News

Global Processed Tomato Market: Foodservice vs. Retail Distribution – Part 2

Part Two: Dimensional Market Analysis

Conducted on the same data provided by Euromonitor, the analysis of the global balance of tomato products highlights the historical hegemony of retail sales, which capture over 70% of volumes compared to out-of-home dining. This global dominance, however, conceals deep geographical and sectoral disparities, characterized by a structural shift in North America and Asia-Pacific toward high-value-added professional models. Driven by much more vigorous future growth rates, foodservice is now establishing itself as the engine of recovery in the face of a retail market that has entered a maturity phase.

Global Balance between Foodservice and Retail Sales

The statistical data collected by Euromonitor show that the global processed tomato market displays contrasting trajectories between foodservice and retail sales.

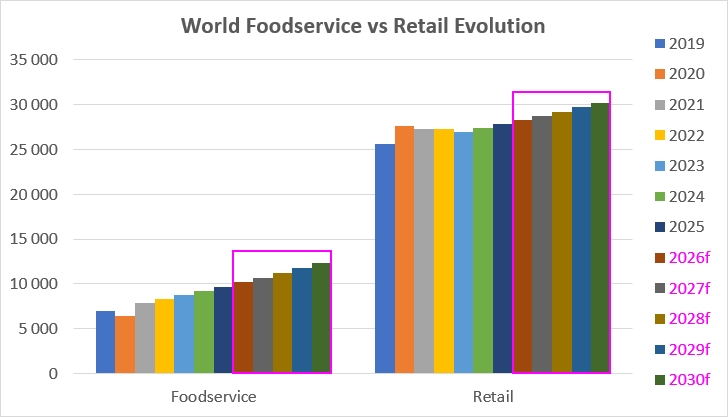

Historically, between 2019 and 2025, out-of-home dining (Foodservice) recorded a significant increase worldwide, with a compound annual growth rate (CAGR) of 5.5%, which brought sector sales from 7.01 to 9.67 million tonnes. In contrast, retail sales, which largely dominate in terms of volume, remained more stable: after a peak in 2020 (27.65 million tonnes), they reached 27.86 million tonnes in 2025, posting a modest CAGR of 1.4%.

Projections for the 2026–2030 period confirm this trend. Out-of-home dining is expected to remain the primary growth driver with a projected CAGR of 4.8%, crossing the 10-million-tonne threshold as early as 2026 to peak at 12.3 million tonnes in 2030. Meanwhile, retail sales are anticipated to continue their linear progression at a pace of 1.6% per year, and should rise from 28.3 million tonnes in 2026 to 30.17 million tonnes in 2030.

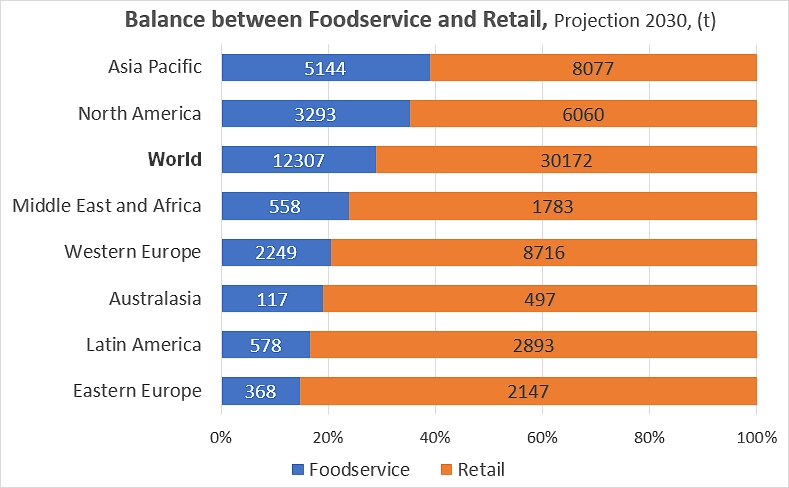

An examination of the geographical distribution of the processed tomato market by 2030 highlights stark regional contrasts. On a global scale, retail stands out as the primary commercial channel, capturing 71% of volumes compared to 29% for out-of-home dining.

This dominance of retail distribution is particularly overwhelming in Eastern Europe and Latin America, where the sector captures 85% and 83% of volumes, respectively. Conversely, Asia-Pacific distinguishes itself as the region where fast food and commercial foodservice are most deeply entrenched, with the latter sector reaching a record 39% market share (5.14 million tonnes) compared to 61% for retail sales. North America follows a similar trend, with a strong foodservice penetration at 35% (3.29 million tonnes). Western Europe and the Middle East/Africa region sit in an intermediate position, showing a breakdown closer to the global average, with a retail sector oscillating between 76% and 79%. Ultimately, the weight of out-of-home dining proves to be significantly more prominent in North American and Asian economies.

An analysis of the compound annual growth rates (CAGR) collected—and projected—by Euromonitor highlights a global and widespread acceleration of the out-of-home dining sector compared to retail sales. At the global level, Foodservice is expected to see its annual growth rise from 0.6% over the historical period (2019-2025) to a solid 4.0% over the projection period (2026-2030), while retail sales are expected to display near-perfect stability, oscillating between 1.4% and 1.6%.

This catch-up or acceleration dynamic in Foodservice is observed in almost all regions. Asia-Pacific outperforms all other zones with a spectacular historical growth of 15.5% for foodservice, which should normalize to a still very high rate of 7.0% for 2026-2030, far ahead of retail distribution (1.5%). Regions like Eastern Europe, Latin America, and Australasia, which had recorded negative growth rates for out-of-home dining between 2019 and 2025 (ranging from -0.4% to -3.0%), are expected to see trends reverse radically: growth in Eastern Europe and Latin America should follow annual paces of 5.5% and 5.0% respectively for foodservice by 2030, clearly outstripping their corresponding retail markets.

The Middle East and Africa stand out with solid vitality in both sectors for the 2026-2030 period, with Foodservice expanding at a steady pace of 5.2% per year and retail sales at 4.3%. Finally, in North America and Western Europe, markets are more mature but should confirm the trend: foodservice sales are expected to grow faster than retail sales, particularly in North America where the latter are projected to stagnate at 0.4% while foodservice sales should grow at a rate of 3.2% per year.

Regional Foodservice/Retail Balance by Product in 2025

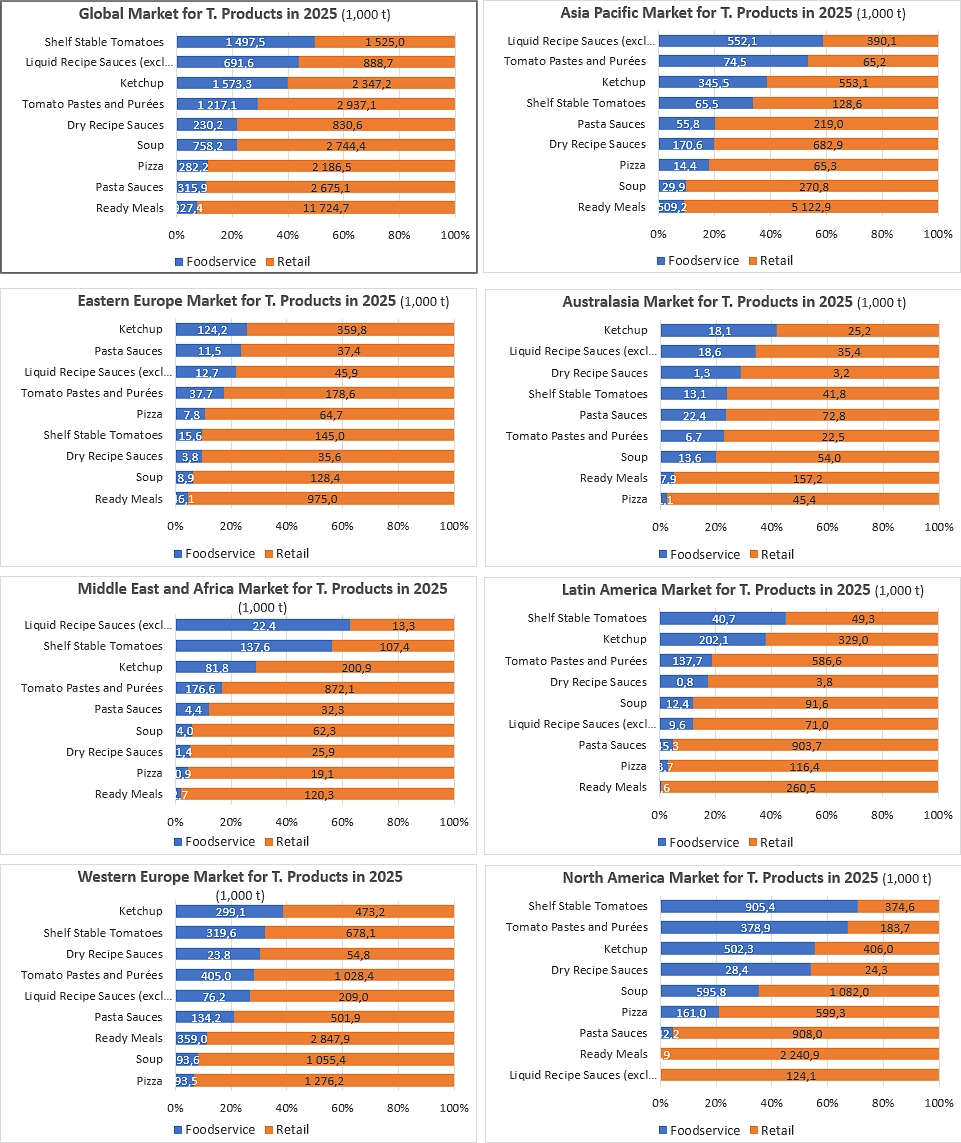

An in-depth analysis of Euromonitor statistics makes it possible to precisely quantify market dynamics and local balances for the year 2025. In a consolidated global market of 35.35 million tonnes, the retail sales sector captures a hegemonic share of 78.8% (27.86 million tonnes) compared to 21.2% in out-of-home dining (7.5 million tonnes). The global balance is thus established at a ratio of 3.7 tonnes sold in stores for every tonne consumed in foodservice. This general gap is explained by the fact that tomato, in its highly processed forms, is primarily a domestic convenience product, while foodservice relies more on less elaborate, or even raw, ingredients, or accompanying condiments. The Foodservice/Retail balance by product shows that the ready meals segment literally crushes the international market by its mass (12.65 million tonnes in total) and displays the most pronounced imbalance in favor of retail distribution, which absorbs 92.7% of it (11.73 million tonnes compared to only 0.93 million tonnes in foodservice). Pasta sauces and pizzas follow a similar convenience logic, with retail sales holding 89.4% (2.67 million tonnes) and 88.6% (2.19 million tonnes) of market shares, respectively. At the other end of the spectrum, the canned tomato market proves to be perfectly balanced with 1.498 million tonnes in Foodservice against 1.525 million tonnes in retail sales, representing a near-perfect balance of 49.6% versus 50.4%.

Ketchup, for its part, confirms its nature as a strategic product for fast food and table dining: it is the most voluminous finished product in the global foodservice sector with 1.573 million tonnes, claiming 40.1% of its category.

The regional breakdown shows that North America completely redefines the standards of the commercial balance. Out of a total regional market of 8.56 million tonnes, Foodservice represents 30.6% (2.615 million tonnes), which is the highest rate in the world. The shift in favor of out-of-home dining is spectacular there for canned tomatoes, where Foodservice wins out at 71.7% (0.905 million tonnes compared to 0.375 million tonnes for the retail sector), as well as for tomato pastes and purées where it corners 67.3% of volumes (0.379 million tonnes compared to 0.184 million tonnes). North America is also the only geographical area where ketchup is mostly consumed at restaurants (55.3% of the regional market, or 0.502 million tonnes). This model stands in stark contrast to that of Eastern Europe, whose total market of 2.24 million tonnes is locked at 88.0% by retail sales (1.97 million tonnes), reflecting a habit of home culinary preparation and a marginal reliance on foodservice for ready meals (46,000 t) or sauces.

Asia-Pacific positions itself as the giant of the retail sector with 7.5 million tonnes out of a total of 9.32 million tonnes (80.5%). The region alone shapes the global trend for store-bought ready meals by selling 5.12 million tonnes. A unique fact in the Euromonitor landscape, it is also the only region where liquid sauces lean toward foodservice (0.55 million tonnes compared to 0.390 million tonnes in retail sales), highlighting the intensive use by local professionals of ready-to-use liquid sauce bases. With 9.93 million tonnes, Western Europe establishes itself as a highly important mature market, characterized by a very powerful retail sector for pizzas (1.28 million tonnes) and soups (1.055 million tonnes), while its foodservice sector maintains a major industrial base for tomato pastes and purées (405,000 t) for kitchen preparation.

Finally, Latin America and the Middle East/Africa region illustrate other forms of relationship with tomato derivatives. The Middle East and Africa stand out with an impressive volume of tomato pastes and purées (1.05 million tonnes in total), of which 83.1% (872,000 t) are purchased in retail stores, confirming that tomato paste is a basic necessity in daily household diets in these regions. Latin America highlights an extreme polarization toward retail pasta sauces (904,000 t) compared to a local Foodservice sector that is virtually non-existent in this segment (45,000 t), while retaining solid retail sales dynamics for its pastes (587,000 t) to support a deeply entrenched traditional home cooking culture.

Foodservice/Retail Balance by Product, for each Region, in 2025

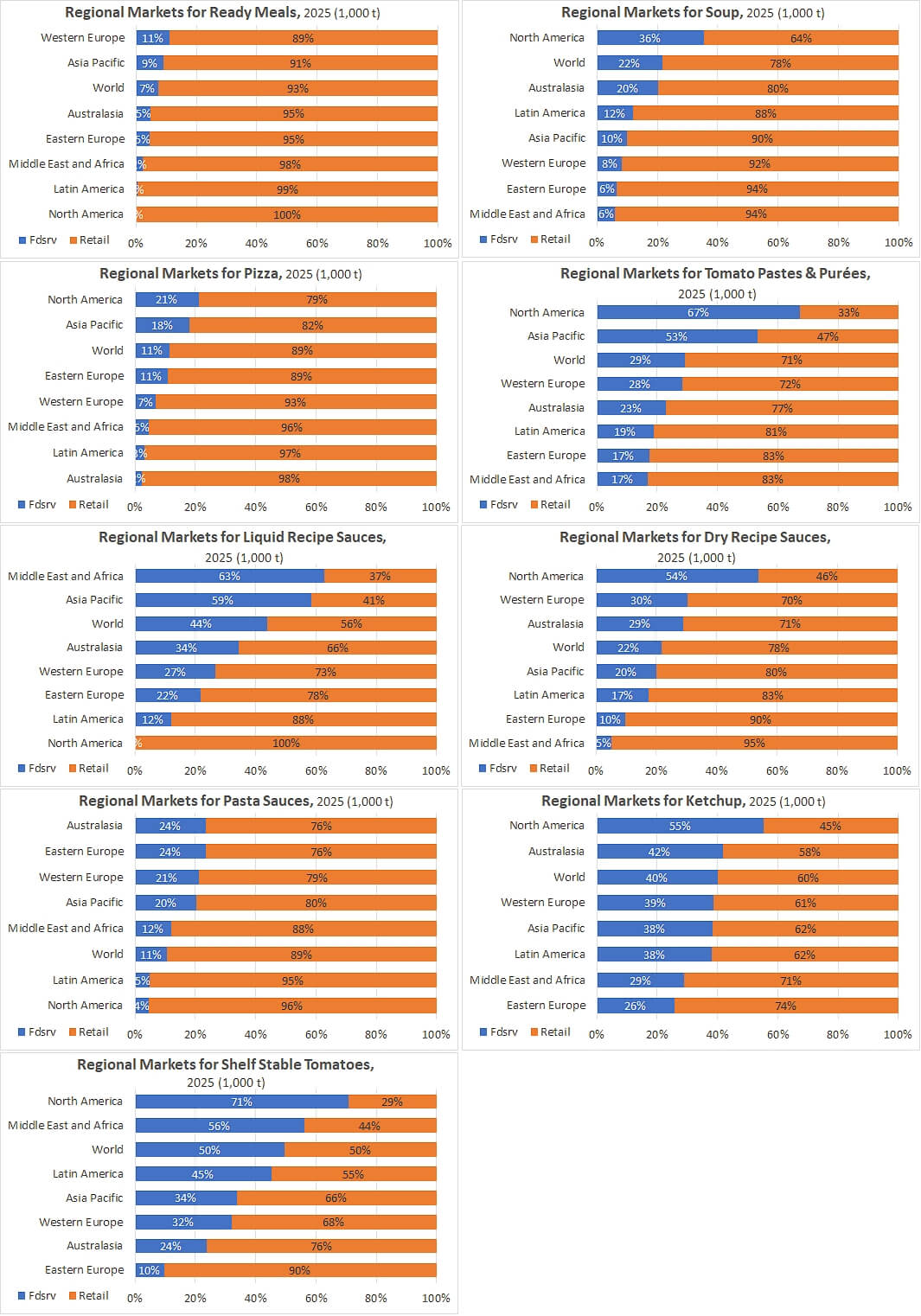

The global balance between out-of-home dining and retail sales is heavily dictated by pure household convenience segments, with Foodservice only managing to balance or dominate in very specific categories of low-processing derivatives or accompanying condiments.

The ready meals segment displays the most marked imbalance in the global market in favor of retail sales, which corner 92.7% of volumes, representing 11.73 million tonnes out of a total of 12.65 million. This ultra-favorable balance for retail is particularly evident in Asia-Pacific with 5.12 million tonnes in the retail sector compared to 0.51 million in out-of-home dining, and in North America with 2.24 million tonnes in retail sales against a negligible amount in foodservice. Pasta sauces and pizzas follow a similar dynamic of strong domestic penetration, with the balance leaning toward the retail sector at 89.4% for sauces (2.68 million tonnes out of 2.99) and 88.6% for pizzas (2.19 million tonnes out of 2.47). In Western Europe, for instance, the balance for pizzas stands at 1.28 million tonnes for retail sales compared to only 0.09 million tonnes in out-of-home dining.

The soup category also features a balance clearly dominated by retail distribution globally, which captures 2.74 million tonnes out of a total of 3.50 million. North America, however, brings an important nuance to this segment with a notable foodservice penetration of 0.60 million tonnes compared to 1.08 million tonnes in retail sales. Regarding dehydrated sauces, the retail sector retains a wide global lead with 0.83 million tonnes out of 1.06 million, driven mainly by household consumption in Asia-Pacific (0.68 million tonnes). Liquid sauces show a more nuanced global balance (0.89 million tonnes in retail sales compared to 0.69 million in foodservice), but Asia-Pacific creates a major exception here by reversing the balance in favor of out-of-home dining, with 0.55 million tonnes in foodservice compared to 0.39 million tonnes in retail sales.

The tomato pastes and purées segment generates a substantial global volume of 4.15 million tonnes, where retail sales remain the majority at 70.7% with 2.94 million tonnes. The balance here is sustained by domestic consumption in Western Europe and the Middle East and Africa, with the latter zone alone absorbing 0.87 million tonnes in retail sales compared to 0.18 million tonnes in foodservice. Conversely, North America completely reverses the balance of this category in favour of professional uses, with the foodservice sector consuming 0.38 million tonnes compared to 0.18 million tonnes for the retail sector.

Ketchup establishes itself as the major processed product of commercial foodservice, posting one of the highest foodservice market shares with 40.1% of global volumes, representing 1.57 million tonnes out of the 3.92 million in the category. The balance even shifts predominantly in favor of foodservice in North America, where Foodservice outpaces retail sales with 0.50 million tonnes compared to 0.41 million. In Europe (Western and Eastern) as well as in Asia-Pacific, the balance remains to the advantage of the retail sector, but foodservice volumes remain very solid, reaching 0.30 and 0.35 million tonnes, respectively.

Finally, the canned tomato segment constitutes the perfect equilibrium point of the global market, with a nearly equal balance of 49.6% in foodservice (1.50 million tonnes) compared to 50.4% in retail sales (1.53 million tonnes). This global parity conceals a radical geographical divide between North America, where foodservice crushes the retail sector at 71.7% (0.91 million tonnes compared to 0.38 million), and Eastern or Western Europe, where the balance leans heavily toward retail stores, reaching, for example, 0.68 million tonnes in retail sales compared to 0.32 million in out-of-home dining for the Western European market.

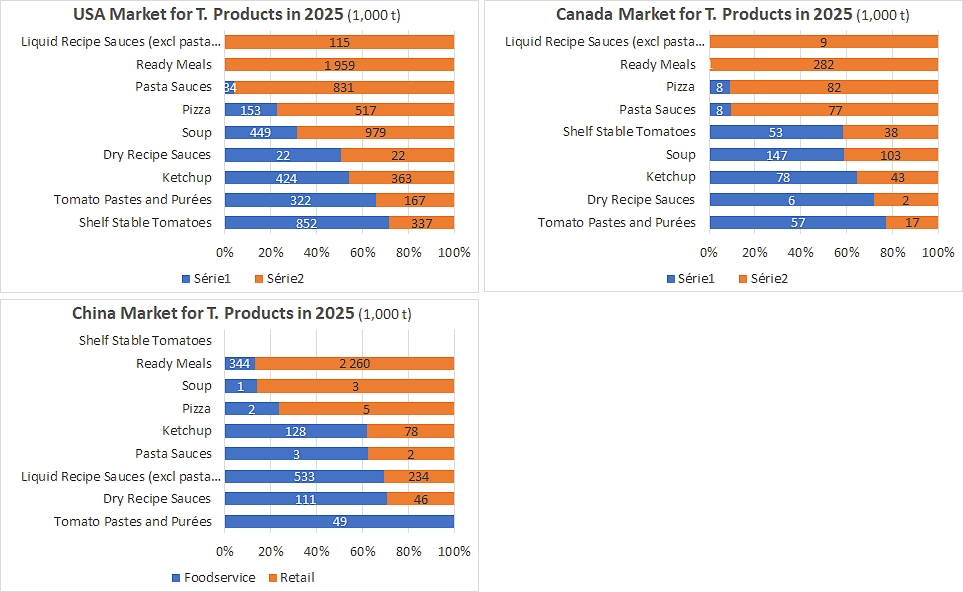

A few national examples in 2025

In the United States, the tomato derivatives market stands out for its considerable volumes and a particularly solid out-of-home activity. Out of a substantial combined total volume, the retail channel dominates with 5.29 million tonnes, while foodservice maintains a remarkable foundation of 2.26 million tonnes, which is one of the highest ratios in favor of foodservice in the Euromonitor panel. Within the American foodservice network, demand is massively driven by canned tomatoes, which reach 0.85 million tonnes, followed closely by soups at 0.45 million tonnes, ketchup with 0.42 million tonnes, and tomato pastes and purées at 0.32 million tonnes. Conversely, the retail channel in the United States is overwhelmed by ready meals, which account for a cumulative 1.96 million tonnes sold, followed closely by soups (0.98 million tonnes) and pasta sauces (0.83 million tonnes). Canada, its neighboring country, displays a proportionally similar market structure but on a smaller scale, with a retail sector of 0.65 million tonnes dominated by ready meals at 0.28 million tonnes, and a commercial foodservice sector of 0.36 million tonnes primarily driven by soup with 0.15 million tonnes.

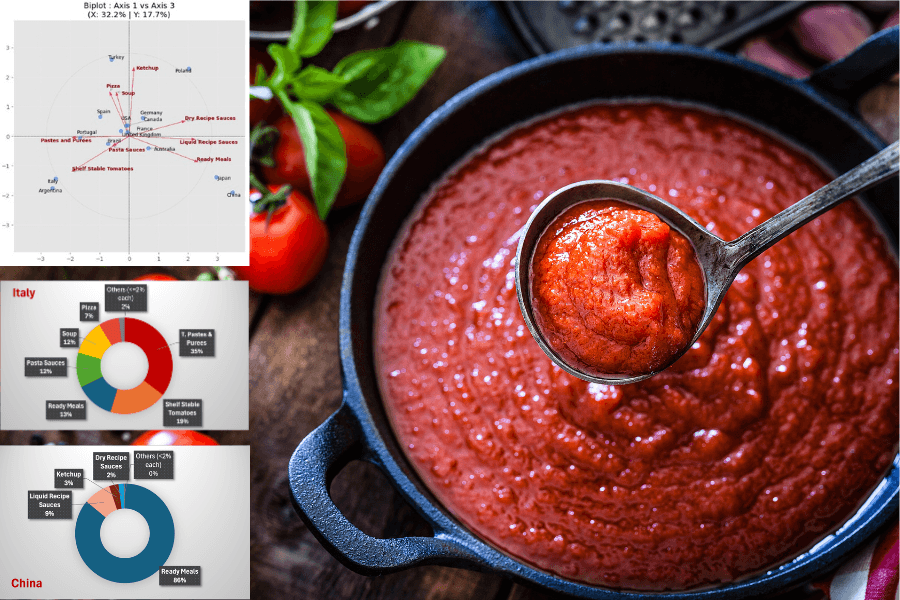

In China, purchasing dynamics reveal a very large-scale market where retail significantly outperforms commercial foodservice. The retail sector accounts for the bulk of the activity there with 2.63 million tonnes, while foodservice represents 1.17 million tonnes. An examination of products within out-of-home dining in China shows a strong presence of liquid sauces, which peak at 0.53 million tonnes, complemented by 0.34 million tonnes of ready meals. On the retail sales side of the Chinese market, consumption is almost exclusively focused on the ready meals segment, which posts a colossal volume of 2.26 million tonnes, completely eclipsing all other processed tomato product categories.

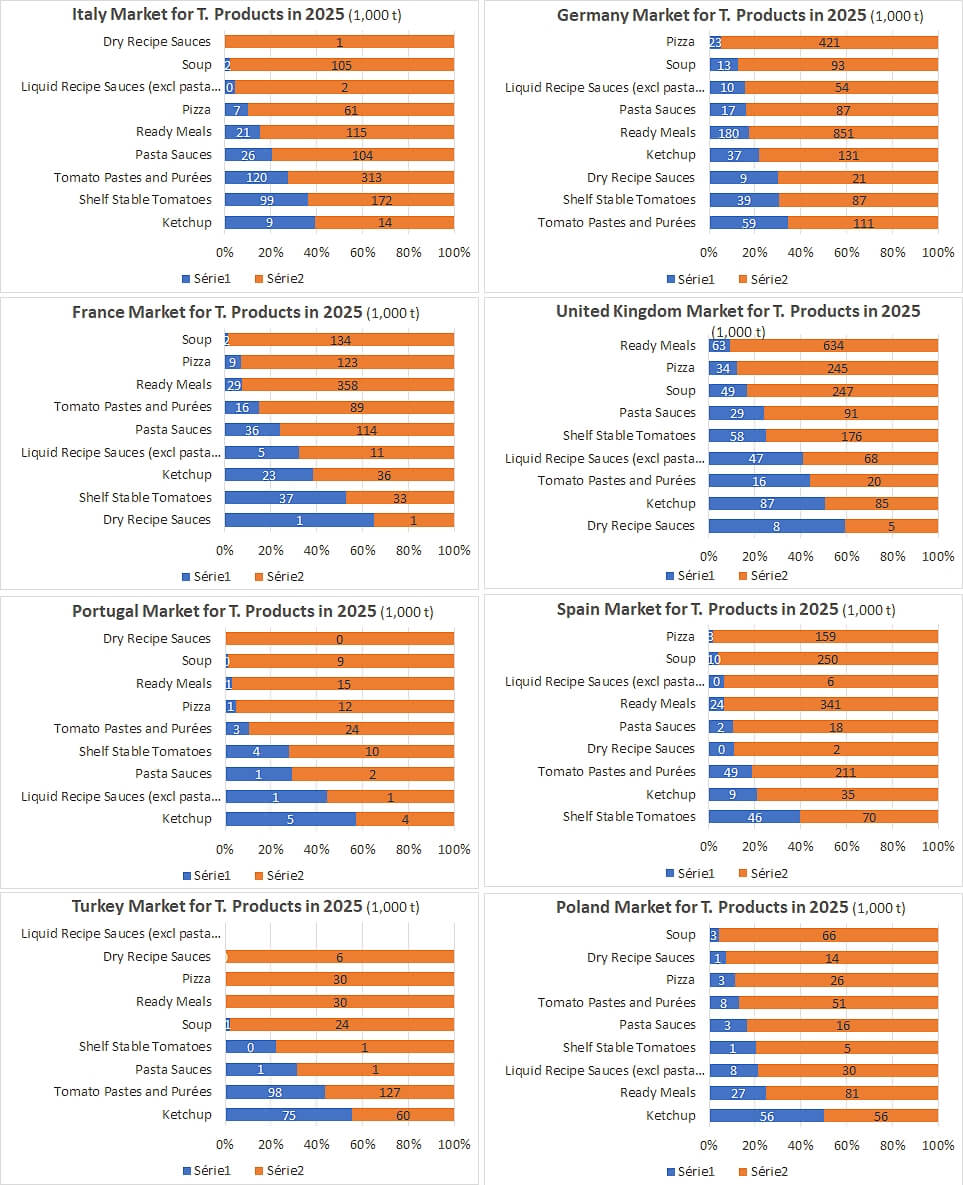

In Europe and its direct area of influence, the analysis of major markets such as Germany, Italy, and the United Kingdom highlights contrasting distribution balances, deeply shaped by local culinary cultures. In Germany, the retail sector largely dominates with 1.86 million tonnes compared to 0.39 million tonnes for foodservice, a market strength driven in stores by 0.85 million tonnes of ready meals and 0.42 million tonnes of pizzas. Italy presents a profile more oriented towards traditional ingredients, with a balance of 0.89 million tonnes in retail sales compared to 0.28 million tonnes in out-of-home dining; tomato paste and purée occupy a hegemonic position there, representing the leading category in foodservice with 0.12 million tonnes and soaring to 0.31 million tonnes in household kitchens. In the United Kingdom, where the retail sector leads the way with 1.57 million tonnes compared to 0.39 million tonnes in foodservice, habits are structured around store sales of ready meals at 0.63 million tonnes, while ketchup illustrates a perfect balance between the two distribution channels, selling roughly 0.09 million tonnes both among restaurateurs and private individuals. France and Spain confirm this strong European habit of retail purchases with 0.90 and 1.09 million tonnes respectively, driven by ready meals or pastes, compared to a modest foodservice sector of 0.16 and 0.15 million tonnes. Portugal and Poland follow a comparable logic, with the Polish market posting retail sales of 0.34 million tonnes (including 0.08 million of ready meals) against 0.11 million tonnes in foodservice, while Turkey stands out with very high volumes of tomato paste both in retail sales (0.13 million tonnes) and in foodservice (0.10 million tonnes).

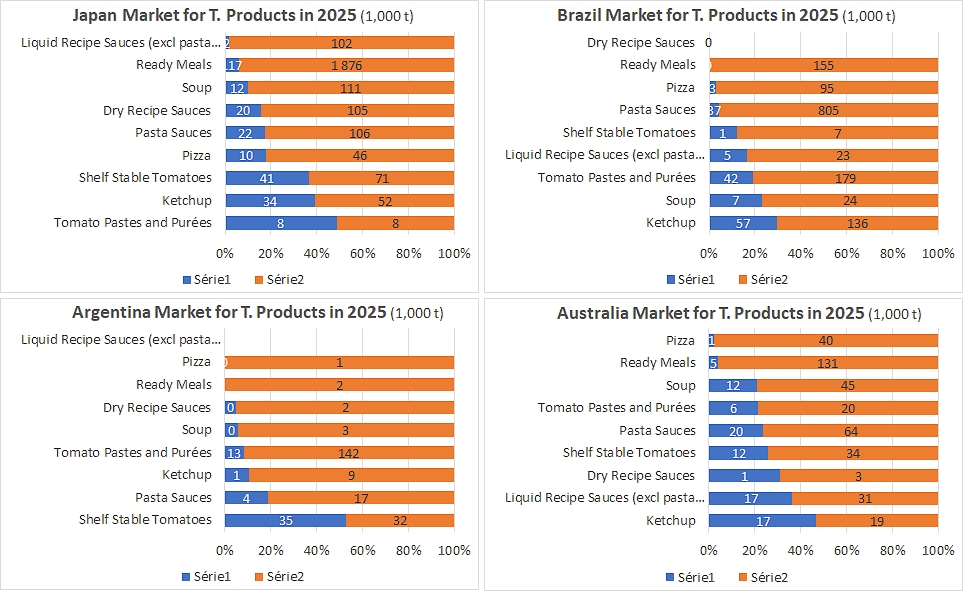

For their part, Japan and Brazil illustrate situations of extreme polarization where the retail channel captures almost all industrial volumes. In Japan, the retail sector dominates spectacularly with 2.48 million tonnes compared to a marginal commercial foodservice sector that draws only 0.27 million tonnes; this balance is the direct result of the ready meals segment, which alone absorbs 1.88 million tonnes in stores. Brazil displays a similar configuration, characterized by significant retail sales of 1.42 million tonnes compared to a foodservice sector limited to 0.15 million tonnes, where the balance is almost entirely locked in by pasta sauces purchased in supermarkets to the tune of 0.81 million tonnes. Argentina shares this heavily retail-oriented Latin American profile with 0.21 million tonnes, dominated by 0.14 million tonnes of tomato pastes and purées, compared to an out-of-home dining sector that draws just 0.05 million tonnes. For its part, Australia aligns closely with these mature dynamics, with retail sales of 0.39 million tonnes led by ready meals (0.13 million tonnes), against a much lower foodservice channel standing at a modest 0.09 million tonnes.

For details on the Euromonitor product categories, click here.

Source: Euromonitor

{kind=link}