News

Euromonitor: The European Market for Tomato Products – Part 2

European Market: Volume Dynamics vs. Value Dynamics

A direct comparison between sales volumes and market value over the 2025-2030 period reveals major shifts in dynamics, which highlight phenomena of inflation, premiumization, or, conversely, pressure on selling prices depending on the geographical area.

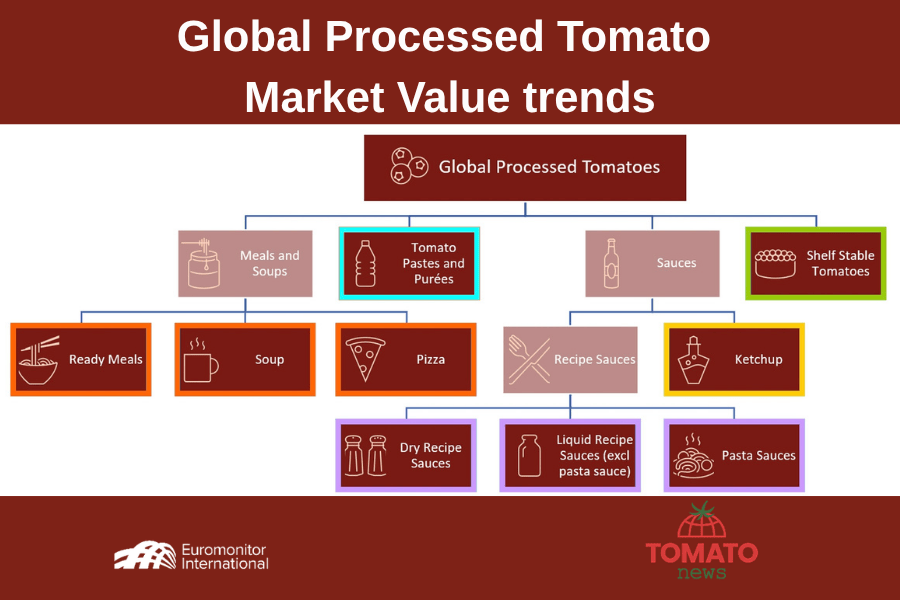

On a global scale, the processed tomato market follows a healthy trajectory where value and sales volumes progress hand in hand, although value shows signs of stabilization. Between 2026 and 2030, the value of global sales is expected to grow at a compound annual growth rate (CAGR) of 1.9%, rising from 170 billion euros in 2025 to 187 billion euros in 2030. This progression, slightly lower than the CAGR of volumes sold over the same period (2.1%), suggests a moderate decrease in average purchase prices per kilo at the global level, potentially driven by the development of economy formats or the rise of private labels internationally.

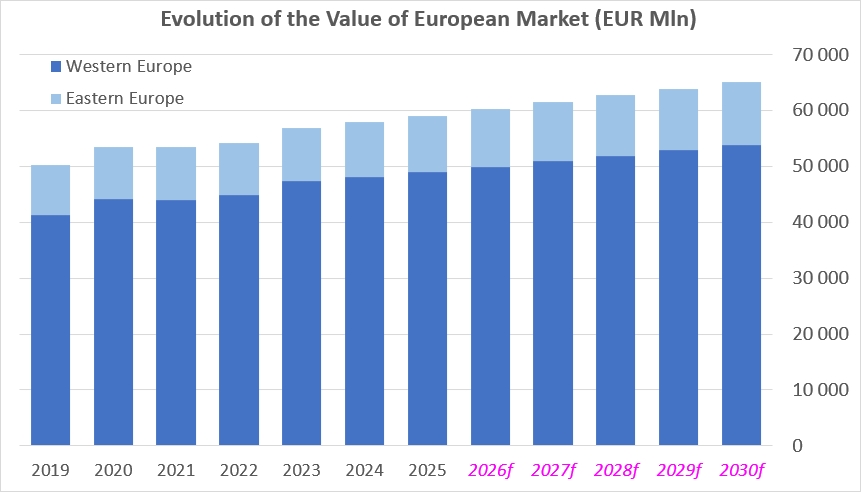

In Europe, the situation is reversed, pointing to a strong market valuation despite a less pronounced expected growth in volumes sold. The overall European market in value terms is projected to grow from 58.98 billion euros in 2025 to 65.01 billion euros in 2030. The striking fact lies in the growth rate: while European sales volumes progress at a forecast CAGR of 1.7%, the value of sales on the continent advances faster, at a pace of 1.9%. This positive differential shows that European consumers are spending more per tonne of processed tomatoes purchased, a finding that can be explained by the omnipresence in the shopping basket of high-value-added elaborate products (such as ready meals and sauces) at the expense of raw products (pastes, canned tomatoes).

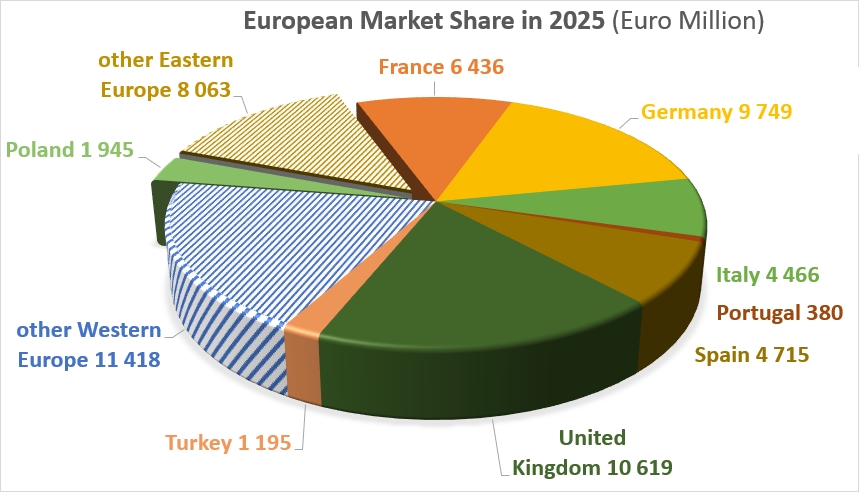

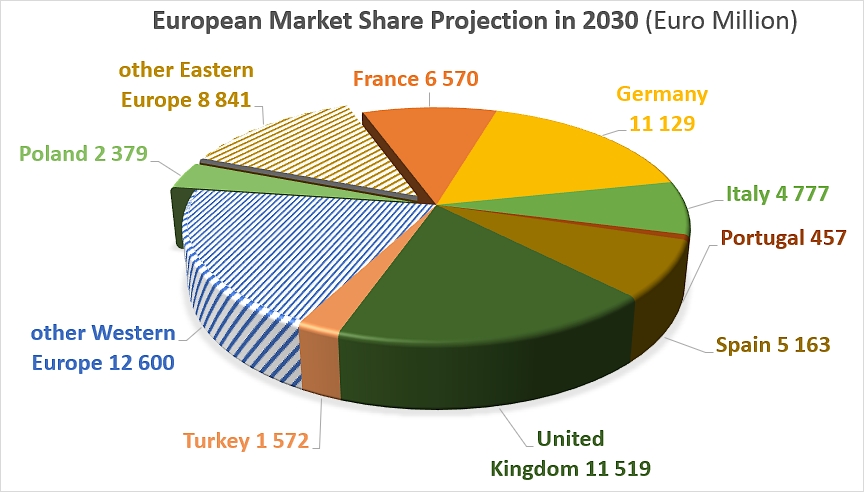

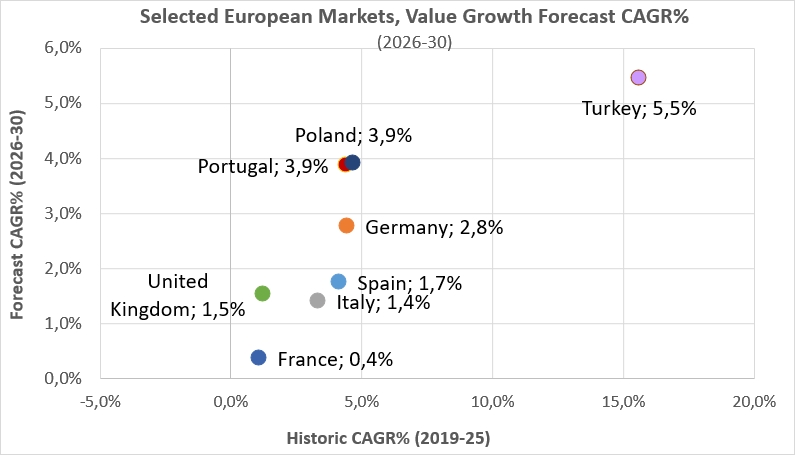

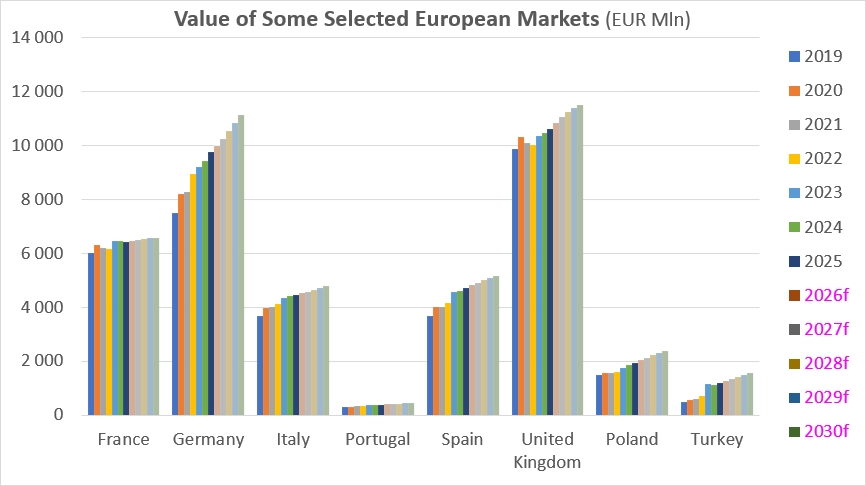

When looking at value, striking contrasts appear compared to sales volume figures, particularly for market leaders. The United Kingdom stands out as the undisputed champion of value creation in Europe: while it only accounts for 16% of volumes sold on the continent, the British market captures no less than 18.0% of the total European market value in 2025 (10.62 billion euros), and is expected to draw 17.7% in 2030 (11.52 billion euros). This financial outperformance is explained by the profile of British purchases, which are heavily geared toward branded ready meals and pizzas—sales segments with high valuations compared to the price of rawer tomato derivatives.

Conversely, Germany displays a profile of purchase rationalization. As the leader in volume with 18% of European sales, it accounts for only 16.5% of the market value in 2025 (9.75 billion euros). However, German sales show an aggressive catch-up dynamic, with a forecast value CAGR of 2.8% (compared to just 1.9% in volume). By 2030, Germany is expected to correct this gap by seizing 17.1% of the total expected value of the European market (65 billion euros), gaining ground on the United Kingdom thanks to an increase in the average shopping basket.

France confirms its premium positioning in buying habits. With only 9% of the volumes sold in Europe, it claims a significantly higher share of value, standing at 10.9% in 2025 (6.44 billion euros). In 2030, although its value share slips to 10.1% (6.57 billion euros) due to a low forecast CAGR of 0.4%, France maintains a very high value-to-volume ratio, indicative of a domestic market focused on quality products and high retail prices.

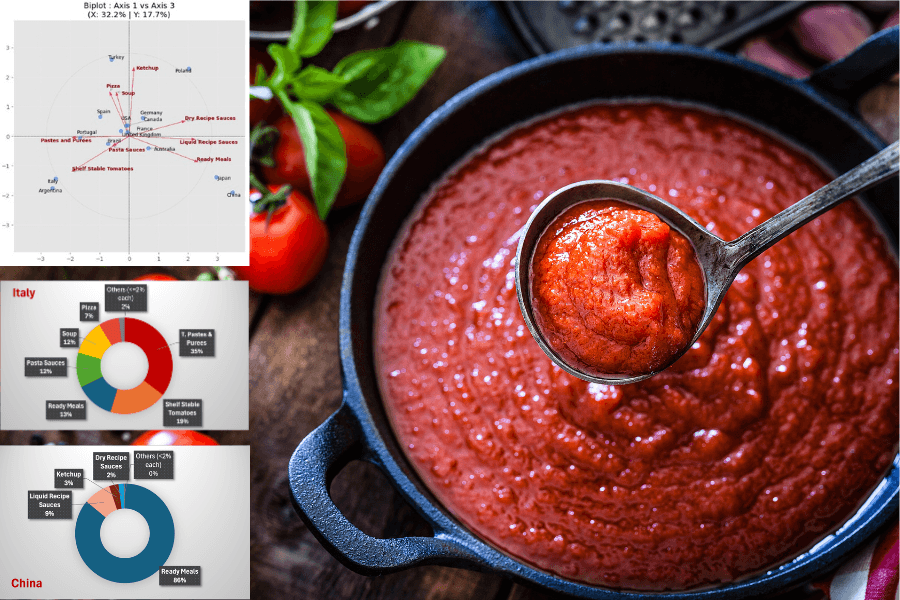

Italy and Spain technically suffer from their consumer profile leaning toward intermediate or less elaborate products. Italy accounts for 9% of the volumes sold in Europe but only 7.6% of the sales value in 2025 (4.47 billion euros), a share likely to drop to 7.3% in 2030 due to a CAGR of 1.4%. Spain follows a similar trend, with its value share slipping from 8.0% to 7.9%. For these two Southern nations, the predominance of tomato pastes, purées, and canned tomatoes in sales—commodity products with low financial valuation compared to ready-made industrial meals—weighs negatively on their overall financial weight.

Finally, Turkey illustrates a sharp economic landing dynamic after a phase of hyper-growth in sales. Over the historical period (2019-2025), the value market in Turkey literally exploded with an exceptional CAGR of 15.6%, propelled by inflation and a surge in consumer spending. For the 2026-2030 period, this value growth is set to slow down sharply to settle at 5.5% (1.57 billion euros in 2030). This figure remains higher than its expected sales volume growth (4.4%), positioning Turkey alongside Poland (3.9% value CAGR) as two Eastern markets that continue to boost the financial performance of the Eastern bloc.

Typological Profile of the European Tomato Derivatives Market

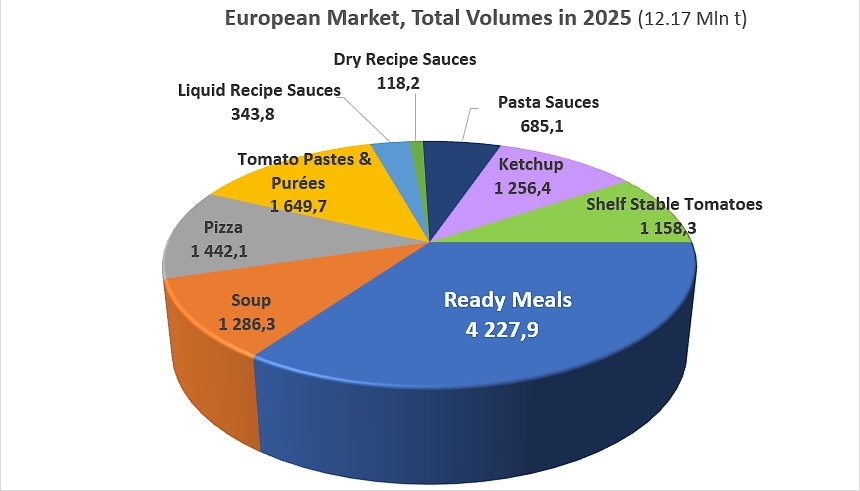

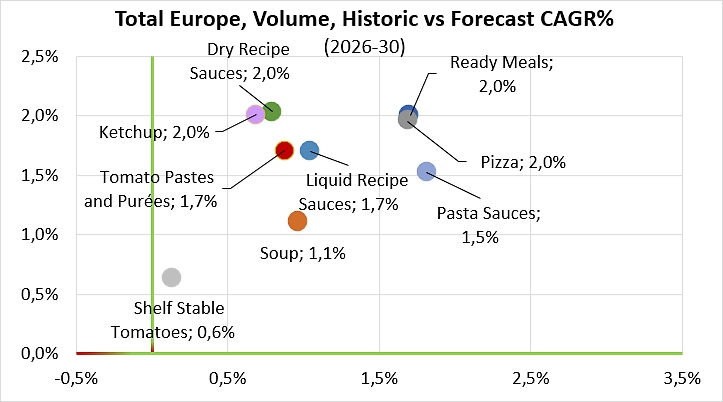

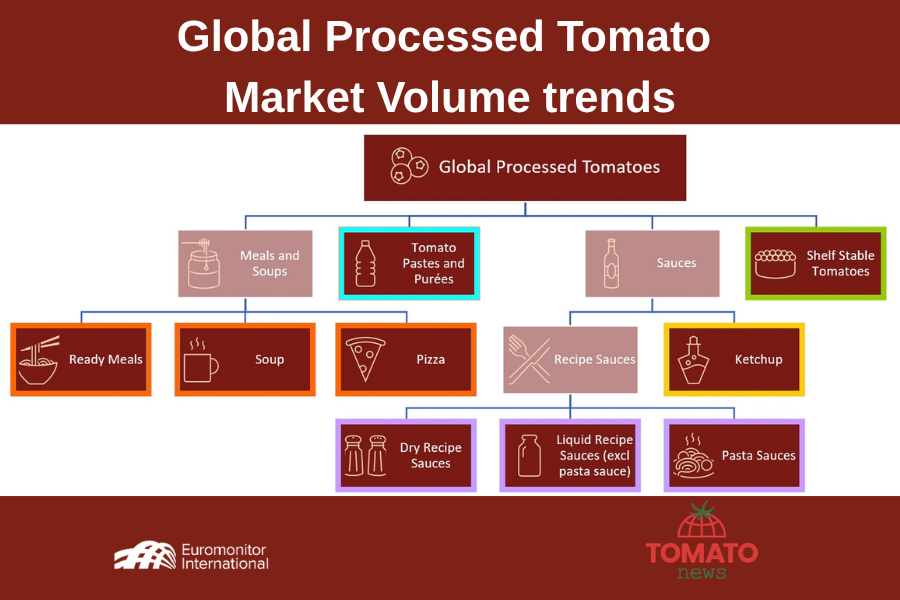

The European tomato products market (12.17 million tonnes in 2025) is organized in a highly asymmetrical manner, massively favoring products focused on convenience and time-saving.

As we have seen, the ready meals category crushes the market, capturing on its own 35% of total sales achieved on the continent (4.23 million tonnes). Far from being saturated, this heavyweight segment is expected to remain a robust growth driver through 2030, with a solid forecast CAGR of 2.0% that should bring the segment to around 4.68 million tonnes.

Ready meals are solidly backed by a group of major intermediate products, each hovering between 1.2 and 1.6 million tonnes in 2025. Within this bloc, tomato pastes and purées, pizzas, and ketchup are expected to display the strongest acceleration in sales by 2030, driven by future annual growth rates ranging between 1.7% and 2.0%. Soups, though significant in volume (1.29 million tonnes), are projected to follow a much more linear and timid trajectory (+1.1%).

At the other end of the spectrum, more traditional or less elaborate products are losing steam. Pasta sauces, for instance, are entering a phase of advanced maturity and will see their annual growth rate drop to 1.5% (compared to 1.8% historically). Finally, as we have seen, the decline is even more blatant for canned tomatoes: with future growth projected at just 0.6%, this segment is sinking into near-stagnation. This confirms a long-term trade-off by European consumers, who are abandoning raw “pantry staple” ingredients in favor of processed, ready-to-use solutions.

Growth Prospects by Segment: Western vs. Eastern Europe

A comparison of tomato products sales projections in Western and Eastern Europe reveals two highly distinct market profiles. It clearly contrasts a mature Western market—characterized by the normalization or slowdown of its historical segments—with an Eastern outlet in a full catch-up phase, experiencing a widespread acceleration in demand.

Eastern Europe behaves as a fast-accelerating catch-up market, driven by the rapid modernization of dietary habits. The pizza segment is particularly revealing, recording the sharpest acceleration on the continent with a forecast CAGR of 4.0%, rising from 72,000 tonnes in 2025 to 88,000 tonnes in 2030. Accompaniment and cooking sauces are also experiencing highly favorable dynamics, as seen with pasta sauces, where development prospects stand at 3.2% to bring the segment to around 57,000 tonnes, and ketchup, which maintains a steady pace of 2.2% to reach a sales volume of 541,000 tonnes in 2030. Meanwhile, historical and volume-heavy categories such as ready meals and tomato pastes are stabilizing at an identical forecast growth rate of 2.0% per year.

Western Europe, although qualified as a mature market due to seemingly lower growth rates, nevertheless remains the true giant of the continent in terms of absolute volume gains by 2030. The ready meals category demonstrates impressive strength: with a consistent forecast CAGR of 2.0%, it will generate on its own an additional volume of 337,000 tonnes, increasing from 3.20 million tonnes in 2025 to 3.54 million tonnes in 2030. Similarly, the pizza segment in the Western market is progressing by 1.8% to reach 1.50 million tonnes in 2030, generating a net gain of 131,000 tonnes that largely outperforms the gross increase observed in Eastern Europe.

The behavior of traditional categories in Western Europe confirms this “volume advantage”: tomato pastes and purées display a notable recovery with a forecast CAGR of 1.7%, which should raise sales levels to 1.55 million tonnes in 2030. Even pasta sauces in the Western market, whose annual growth slows slightly from 1.8% to 1.4%, manage to generate a gain of 48,000 tonnes—a volumetric performance higher than the entire pasta sauce market in the Eastern part of the European market. Finally, the only real point of stagnation again concerns canned tomatoes in Western Europe; although they weigh nearly one million tonnes, their growth prospects are expected to cap at a very low 0.5%, confirming a certain lack of interest among Western households for this raw product.

Europe’s Retail Prices by Country

The European market for tomato products is structured by a clear divide between low-processed industrial derivatives and high-value-added elaborate recipes. At the floor of this market, the canned tomato and tomato paste or purée segments establish themselves as basic necessities, whose retail unit prices generally hover within a low range between €1.2/kg and €3.5/kg. In these categories, volume logic prevails, and the geographical proximity of growing areas and processing sites in Italy, Spain, Portugal, Greece, and France dictates price structures, keeping prices at structurally low levels, particularly in Spain, thanks to large-scale integrated agricultural production. At the other end of the spectrum, the ceiling for dehydrated products is occupied by dry recipes sauces, which reach staggering heights ranging from €12/kg to nearly €50/kg. This extreme valuation is not explained by the scarcity of the basic ingredient, but by the impact of the dehydration process, which removes water weight to concentrate financial value while meeting a premium marketing positioning focused on ready-to-cook products.

Between 2019 and 2025, this landscape was profoundly disrupted by an era of global inflationary overheating. The surge in energy costs for cultivation, harvesting, and processing (concentration), combined with skyrocketing prices for metal or glass packaging and logistics transport, propelled unit prices upward across Europe, giving rise to spectacular national trajectories.

The most meteoric evolution is observed in Turkey within the tomato paste segment, where the retail unit price recorded a historical average annual growth rate of +13.2%; while the country stood out in 2019 on the European market with a very low price of €1.2/kg, the knock-on effect of local hyperinflation converted into euros pushed this price up to €2.5/kg in 2025. A similar dynamic occurred in the Turkish soup market, where the price jumped from €4.7/kg to €9.1/kg over the same period—an average annual rate of +11.8%—hoisting this product to a higher value level than those in France or Italy.

Conversely, the dry sauce segment in Italy revealed a unique glass ceiling effect: although the country started the period with the highest price in Europe at €49.8/kg in 2019, an average annual deceleration of -1.0% brought this rate down to €46.8/kg in 2025, suggesting that consumers were no longer willing to absorb further increases in this highly valued segment. At the same time, the United Kingdom distinguished itself through a strong revaluation of its condiments, with ketchup posting an average annual increase of +4.5% to move from €3.6/kg to €4.7/kg, contrasting sharply with the stagnation observed in Germany at €2.9/kg. This historical period also forced Western European countries, such as France and Spain, to increase the prices of shelf-stable tomato derivatives, pastes, and purées at a solid rate of around +3.4% per year in order to preserve industrial margins in the face of the input crisis.

In future articles, Tomato News will look back in greater detail at the ‘price/product’ profile of each country in this panel.

Projections for the 2026–2030 period outline a radical economic shift characterized by a major restructuring and stabilization of price grids. Based on current knowledge at the time of writing, Euromonitor models anticipate an easing of pressure on raw materials and an increased sensitivity of European households toward purchasing power. This is leading to a global convergence of growth rates toward stability, or even creeping deflation in certain industrialized countries. In mature countries like France, Germany, and Italy, forecast average annual growth rates are losing steam, now hovering between -0.5% and +0.5%, which equates to stagnant nominal prices and falling real prices. France is thus expected to rigidly stabilize the retail price of its ready meals at €9.0/kg until 2030, maintaining its premium positioning inherited from a moderate increase of +0.8% per year during the previous period. Germany, for its part, illustrates a trend toward industrial optimization and falling prices on premium goods, as the unit price of its dehydrated sauces, after peaking at €20.3/kg in 2025, is expected to decrease steadily at an average annual rate of -1.6% to settle at €19.0/kg in 2030.

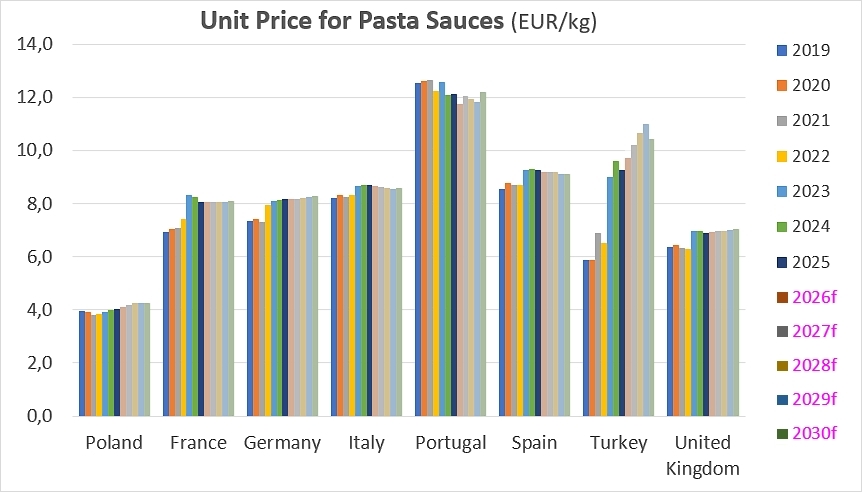

In the face of this “slow-motion dynamic” in Western Europe, Eastern Europe is establishing itself as the primary residual driver of value creation, fueled by the premiumization of the local offering and the continuous catch-up of purchasing power. Poland is the most striking example: the price of its tomato paste is expected to continue its upward trajectory at a projected average annual rate of +2.5%, climbing to €5.2/kg in 2030 to become one of the most expensive products in its category within the panel, far ahead of France’s €2.9/kg or Portugal’s €1.4/kg. The Polish market could also post a notable increase in ketchup, with an average annual progression of +1.7% until 2030. Meanwhile, Portugal will stand out due to an atypical behavior in the pasta sauce segment; after seeing its unit price drop from €12.5/kg to €12.1/kg between 2019 and 2025, the country is expected to enter a technical rebound of +1.0% per year to reach €12.2/kg in 2030, consolidating its rank as the most expensive market in Europe compared to an Italy “frozen” since 2025 at €8.6/kg. Finally, Turkey is expected to record a drastic normalization of its financial flows, with its forecast average annual growth rates calming down to settle within a reasonable range between +0.5% and +2.3% depending on the category, far from the overheating of past years.

Unit Price Outlook: Western Europe vs. Eastern Europe

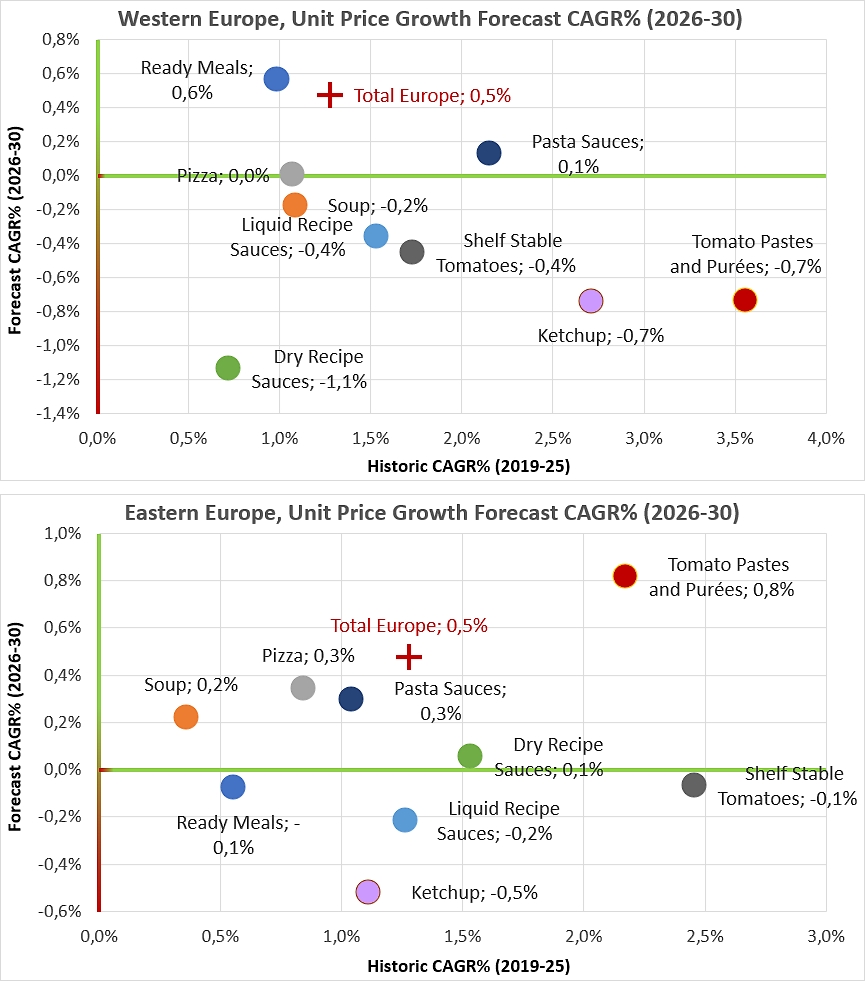

In terms of unit prices by product category, the European market for industrial tomato derivatives confirms the blatant asymmetry already identified across numerous aspects between its Western and Eastern components. While both regions suffered the consequences of the inflationary crisis over the historical period (2019–2025), their price trajectories and forecast growth dynamics (2026–2030) reveal two distinct economic models: a mature Western market looking for its landing point, and an Eastern market in a phase of structural catch-up and premiumization.

An examination of the historical period between 2019 and 2025 shows that Western Europe, against a backdrop of rising prices for raw materials and various agricultural and industrial inputs, drove the momentum of price increases on raw and commodity products. The most prominent example is found in the tomato pastes and purées category: Western Europe recorded a spectacular average annual increase of +3.6%, pushing the price from €1.6/kg up to €2.0/kg. Conversely, Eastern Europe approached this basic segment with a more moderate growth of +2.2% (moving from €2.9/kg to €3.2/kg). This dynamic reverses for high-value-added products like dehydrated sauces: in this segment, Eastern European markets saw unit prices climb at an average annual rate of +1.5% to reach €17.0/kg in 2025, while Western markets recorded only a timid increase of +0.7% (peaking at €15.7/kg). Condiments like ketchup and pasta sauces confirm this Western trend of passing industrial costs onto table value, posting respective annual growth rates of +2.7% and +2.2% in the West, compared to just +1.1% and +1.0% in the East.

Projections through 2030 map out a disruptive scenario and completely reverse the balance of power regarding growth. Euromonitor data seems to indicate that Western Europe is about to enter a phase of creeping deflation or rigid stagnation of unit prices for virtually all categories. The heaviest slowdown is expected to affect dry sauces in Western European markets, whose compound annual growth rate (CAGR) is projected to sink to -1.1%, bringing the price down from €15.7/kg to €15.0/kg in 2030—a sign of cost optimization or fierce price competition on premium tomato derivatives. Ketchup (-0.7%), pastes (-0.7%), and canned tomatoes (-0.4%) are expected to follow this same downward slope in the West. Only ready meals are projected to successfully maintain a slight value growth of +0.6% per year.

In contrast, Eastern Europe is establishing itself as the true driver of value growth through the end of the decade. Free from the price drops affecting Western European markets, the Eastern region is projected to post positive and steady growth rates by 2030. The paste and purée segment is expected to progress there at a solid annual pace of +0.8% (reaching €3.4/kg), while pizzas (+0.3%), pasta sauces (+0.3%), and soups (+0.2%) will continue to gain value. The valuation trajectory of ketchup in Eastern European markets deserves particular attention: although it displays a negative growth rate of -0.5% over the forecast period, the unit price will manage to stabilize at €2.2/kg, thereby perfectly matching Western Europe’s price level in 2030.

On a continental scale, the overall European market reflects this major macroeconomic easing. The average annual growth rate of unit prices, which stood at +1.3% per year during the inflationary crisis (2019–2025), is expected to lose steam to settle at a modest +0.5% per year between 2026 and 2030, bringing the indicative average value (all products combined) from €5.8/kg to €6.0/kg. This apparent stability actually conceals a geographical shift: Western Europe compensates for its maturity and falling prices by stabilizing volumes, while Eastern Europe absorbs the remaining value by consolidating its price positions and gradually aligning its pricing standards with those of its Western neighbors.

In conclusion, Euromonitor figures show that the European processed tomato market is now structured around a two-tier dynamic, revealing a major structural, cultural, and geographical divide.

On a geographical level, Western Europe has entered an advanced maturity phase where growth is normalizing. Conversely, Eastern Europe and emerging countries like Turkey are establishing themselves as powerful growth engines. While the hierarchy of market shares remains frozen through 2030 in favor of Germany or the United Kingdom, actual volume momentum is driven by the Eastern axis (Turkey, Poland), whose expansion offsets the slowdown of markets like France.

This duality is accompanied by a cultural divide in consumption patterns. The Nordic and Anglo-Saxon bloc drives financial valuation by purchasing complex, expensive processed products focused on convenience and ready-to-eat solutions. In contrast, the Mediterranean bloc consumes large volumes but generates less value, remaining highly attached to less elaborate shelf-stable products as ingredients for home cooking.

Generally speaking, the market is shifting toward added value and convenience. Elaborate products (ready meals, soups, sauces) capture the bulk of growth with a compound annual growth rate (CAGR) of 1.8%, while traditional canned tomatoes are stagnating. At home, consumption is moving away from basic products to focus on pizzas and ready meals.

Finally, the true growth driver is migrating from the home to out-of-home catering (foodservice). This phenomenon is blatant in Eastern Europe, where economic catch-up and urbanization are propelling this channel at an exceptional pace, boosting demand for basic ingredients (pastes) and condiments (ketchup).

By 2030, Western Europe should remain the undeniable economic pivot due to its critical size, generating the bulk of additional volumes, while Eastern Europe offers the best growth rates in a global market undergoing price maturity and convergence.

Some complementary data

Pasta Sauce

These pre-packaged/prepared sauces are either added directly to cooked pasta or heated up for a few minutes beforehand. Alternatively, they can be added to fresh ingredients (e.g. meat or vegetables), and then heated up to make a sauce which will then be added to cooked pasta. Pasta sauces include ambient or shelf-stable as well as chilled (in refrigerators) and frozen formats. Dehydrated pasta sauces which need addition of water or wine are excluded and tracked in dry sauces. Product typesinclude: Pesto, bolognese, carbonara, mushroom, vegetable, etc.

Canned Tomatoes

Ambient/shelf stable tomatoes typically sold in tins, glass jars, aluminium/retort packaging or brick liquid cartons such as Tetra Recart or Combisafe. This includes sun-dried tomatoes. Products with added seasoning (e.g. with chilli, garlic or herbs) are also included. Note that tomato pastes, passata and purées are all excluded and tracked within sauces, dressings and condiments.

Tomato pastes and Purées

Tomato paste, or tomato concentrate, consists of tomatoes that have been cooked for several hours, strained and reduced to a thick, rich concentrate. Tomato purée consists of tomatoes that have been cooked briefly and strained, resulting in a thick liquid. They typically only have 2-3 ingredients like water, tomatoes, salt or citric acid. They don’t contain any other spices/seasonings that are typical in pasta sauces.

Pizza

Pizza covers both, chilled and frozen pizza, typically in a ready-to-heat format. Any type of packaged, ready-made pizza sold in chiller/refrigerator and retail freezer cabinets are included. Pizza made on site is excluded.

Liquid Recipe Sauces (excl. pasta sauces)

Liquid cooking sauces and pastes are convenience products added before or during cooking, such as marinades or bases for stir-frys and stews. Categorized by specific cuisines or recipes, they include liquid gravies and dish-specific spice mixes, like liquid masala. While they serve as the liquidcounterpart to dry sauces, they exclude basic herbs and spices. Notably, this category includes liquid hot pot bases but excludes multipurpose “table sauces” like soy sauce, ketchup, or mayonnaise, which are tracked separately even if used during the cooking process.

Soup

Soups is the aggregation of dried (dehydrated formats), shelf stable and chilled and frozen soups. Includes: Ready-made, pre-packaged soup, regardless of format. Excludes: Liquid stocks and or stock/bouillon cubes. These are tracked in sauces, dressings and condiments, under cooking ingredients. Herbal soup mixes common in Asia are also excluded.

Ready Meals

This is the aggregation of shelf stable, dried, chilled and frozen ready meals. They have a high degree of readiness and convenience. In most instances they are ready-to-heat or ready-to-eat. Ready meals are generally accepted to be complete meals that require few or no extra ingredients. However, in thecase of shelf stable ready meals, the term also encompasses meal ‘centres’.

Dry Recipe Sauce

Dry sauces are recipe mixes in powdered formats ie products in this category are named as the dish itself. Requires the addition of boiling water or milk before consumption. Other powdered products not attached to a specific recipe should be excluded from dry sauces. Includes dry recipe powder mixes, dry recipe seasoning mixes (ie, fajita spice mix), hot pot sauce mixes in powder format, and dry powder marinades. It often goes by the name of the recipe/dish it makes. Liquid versions should be in cooking sauces. Other product types include: hollandaise sauce, white sauce, pepper sauce, sweet and sour sauce, spaghetti bolognaise, satay sauce, etc.

Western Europe

Andorra, Austria, Belgium, Cyprus, Denmark, Finland, France, Germany, Gibraltar, Greece, Iceland, Ireland, Italy, Liechtenstein, Luxembourg, Malta, Monaco, Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, Turkey, United Kingdom.

Eastern Europe

Albania, Belarus, Bosnia and Herzegovina, Bulgaria, Croatia, Czech Republic, Estonia, Georgia, Hungary, Kosovo, Latvia, Lithuania, Moldova, Montenegro, North Macedonia, Poland, Romania, Russia, Serbia, Slovakia, Slovenia, Ukraine.

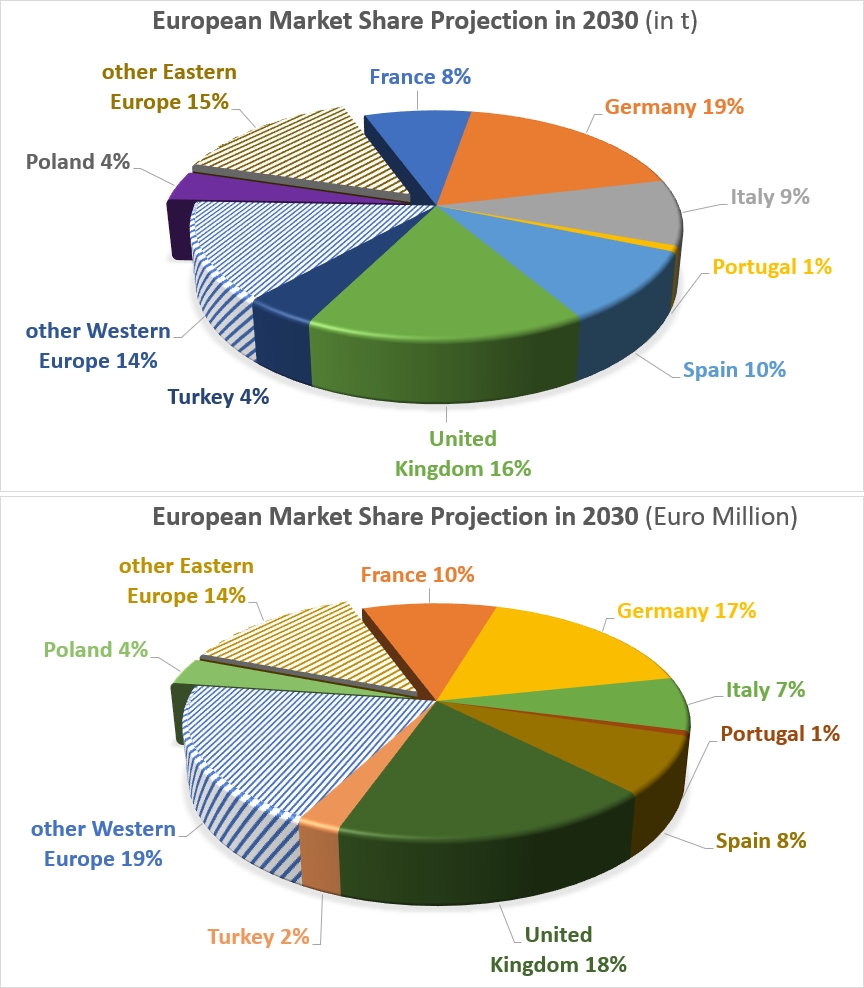

Outlook for the breakdown of tomato derivative sales in the European market in 2030, by volume and value.

Volume development outlook in Europe for each product category, between 2016 and 2030.

Total annual values in millions of Euros of selected European markets for tomato derivatives.

Note: Euromonitor’s forecasting methodology integrates quantitative econometric modeling with qualitative local expertise. At its core, the system utilizes regression-based frameworks to link historical sales data with key macroeconomic drivers—such as GDP, inflation, and disposable income—which are updated quarterly.

Beyond statistical modeling, the approach incorporates structural factors like demographics and urbanization, while analysts apply an “expert layer” to account for industry-specific trends, innovation, and channel shifts. This hybrid model also allows for scenario and shock modeling, ensuring that projections remain market-realistic and adaptable to potential economic disruptions.

Source: Euromonitor

{kind=link}