News

Euromonitor: The French Tomato Products Market

French tomato products market: growth leaves the kitchen for the restaurant

The French tomato products market is shifting from inflation-driven growth toward stable consolidation, stalled by a pricing glass ceiling. While households have long favored raw ingredients to save money, the 2030 horizon marks a balance between authenticity and convenience. Most notably, in the face of a saturated retail market, Foodservice is becoming the exclusive engine of growth: disrupted by the rise of “uberization,” tomatoes are being cooked less at home and are now consumed in restaurants.

An examination of Euromonitor’s historical and prospective data for the French tomato derivatives market between 2019 and 2030 reveals profound structural changes, characterized by a clear shift in growth drivers between the first and second halves of the period under review.

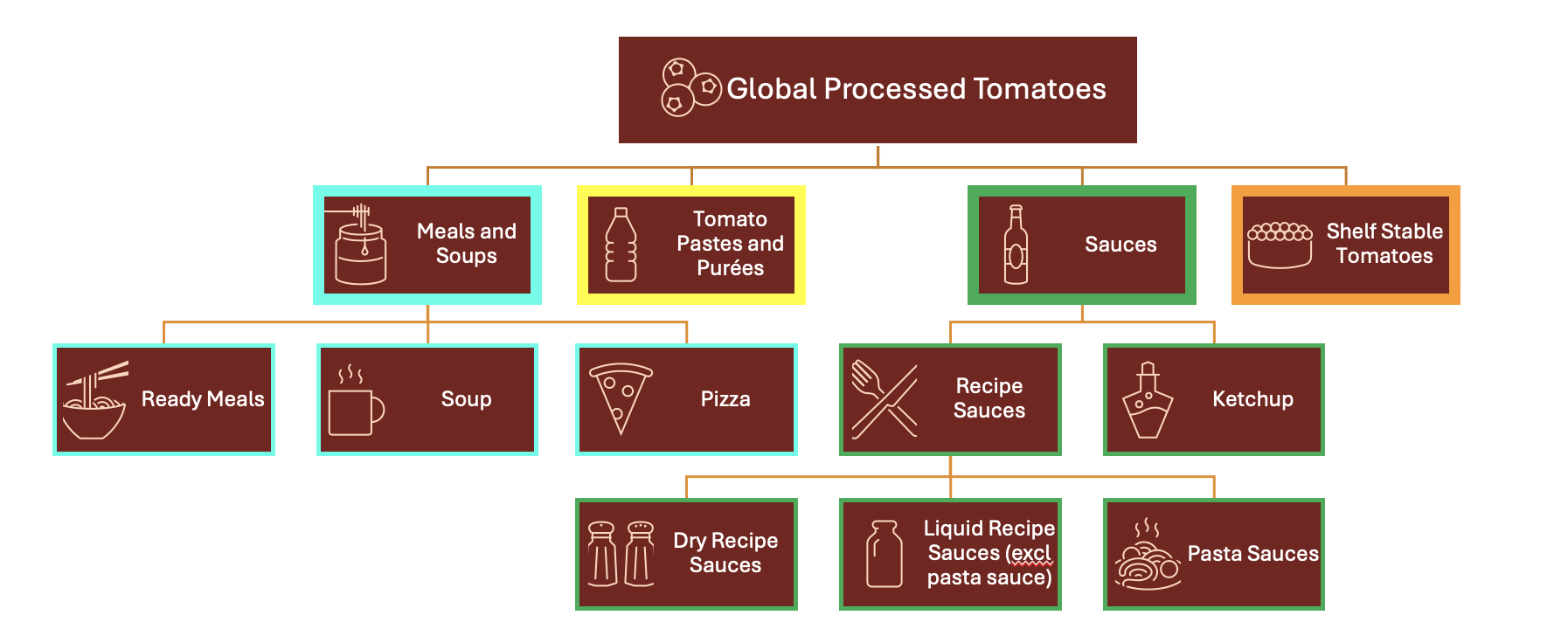

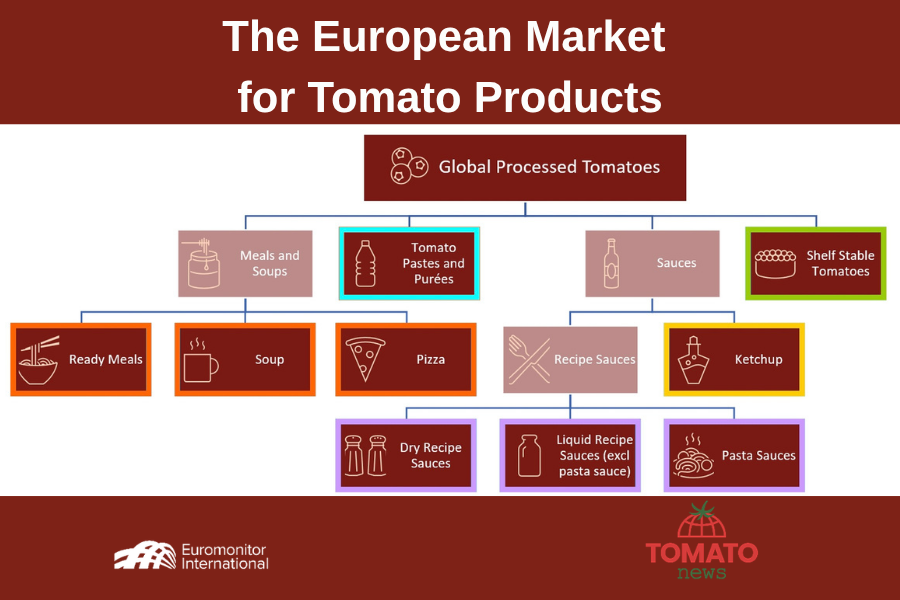

The different categories and sub-categories of the global processed tomato market (Source: Euromonitor)

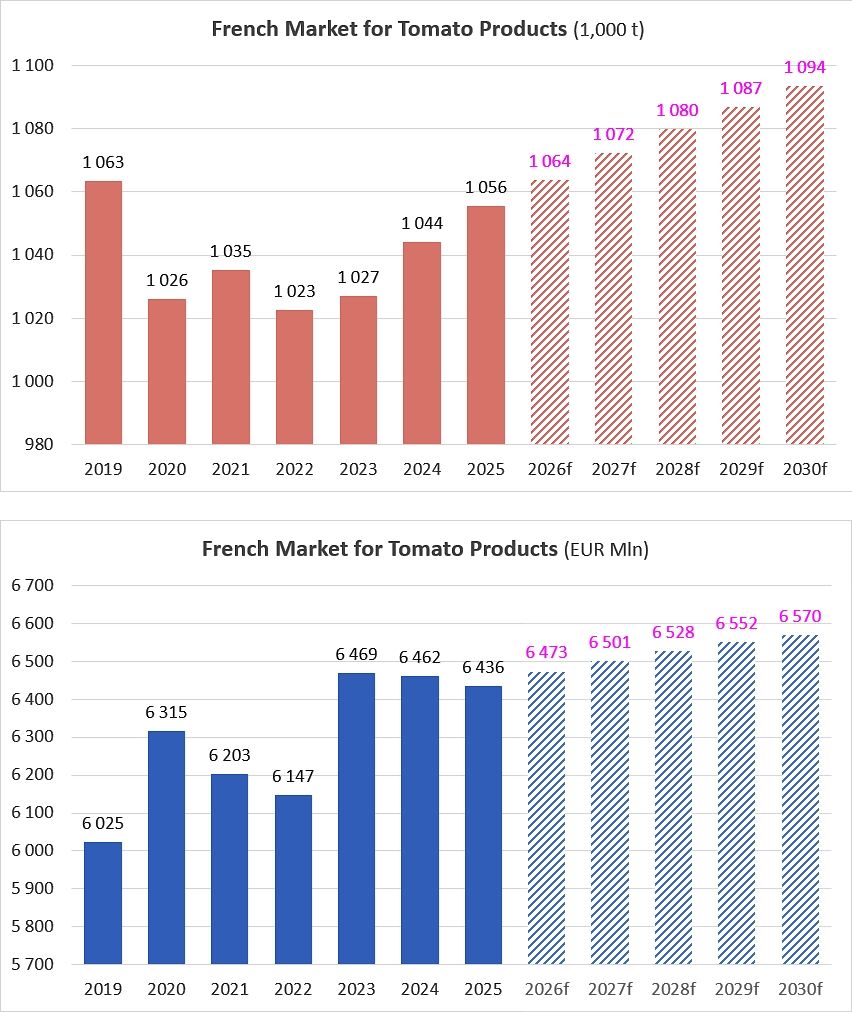

The analysis of the historical phase, spanning from 2019 to 2025, highlights a blatant disconnect between the evolution of consumed volumes and the overall market value. On the volume side, the market demonstrates advanced maturity, or even a slight erosion, dropping from 1.063 million tonnes to 1.056 million tonnes, which translates into a negative compound annual growth rate (CAGR) of -0.12%. This decline is, at least in part, linked to the highly disrupted consumption patterns during and immediately following the Covid pandemic period.

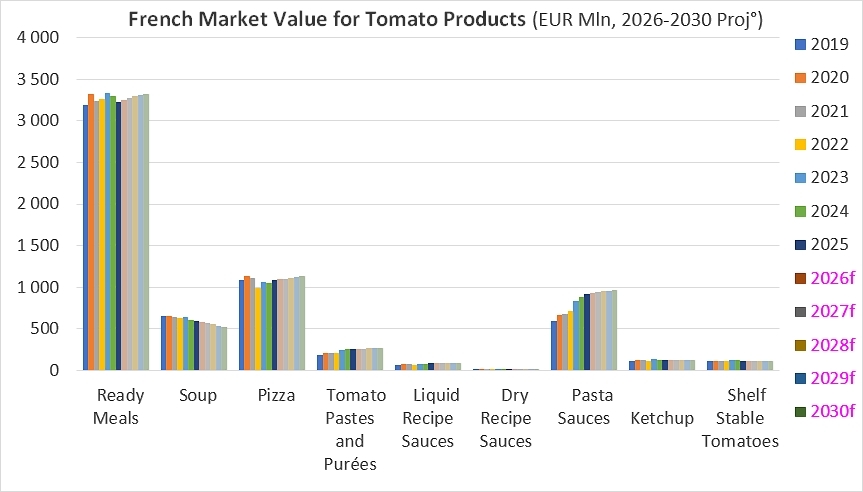

Conversely, the total market value at retail prices progressed continuously over this same period, climbing from €6.025 billion to €6.436 billion, representing an average annual growth rate (CAGR) of 1.11%. This asymmetrical pattern is explained by a predominant price effect, directly linked to global and sector-specific inflationary pressures: the rising costs of agricultural raw materials, combined with skyrocketing costs for energy and packaging materials such as glass or tinplate, forced operators to increase their prices. The market’s historical growth was therefore driven by value and fueled by inflation, with consumers overall paying more for slightly lower volumes.

Projections for the 2026–2030 period outline a radically different trajectory, signaling a complete reversal of consumption and pricing dynamics. Sales volumes of industrial tomato derivatives are expected to enter a firm and steady recovery phase, growing from 1.064 million tonnes in 2026 to 1.094 million tonnes by the 2030 horizon, thereby posting a positive compound annual growth rate (CAGR) of 0.69%. At the same time, market value is expected to continue rising, peaking at €6.570 billion in 2030, but its growth rate is likely to slow down sharply, settling at an average annual rate of just 0.37%. This marked slowdown in value, when viewed alongside the recovery in volumes, points to an expected normalization of consumer prices and a cooling down of inflation. It also suggests tighter budget trade-offs by French households, who are likely to shift toward more affordable products, family packs, or private labels, thereby limiting the sector’s overall financial expansion in favor of a return to volume-driven convenience shopping.

Product Breakdown

A detailed analysis of the French tomato derivatives market by product category helps explain which segments caused the historical stagnation in overall volumes and which are expected to drive the anticipated rebound by 2030. Examining the data highlights highly contrasting trajectories based on the level of product processing and household consumption habits.

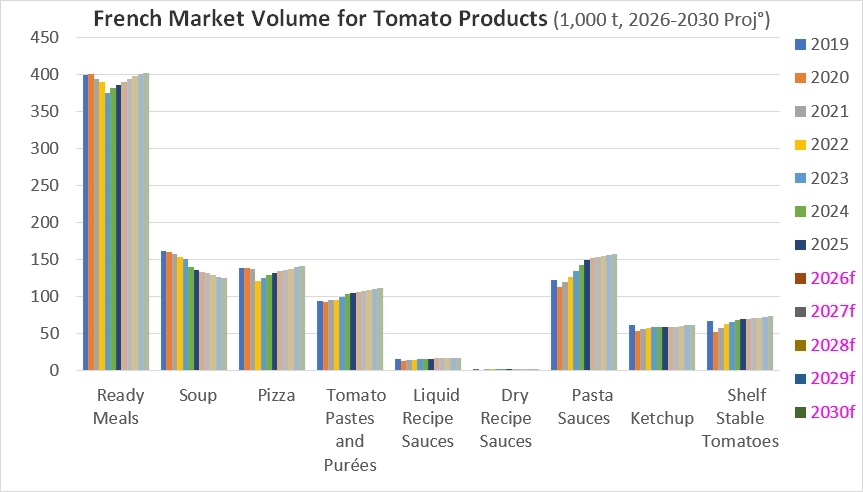

Observation of the historical period (2019–2025) shows that the slight overall decline in volumes (-0.12% per year) was largely driven by the structural decline of two major market pillars. The soup segment suffered a severe and continuous drop, plunging from 161,000 tonnes in 2019 to 136,000 tonnes in 2025, representing a sharp average annual decline of -2.79%. Meanwhile, the ready meals market, which nonetheless represents the largest volume outlet with nearly 400,000 tonnes, also contracted at a rate of -0.55% per year. The fresh or frozen pizza segment followed a similar trend, falling by -0.80% per year to settle at 132,000 tonnes in 2025. These significant declines in complex or pre-prepared products reflect a relative shift away from these industrial solutions during the period.

Conversely, basic ingredients and cooking aids sustained the historical market. Pasta sauces showed outstanding health with an average annual growth of 3.40%, jumping from 122,000 to 149,000 tonnes, driven by a return to quick and economical home cooking. Following the same logic, tomato paste and purees grew strongly at a rate of 1.88% per year, rising from 94,000 to 105,000 tonnes, while shelf stable tomatoes (canned tomatoes) edged up by 0.39% per year. For their part, table sauces such as ketchup remained generally stable with a slight downward trend (-0.77%).

Projections for the 2026–2030 period signal a complete shake-up of this sectoral hierarchy, as nearly all declining categories are expected to begin a technical or structural recovery cycle, driving the overall market rebound to 0.69% per year. The most dramatic turnaround involves pizzas, whose volumes are projected to bounce back at a dynamic pace of 1.32% per year to reach 141,000 tonnes in 2030. Similarly, ready meals are expected to reverse their trend and return to positive growth of 0.78% per year, once again crossing the 400,000-tonne mark by the end of the period. With the notable exception of soups, which continue their inexorable decline albeit at a slower pace (-1.74% per year to end at 125,000 tonnes), tomato derivatives that offer convenience and time savings seem to be regaining consumer favor in the forecasts.

Finally, Euromonitor data shows that traditional grocery segments will consolidate their gains and align with uniform, solid growth trajectories: tomato paste and purees are expected to maintain a robust growth of 1.39% per year. Pasta sauces, following a phase of rapid expansion, will enter an era of stable maturity with more moderate but positive growth of 0.93% per year (reaching 157,000 tonnes in 2030). Shelf stable tomatoes (1.26% per year) and ketchup (1.37% per year) are also projected to see an acceleration in their volumes compared to the historical period.

Foodservice vs. At-Home Consumption

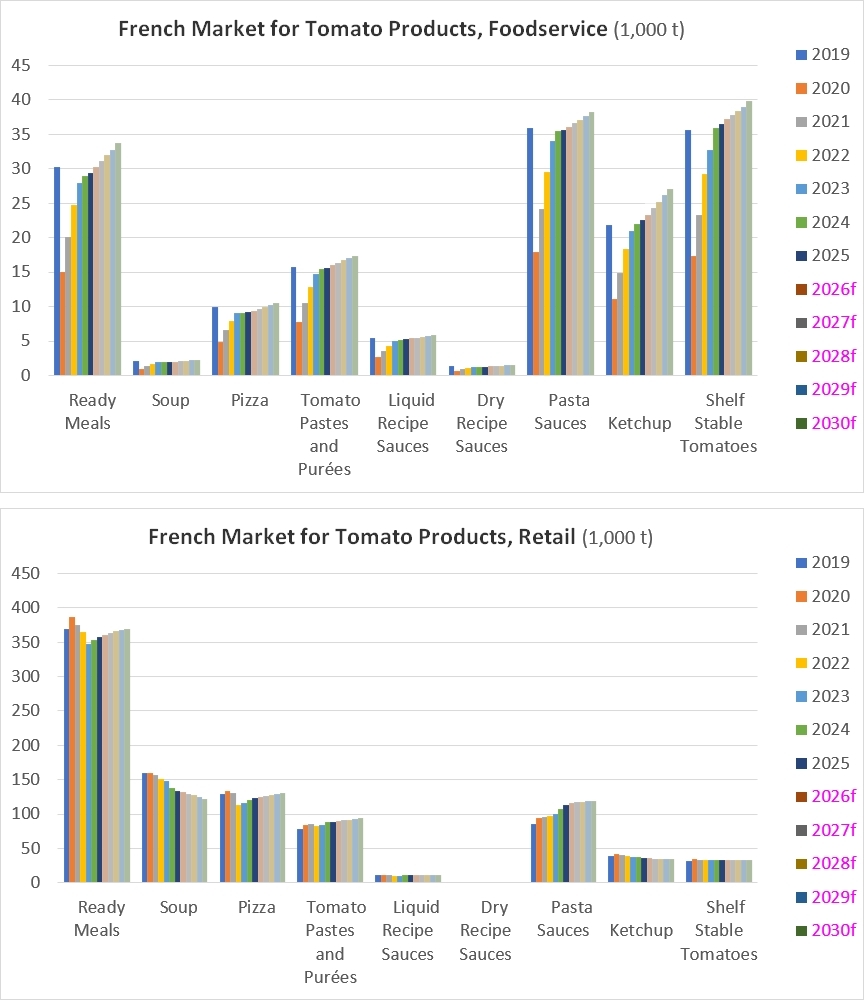

A comparative examination of distribution channels in the French tomato derivatives market between 2019 and 2030 reveals deeply divergent consumption patterns between foodservice and at-home household consumption. These two channels, while subject to the same macroeconomic uncertainties, react according to their own timelines and intensities.

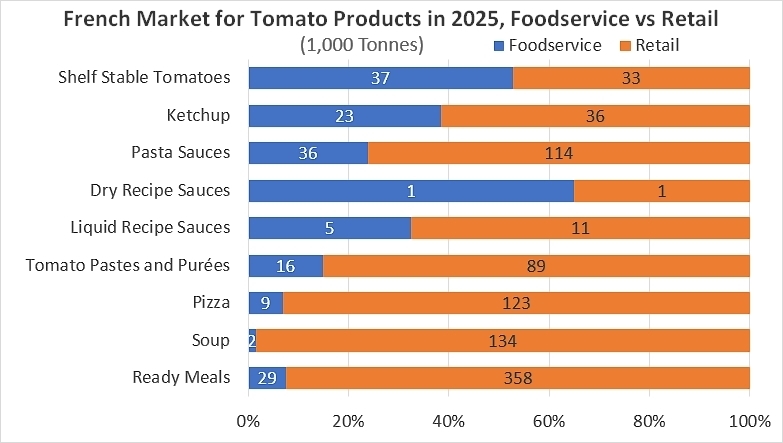

The analysis of the historical period (2019–2025) remains structurally shaped by the shock of 2020, which caused significant volume shifts between the two channels: in 2020, health-related lockdown measures and restaurant closures caused an immediate and massive collapse of the Foodservice channel, whose overall volumes were cut in half, plunging from 158,000 to 79,000 tonnes. Conversely, the Retail channel captured part of this shift toward at-home consumption, jumping from 905,000 to 948,000 tonnes in a single year, driven by the rise of family meals and culinary bases like pasta sauces, which recorded a spectacular, historic growth of 4.73% per year across the entire period.

Despite this initial shock, the post-crisis normalization phase shows a gradual but uneven catch-up dynamic depending on the products considered. In terms of overall volume, Foodservice had almost completely returned to its pre-crisis level by 2025 (157,000 tonnes, representing a nearly flat compound annual rate of -0.09% over 2019–2025), while Retail saw its volumes slowly erode after the 2020 peak to settle at 898,000 tonnes in 2025, posting an average annual decline of -0.13%. By category, this historical period shows a marked decline in soups across both channels, whereas basic or raw ingredients like tomato paste and purees performed strongly in Retail (+2.26% per year) to meet the deep-rooted habit of home cooking.

Projections for the 2026–2030 period outline a clean break and signal a complete reversal of growth drivers, with the out-of-home dining channel becoming the market’s true accelerator. Foodservice is expected to experience a rapid expansion phase generalized across all product categories, posting a vigorous average annual growth of 2.28% to reach 176,000 tonnes in 2030. This vitality will be particularly driven by the ketchup segment, which is projected to jump by 3.75% per year, as well as by flagship products of fast food and Italian dining, such as pizzas (+2.81% per year) and ready meals (+2.78% per year). Restaurateurs and food chains are heavily reinvesting in tomato derivative products to meet a growing demand for social dining and on-the-go food options.

On the retail trade side, forecasts for 2026–2030 point toward a much more moderate and cautious growth, established at 0.40% per year in overall volume to reach 917,000 tonnes in 2030. Following the “home cooking” excitement of previous years, pasta sauces are entering an advanced maturity phase with growth limited to 0.77% per year. Ketchup and soups continue their decline on supermarket shelves, while categories associated with quick and economical meal solutions, such as pizzas (+1.20% per year) and paste (+1.23% per year), maintain a positive direction.

Per Capita Sales by Product Category

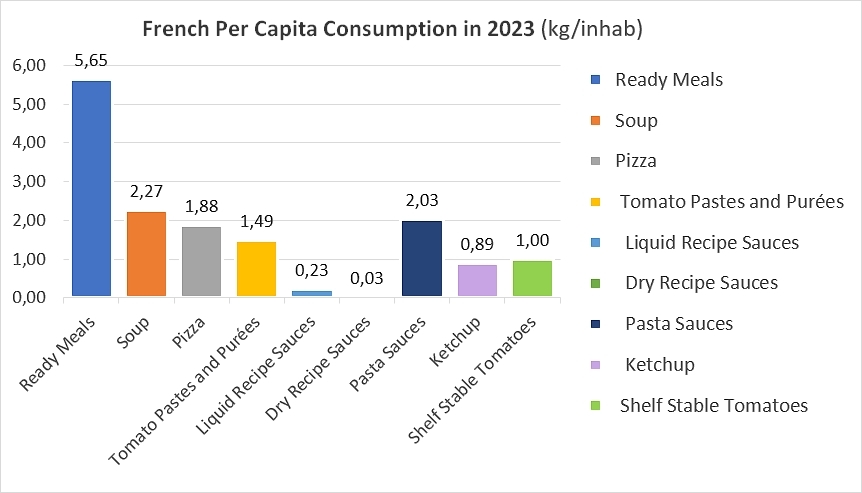

The analysis of per capita consumption volumes in the French tomato derivatives market between 2021 and 2025 highlights individual consumer trade-offs in a shifting economic landscape, shaped by the previously mentioned dynamics of eroding purchasing power and the rationalization of food spending. Observing individual data helps explain how the overall maturity of the market translates concretely into the average French consumer’s plate.

The first striking observation concerns the clear dominance of ready meals in individual consumption habits, although this segment is showing slight signs of fatigue. An average French consumer eats between 5.6 and 6.0 kilograms of tomato-based ready meals per year. This high level is explained by the central role that quick meal solutions, such as lasagna or microwaveable dishes, play in the daily lives of working professionals. However, per capita consumption appears to have eroded slightly, dropping from 6.0 kg in 2021 to 5.65 kg in 2023, before experiencing a modest stabilization estimated at around 5.8 kg for 2025. This initial decline is part of an underlying trend characterized by a negative compound annual growth rate of -0.77% over the entire historical period. This could reflect a consumer trade-off in favor of traditional basic solutions, at the expense of industrial options that were more expensive or perceived as ultra-processed at the height of the inflationary crisis.

In the same vein, processed product categories such as soups and pizzas show a structural decline in individual consumption. Tomato-based soups recorded the most marked slowdown, with per capita consumption plunging from 2.4 kg in 2021 to an estimated 2.0 kg for 2025, representing a sharp average annual decline of -3.84% (CAGR). For their part, pizzas posted a decline of -1.21% per year, slipping from 2.1 kg per capita in 2021 to 1.88 kg in 2023, before stabilizing at around 2.0 kg in 2025. These shifts confirm that household budget trade-offs primarily penalized finished products and categories that are weather-sensitive or face competition from home cooking.

Conversely, the analysis of per capita data validates the argument of a massive shift toward basic ingredients and cooking aids, which allow for lower-cost cooking. Pasta sauces have emerged as the big winner in the daily lives of the French, with individual consumption climbing from 1.8 kg in 2021 to an estimated 2.2 kg in 2025, driven by a highly dynamic annual growth rate of 5.29% (CAGR). Equally significant, tomato paste and purees grew at an average annual rate of 1.92% to reach 1.6 kg per capita in 2025. Even more impressively, canned tomato consumption recorded a jump of 4.63% per year, rising from 0.9 kg in 2021 to 1.0 kg as early as 2023, a level that holds steady through 2025. Ketchup, meanwhile, remained remarkably stable, fluctuating slightly around 0.9 kg per capita.

Analyzing the French tomato derivatives market through the lens of individual consumption confirms previous observations regarding consumer choices, shifting national volumes, and trade-offs between different distribution channels.

In the first place, the decline in volumes coupled with an increase in value is explained by a shift in product ranges: faced with inflation, households turned away from ready meals and pizzas in favor of cheaper, raw ingredients like pasta sauces or canned tomatoes. Although this individual retrenchment contracted volumes, the sharp rise in production costs—even for basic products—artificially inflated market value.

Furthermore, this shift toward “home cooking” accounts for the strong resilience of the retail channel (see complementary data at the end of the article). By increasing their consumption of cooking aids, French consumers offset restaurant closures and costs, turning retail grocery into a safe haven.

Finally, projections for 2026–2030 signal a trend reversal. The stabilization of individual consumption for processed products, which began as early as 2024, foreshadows a rebound in overall volumes. Barring an unexpected change in the French context, this momentum should now be driven by foodservice and the search for convenience, marking the transition from a domestic crisis economy to standardized consumption.

Sales Projections for 2026–2030 (Total Volumes)

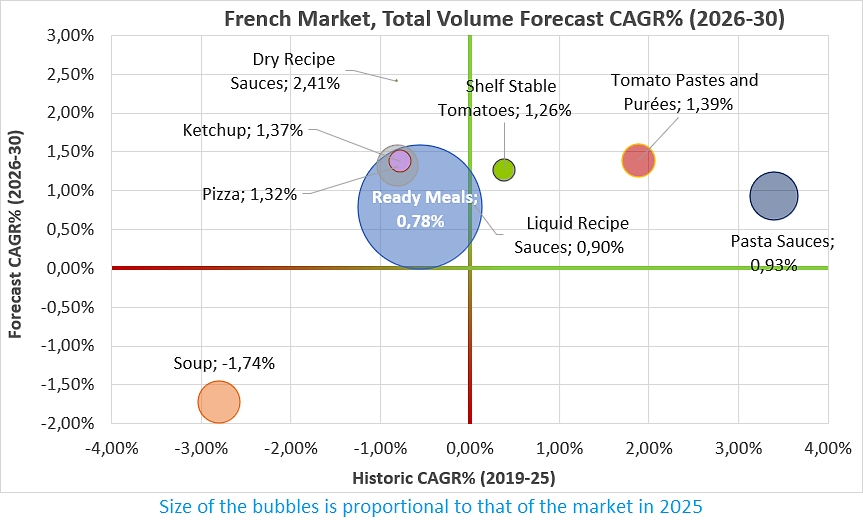

An analysis of the compound annual growth rates (CAGR) in the French tomato derivatives market, recorded from 2019 to 2025 and projected from 2026 to 2030, highlights a profound transformation in consumption habits, marking a true trend reversal on a national scale. While the historical period (2019–2025) ended with a slight annual market decline of around -0.12% (CAGR), projections for the 2026–2030 period point to a clear recovery, with overall growth estimated at +0.69% (CAGR) per year. This turnaround is expected to rely on a return to positive dynamics for the majority of categories that were losing steam up until 2025. The most glaring case—albeit on extremely modest volumes—is that of dehydrated sauces, which post the sector’s most spectacular rebound by shifting from a decline of -0.81% to the market’s strongest growth at +2.41%. For significantly larger quantities, ketchup, pizzas, and ready meals are turning the tide to post solid growth, signaling a successful adaptation of supply to new consumer demands or a renewed interest in these meal solutions.

At the same time, raw ingredients and basic cooking aids confirm their status as pillars and safe havens, remaining part of a long-term home-cooking trend. Shelf stable tomatoes are expected to see a notable acceleration in growth, rising from +0.39% to +1.26%, while tomato paste and purees will maintain a very solid pace at +1.39%, despite a slight slowdown compared to the previous period. According to Euromonitor projections, liquid sauces (excluding pasta sauces) are set to break out of their historical stagnation at 0.00% to return to an estimated growth of +0.90% per year.

Conversely to this recovery dynamic, two notable exceptions are reshaping the landscape of the French market. Pasta sauces, the major growth driver of the past period with a spectacular increase of +3.40%, are expected to face a sharp slowdown, settling at +0.93%, which suggests a saturation effect or a household shift toward canned tomatoes used as a base to make their own “homemade sauces.” Finally, the soup segment remains the only one firmly stuck in decline; although its downturn will be less rapid after 2025 than before, shifting from -2.79% to -1.74% (CAGR), soups continue to suffer from a consumer shift away from industrial options in favor of fresher products.

Sales Projections for 2026–2030 (Foodservice vs. Retail)

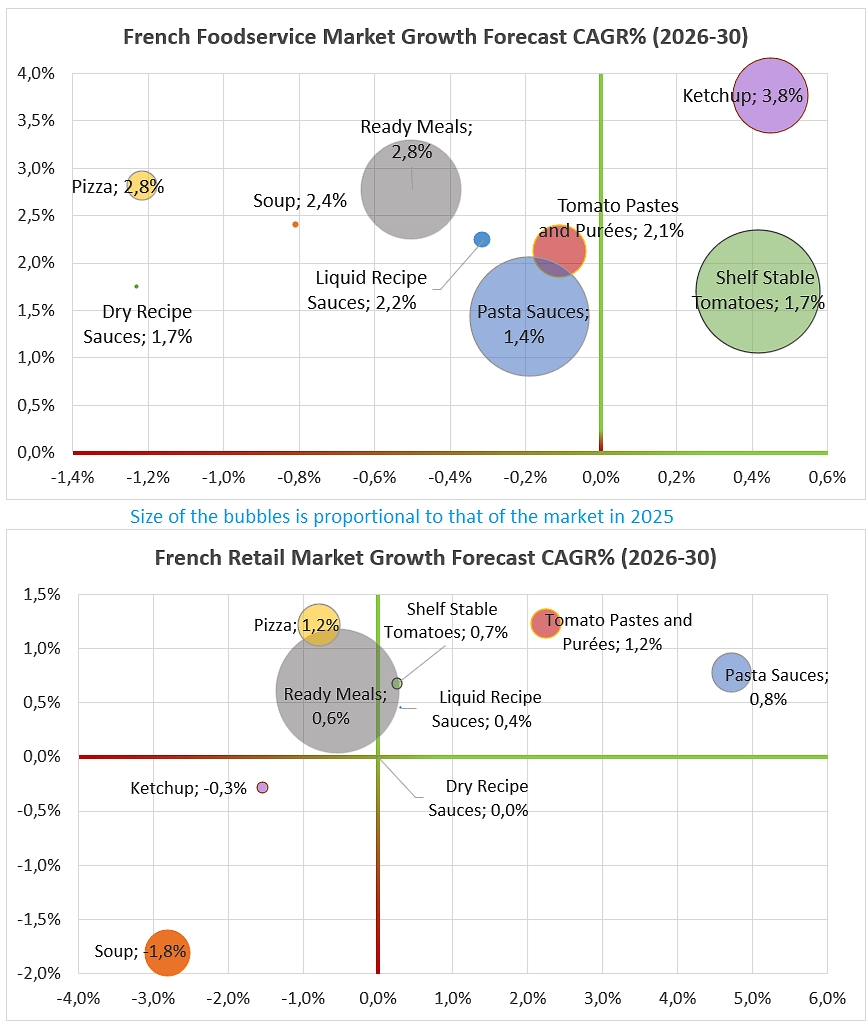

A comparative analysis of distribution channels reveals a true paradigm shift between the foodservice and retail channels in the French tomato-based products market. While the 2019–2025 period ended with an identical and uniform decline of -0.1% per year for both channels, projections for the 2026–2030 period highlight a massive decoupling in favor of out-of-home dining. The latter is poised to experience a spectacular boom, with an average annual growth estimated by Euromonitor at +2.3%, while retail stagnates in a very modest recovery at +0.4%. This striking contrast shows a transfer of value and volumes toward out-of-home consumption, driven by the momentum of fast food, delivery services, and pizza chains.

This surge in the Foodservice channel is visible across nearly all product categories, which are all shifting from a recessionary dynamic to skyrocketing growth: ketchup leads the way with an unprecedented historical acceleration forecast at +3.8% per year, followed closely by ready meals and pizzas, which each jump to +2.8% annual growth. Even basic ingredients such as soups, tomato purees, or liquid sauces, which were previously declining or stagnating in foodservice, are posting vigorous rebounds between +1.7% and +2.4%. This widespread performance indicates that foodservice professionals are heavily increasing their procurement to meet a rapidly expanding demand for out-of-home dining.

On the retail sales side, the landscape is much bleaker and points to a loss of momentum for at-home consumption. Retail’s major historical drivers are collapsing: pasta sauces, which boasted an exceptional momentum of +4.7% (CAGR) over the past period, are seeing their growth crumble to just +0.8%, while tomato paste and purees are slowing down by half to settle at +1.2%. Worse still, at-home consumption of ketchup and soups remains mired in negative growth, settling at -0.3% and -1.8% respectively. The only segments making slight gains on supermarket shelves are pizzas, canned tomatoes (peeled, diced, etc.), and ready meals, but their growth rates—ranging between +0.6% and +1.2%—remain very far behind the performances recorded for these same segments in foodservice.

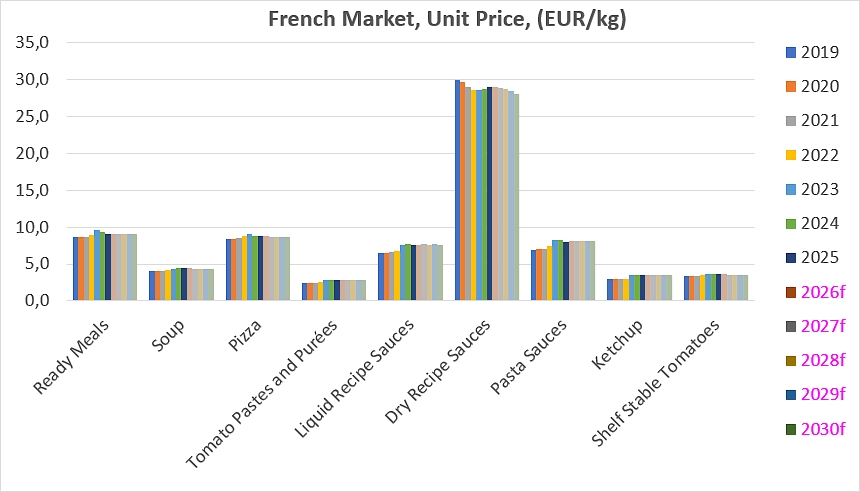

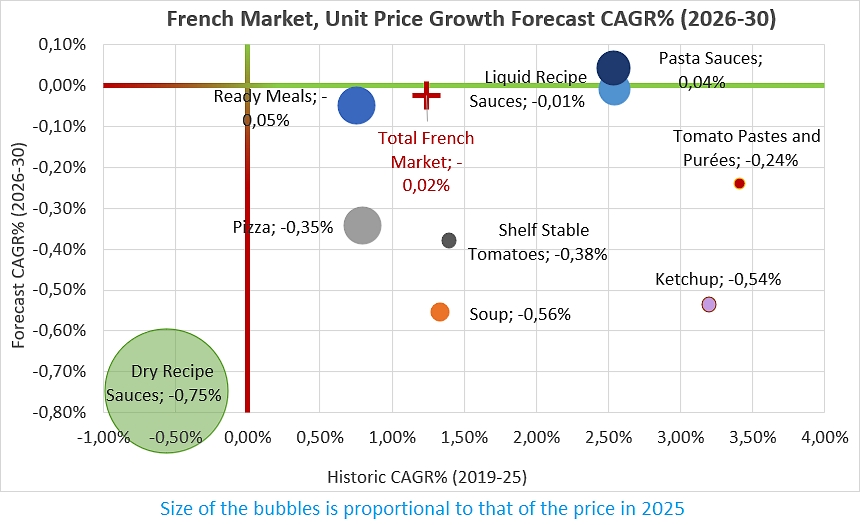

French Market: Unit Pricing and Valuation

The evolution of unit prices per kilo (EUR/kg) in the French retail market for tomato derivative products highlights a total break in momentum between past trends and future projections, marked by a sharp halt to inflation across all segments. Indeed, the historical period (2019–2025) was characterized by a near-universal rise in value, with most categories hitting a pricing peak around 2023–2024. Conversely, the 2026–2030 horizon is shaping up to be a phase of creeping deflation and absolute stagnation, where price structures are freezing or subtly eroding—signaling a long-term stabilization of production costs or increased competitive pressure on the shelves.

Looking closely at the categories, the trend reversal is particularly blatant for the basic products and cooking aids that had previously risen sharply: tomato paste and purees, which held the record for historical increases at an annual rate of +3.42% (rising from €2.4/kg to a plateau of €2.9/kg), are expected to see their growth stop completely and shift toward a slight decline of -0.24% per year by 2030. Ketchup is projected to hit a similar standstill: after a historic surge of +3.20% per year that brought the price per kilo to €3.6, its price is expected to edge down slowly to settle at €3.5 starting in 2027, representing a projected decline of -0.54% per year. Similarly, liquid sauces and canned tomatoes are shifting from a phase of clear valuation gains toward a very slow erosion of their unit prices.

Meal solutions and ready meals are expected to follow exactly the same trajectory of forced stabilization: industrial pizzas and ready meals, whose prices per kilo had peaked at €9.1 and €9.6 respectively at the heart of the inflationary crisis in 2023, are beginning a downward trend to freeze at €8.7 and €9.0 over the entire forecast period, posting negative growth rates of -0.35% and -0.05%. The only notable exception to this deflationary trend involves pasta sauces: although their growth slows to nearly zero at +0.04% per year, they remain the only category capable of maintaining their price per kilo at its highest level, sitting at €8.1 from 2025 to 2030. Finally, dry (dehydrated) sauces confirm their atypical status as a very high value-added product, albeit one in structural decline, continuing a steady decrease begun as early as 2019 to settle at €28.1/kg by the end of the period.

In conclusion, the French tomato derivatives market confirms its resilience as it begins a major transition leading up to 2030. Following a period of nominal growth dictated by inflation and pricing crises, the sector is entering a phase of organic consolidation driven by a more homogeneous underlying demand. This shift marks the end of an era of sharp price increases, with products now hitting a pricing glass ceiling for the next five years.

In terms of consumer behavior, dietary habits are rebalancing. While the recent economic crisis pushed consumers to turn away from industrial ready meals in favor of raw, economical ingredients for home cooking, the market is now moving toward a compromise between convenience and authenticity.

However, the true paradigm shift lies in the realignment of distribution channels. Faced with a mature and saturated retail market, the foodservice sector is now emerging as the primary engine of growth. Reshaped by the boom in out-of-home dining and delivery services, the tomato market no longer relies on domestic cooking, but finds its salvation in restaurant kitchens.

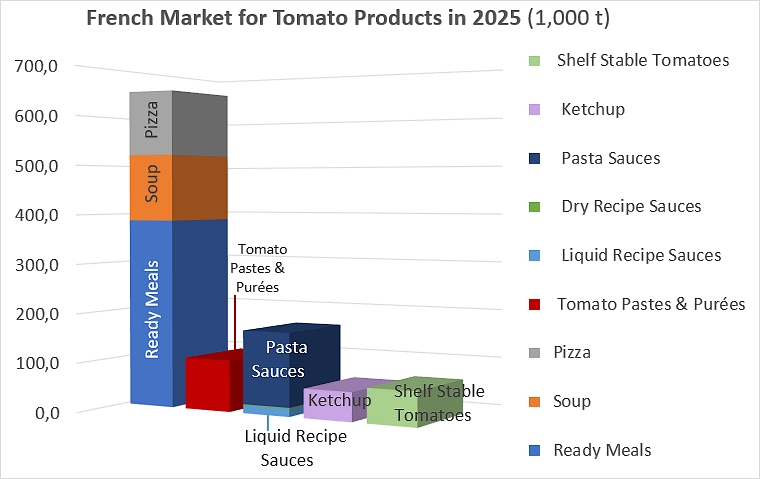

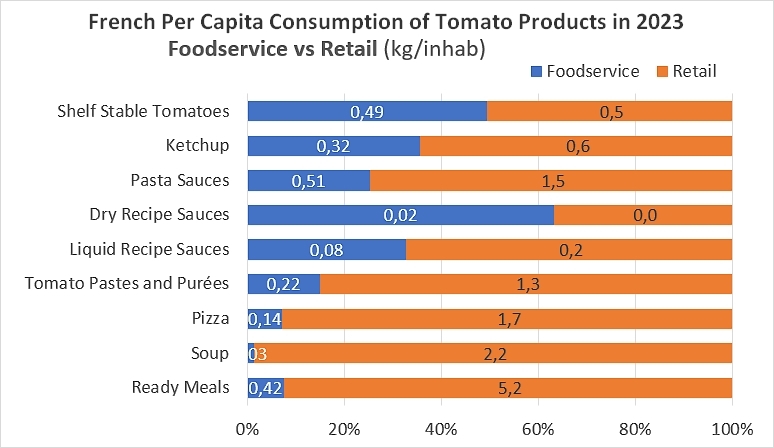

Some complementary data

Composition of the French tomato derivatives market in 2025 (1.06 million tonnes)

Breakdown of sales volumes for different products across foodservice (out-of-home dining) and retail channels.

Evolution of value across the different product sectors of the French market from 2019 to 2030.

For some complementary data on the product categories, click here.

Sources: Euromonitor, FAO Population

{kind=link}