly higher than value growth, suggesting lower unit prices or intensifying competition. The case of China is the most striking, with a volume CAGR of 2.5% against only 0.4% in value, reflecting a strong “commoditization” of tomato products. A similar, though less pronounced, trend is visible in France (0.7% in quantity vs 0.4% in value) and Argentina (2.5% in quantity vs 1.4% in value).

Finally, high-growth markets maintain a positive dynamic on both fronts, often with a premium on value. Brazil dominates with 5.6% in value against 4.9% in volume, followed closely by Turkey (5.5% vs 4.4%). These countries, along with Portugal (3.9% in value) and Poland (3.9% in value), demonstrate that in expanding zones, increased sales quantities are accompanied by the ability to generate more value, confirming the dynamism and attractiveness of these markets for years to come.

In conclusion, the global processed tomato market as described by Euromonitor demonstrates remarkable resilience, with annual growth expected to accelerate to 2.1% by 2030. This momentum is driven by a geographical shift toward emerging hubs such as Brazil and China, which are challenging the historical dominance of the US-Europe bloc while diversifying global demand.

This transformation is primarily fueled by the rise of Foodservice. With an annual growth rate of 4.0%, professional catering is establishing itself as the sector’s true engine, capturing nearly 23% of global volumes by the end of the decade. This professionalization trend requires industry players to navigate between premiumization in mature countries and volume-based strategies in rapidly expanding regions.

With a projected volume of 39 million tonnes in 2030, processed tomatoes confirm their status as a cornerstone of the global food supply. Moving forward, the success of operators will depend on their agility in serving increasingly technical channels and adapting their value models to the specificities of each region.

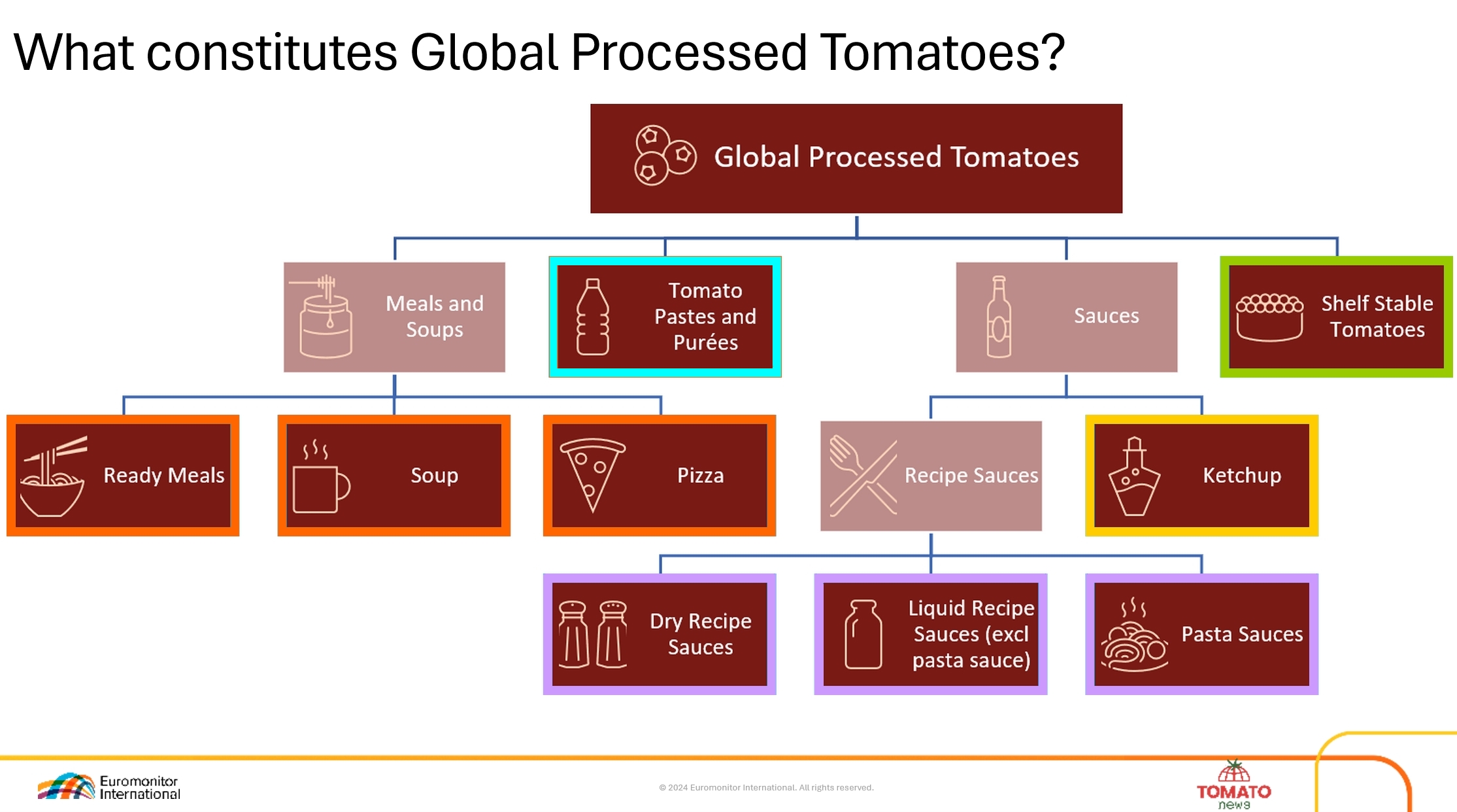

Composition of Global Processed Tomato Market

Methodology: Euromonitor’s forecasting methodology integrates quantitative econometric modeling with qualitative local expertise. At its core, the system utilizes regression-based frameworks to link historical sales data with key macroeconomic drivers—such as GDP, inflation, and disposable income—which are updated quarterly. Beyond statistical modeling, the approach incorporates structural factors like demographics and urbanization, while analysts apply an “expert layer” to account for industry-specific trends, innovation, and channel shifts. This hybrid model also allows for scenario and shock modeling, ensuring that projections remain market-realistic and adaptable to potential economic disruptions.

In future articles in this series, we will examine in more detail the characteristics of some regional and national markets, as well as the balance between food service and retail distribution channels for processed tomato products.

Source: Euromonitor

{kind=link}