News

Algeria: Fresh and processed tomato production set to increase

According to the president of the National Interprofessional Council of the Tomato Sector (CNIFT), Mostefa Mazouzi, quoted by Finabi Conseil in a report released in July 2025, “fresh and industrial tomato production has increased steadily in recent years to reach a record figure of 2.7 million tonnes in 2024”.

“The production of industrial tomato recorded an exceptional surplus this year,” Mazoudi had already declared to Jeune Indépendant in September 2024, noting that we had tomato throughout the year. This was attributed to to the different production centres at the national level and also to the strategy adopted three years ago.

He also highlighted the record production recorded at the eastern pole, in the wilayas of Annaba, Skikda, El Taref and Guelma, where 17,000 hectares are devoted to tomato production, in addition to the good results achieved at the extreme eastern pole of the country, i.e. at the wilayas of Souk Ahras, Oum El Bouaghi, Khenchla and Tébessa. Other wilayas, especially in the south (Oued Souf, In Salah, El Meniaa and Adrar) to bring the total surface planted to 34,000 hectares and guaranteeing production throughout the year. This level of production has made it possible to lower the price, especially since “the kilo is sold between 50 and 60 dinars (33 to 40 euros per tonne)”.

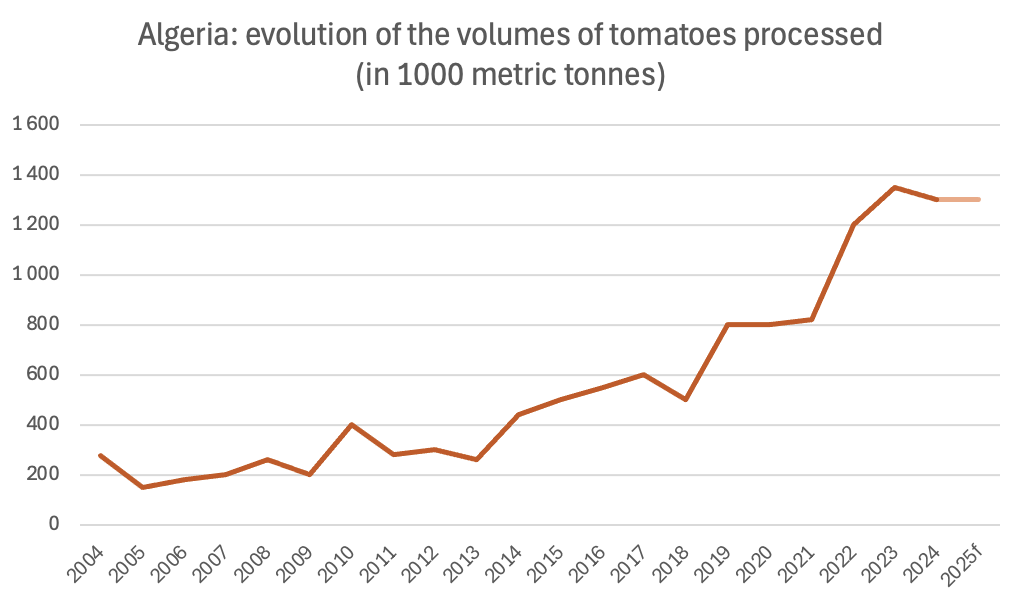

About 50% of this production is consumed fresh while the other half is intended for processing. “1,350,000 tons are processed, including 156,000 to 160,000 tonnes of triple tomato concentrate at 36%,” said Mr. Mazouzi, according to which this production exceeds our needs in this area. “Our needs for tomato concentrate are estimated at 100,000 tonnes,” he said. The estimated surplus of approximately 60,000 tonnes can therefore constitute a stock for periods when production could decline, especially since this product cannot be export-oriented. “We cannot export it, because it is a subsidized product,” explained the president of the tomato interprofession.

The limited processing capacities is often mentioned by producers, especially during the peak of production that extends from mid-June to the end of August of each campaign, according to which all their production does not find a buyer, and that large quantities are sometimes thrown away. This was confirmed by Mr. Mazouzi who says the number of transformation units, of 30, is not sufficient and are above all not well distributed.

The majority of these units, or 75%, are located in the east of the country. The recent opening of the La Belle new canning plant with a daily capacity of 3,300 tonnes (which should increase to 7,800 tonnes in the future) in the Wilaya of Relizane, is a welcome addition but it is still insufficient according to Mazoudi who advocates a better distribution of these transformation units. According to him, it is necessary to create new processing units through the different production poles at the national level and also to opt for small units.

The country remains mostly absent from the world market both for fresh and for processed tomatoes, but there are currently moves towards the development of fresh exportos, notably into Europe. “If we assume that the available statistics on national production are reliable because they come from professionals in the sector and they are confirmed by several sources, the genesis of the failure comes from the national export strategy,” analyzes Finabi Conseil. The firm identifies several ways to correct this situation and initiate an international opening for the export of fresh tomatoes such as “Structure an exportable fresh tomato sector with pilot poles (Annaba, El Tarf, Oued Souf…)“; “Set up a cold chain export and packaging hubs”; “Establish a national traceability and certification system (GlobalG.A.P, HACCP…)”; “Identify target markets: Russia, UAE, Eastern Europe, United Kingdom”.

Regarding processing, the merit of the development of the Algerian industrial tomato sector in recent years goes to farmers, processors but also to the policy of Provisional Additional Safeguard Duties (DAPS) that protect the country from imports. Imported tomato concentrate is subject to taxation that includes customs duties of 30% and DAPS of 120%. This context explains the development of local production and the opening of new processing capacities in the last few years. A local production that today reduces imports from China of triple tomato concentrate in drums which were sometimes re-labeled as European during their passage in Italy.

In Algeria, industrial tomato producers also benefit from a premium of the order of 4 DA per kg, which is in addition to the price paid by the canning plants. This assists producers in covering different costs: land rental, high level of fertilization, purchase of plants, labour for planting and harvesting, irrigation equipment and phytosanitary protection. Some producers mechanize planting and harvesting operations, but this is far from the norm and most of the tomatoes are still harvested by hand. The tomatoes are then transported by farmers on pick-ups to grouping points where the crates are emptied in larger lorries to be delivered to factories. In front of the tomato plant, long lines of trucks are often waiting for their turn meaning some fruit losses or some poor quality.

To increase productivity and reduce production costs, producers multiply innovations. Last May, in Guelma, the daily El Watan reported the disappearance of sprinkler irrigation in favour of more economical drip irrigation. In addition to reducing the water needs of the plot, this technique allows yields from 30 to 80 tonnes per hectare, especially by directly adding fertilizers mixed with water. Another strategy is the mechanization of harvesting or planting operations. In the latter case, the equipment is more accessible.

While companies benefit from the various subsidies that reduce the cost of their raw materials, observers wonder about their efforts to improve their own competitiveness (cost and investment reduction) and to support farmers to improve their productive performance.

The bulk of the 2025 processing season is currently finishing but no serious information on total volumes is available to date.

Sources: FINABI, Jeune Indépendant, TSA, Algérie Eco, El Watan

{kind=link}