News

Euromonitor: The European Market for Tomato Products – Part 1

The European processed tomato market is going through a phase of profound mutation, likely to redefine the strategies of the sector’s stakeholders. Driven by evolving urban lifestyles, convenience requirements, and the expansion of the foodservice sector, consumer behavior is reshaping the continent’s value map. Far from being uniform, these dynamic highlights striking region-to-region product-profile contrasts.

The highly comprehensive view of the processed tomato market, developed using statistical data collected by Euromonitor, highlights stable global growth but contrasting regional, national, typological, and financial dynamics between the historical period from 2019 to 2025 and the future projections established for the 2026-2030 period.

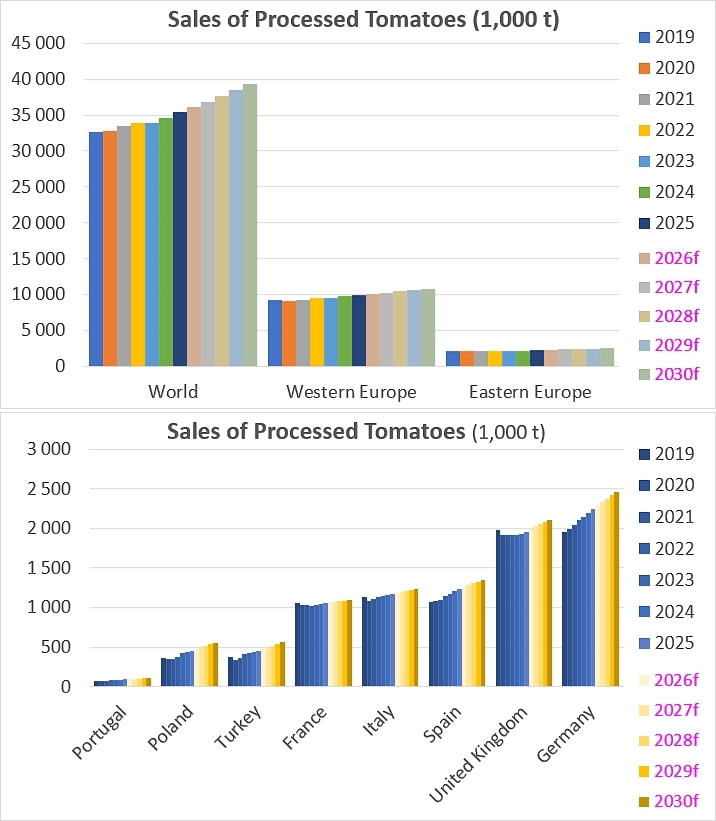

On a global scale, the processed tomato market is continuously expanding and showing a clear acceleration in its growth rate. Volumes are thus rising from 32.58 million tonnes in 2019 to a projected 39.28 million tonnes in 2030, while the compound annual growth rate (CAGR) is expected to accelerate significantly, from the historical period (1.4%) to the forecast period (2.1%) between 2026 and 2030.

The European continent behaves overall as a mature market that tends to lose international market share, simply due to faster growth recorded in emerging consumption regions: the “weight” of Europe as a whole (Western and Eastern Europe) on the global stage is undergoing a slow but clear erosion, dropping from nearly 35% in 2019 to 34.5% in 2025, and likely below 34% in the 2030 projections.

Meanwhile, within this bloc, internal dynamics are shifting. Western Europe is experiencing a relative decline: although it accounts for the bulk of sales on the continent with an average of nearly 10 million tonnes over the studied period, its share of the global market is continuously receding, falling from 28.3% in 2019 to a projected 27.4% in 2030, with an expected CAGR of 1.6% that remains notably below the global average (2.1%). Conversely, Eastern Europe is showing resilience; while its global market share remains flat at 6.4%, its growth rate could double to post a forecast CAGR of 2.1%, compared to just 1.1% over the historical period.

A detailed country-by-country analysis clearly distinguishes two groups: market giants on one side, such as Germany, the United Kingdom, Spain, Italy, and France, and smaller-scale markets on the other, represented by Turkey, Poland, and Portugal. Among the growth drivers boasting a high CAGR, Turkey stands out as the growth champion with the strongest acceleration: the CAGR of tomato derivative sales in Turkey is expected to rise from 3.4% to 4.4% for the 2026-2030 period, which would notably allow the country to overtake Poland once again in terms of volumes by 2030, with a outlook of 558,000 tonnes. Meanwhile, Portugal and Poland maintain high and stable growth rates, settling around 3.5% to 3.7%.

On the side of the mature giants, a widespread slowdown is visible. Germany and the United Kingdom remain the two largest European consuming countries in the panel, each exceeding 2 million tonnes; however, their growth tends to lose steam slightly, with Germany’s CAGR dropping from 2.3% to 1.9%, while the United Kingdom’s is expected to progress to around 1.5%. For its part, Spain is experiencing a sharp braking effect, as its forecast CAGR falls to 1.5% after a strong historical growth of 2.4%. Finally, the remaining countries are characterized by either a recovery or stagnation. After a historical period of decline around -0.1% between 2019 and 2025, the French market is expected to initiate a slight recovery with a forecast CAGR of 0.7%, which nevertheless remains the lowest among the featured countries. Italy follows a similar trajectory, with initially sluggish historical growth of 0.5%, but it is expected to double its pace to reach a CAGR of 1.0% by 2030.

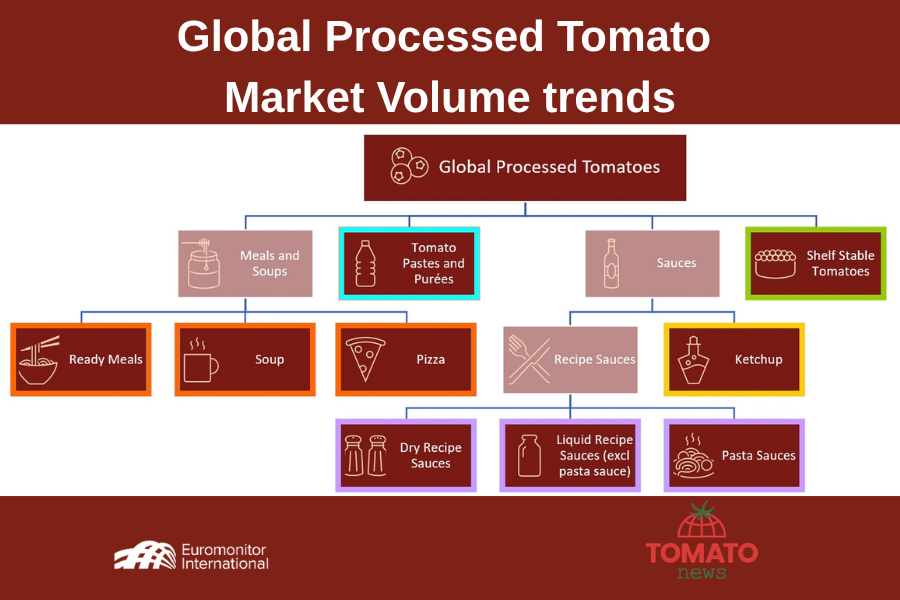

Europe Across Major Product Categories

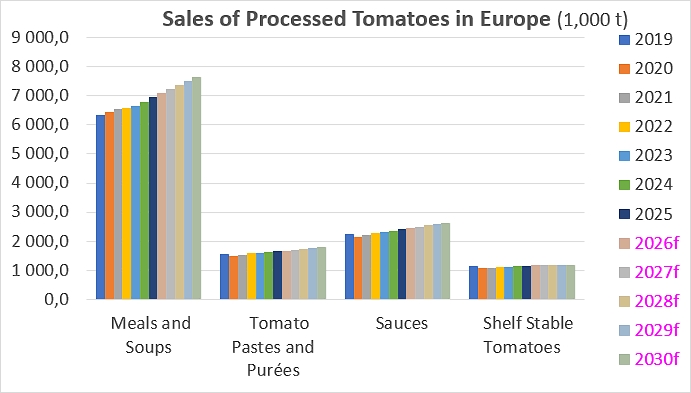

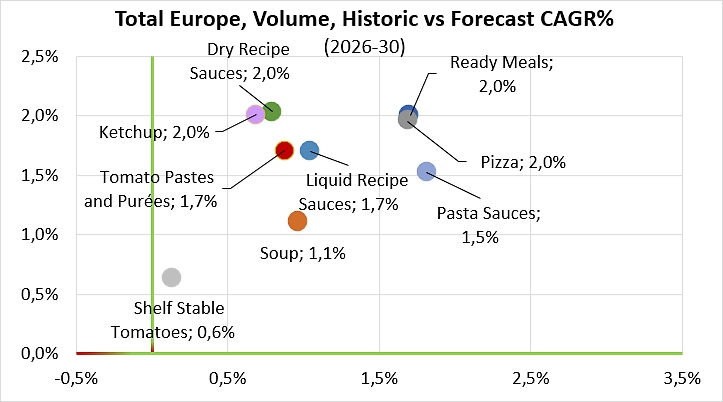

Euromonitor figures allow for an analysis of the distribution and evolution of the tomato derivatives market by product sub-categories, shifting the focus specifically onto the European continent. This reveals widespread growth across this geographical scale, but with distinct penetration dynamics between the historical period of 2019 to 2025 and future projections through 2030.

At the European scale, the Meals and Soups category exerts an overwhelming dominance over the entire sector, representing by far the largest market share by volume. Initially measured at 6.34 million tonnes in 2019, this European segment is projected to reach 7.64 million tonnes by 2030. This category shows no signs of slowing down; on the contrary, its momentum is accelerating slightly, as its compound annual growth rate (CAGR) rises from a historical level of 1.6% to a forecast 1.8% for the 2026-2030 period, thereby consolidating its position as the primary market driver on the continent.

In parallel, the sauce and paste categories are showing particularly marked accelerations within Europe. As the second-largest segment by volume, sauces demonstrate strong consistency, rising from 2.26 million tonnes in 2019 to a projected 2.64 million tonnes in 2030. The growth rate of these sauces is intensifying significantly, with their forecast CAGR climbing to 1.8% compared to 1.1% historically, allowing them to align with the progression speed of ready meals. As for Tomato Pastes and Purées, they recorded the weakest historical growth after canned tomatoes, with a meager 0.9% between 2019 and 2025, notably marked by a low point of 1.48 million tonnes in 2020. However, European projections for this segment are reversing dramatically with a near-doubling of the growth rate, materialized by a forecast CAGR of 1.7% aiming to reach 1.80 million tonnes in 2030.

In contrast to these positive dynamics, the Shelf Stable Tomatoes category appears in Europe as a mature and virtually stagnant market. Ranked as the smallest category by volume, it is also the one that—as previously mentioned in past Tomato News articles—is progressing the slowest, showing continental tonnages that are nearly flat, moving from 1.15 million tonnes in 2019 to a “modest” 1.20 million tonnes in 2030. After bordering on zero growth over the historical period with a rate of 0.1%, this segment is expected to see only a very timid uptick in the future with an estimated forecast CAGR of 0.6%. This could reflect a relative disinterest among European consumers for this raw product in favor of more elaborate solutions.

National Consumption Profiles in 2025

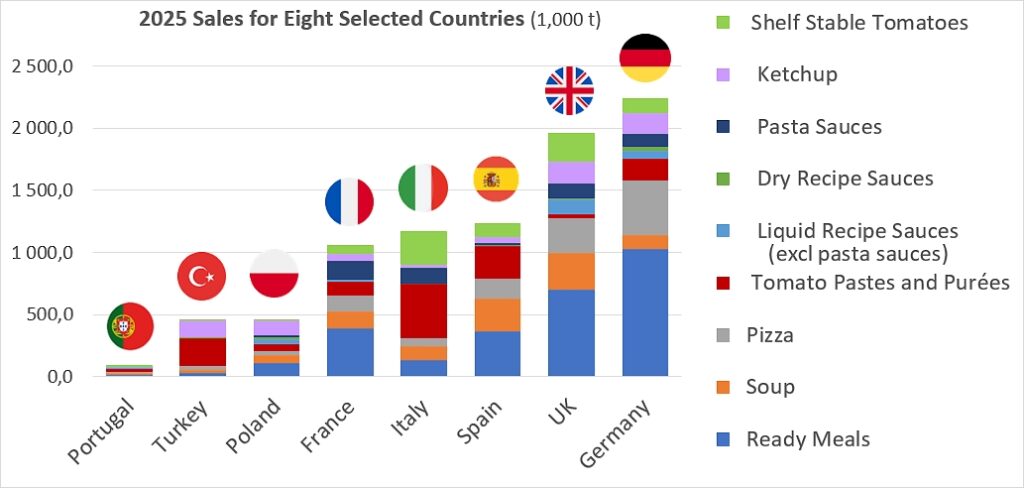

Providing an extremely precise X-ray of consumption habits and market structures, the detailed analysis of data within eight selected countries for the year 2025 reveals highly pronounced cultural and culinary profiles. It distinctly separates North and West European countries, which lean toward ready-to-use finished products, from Mediterranean basin countries, which remain attached to basic cooking ingredients.

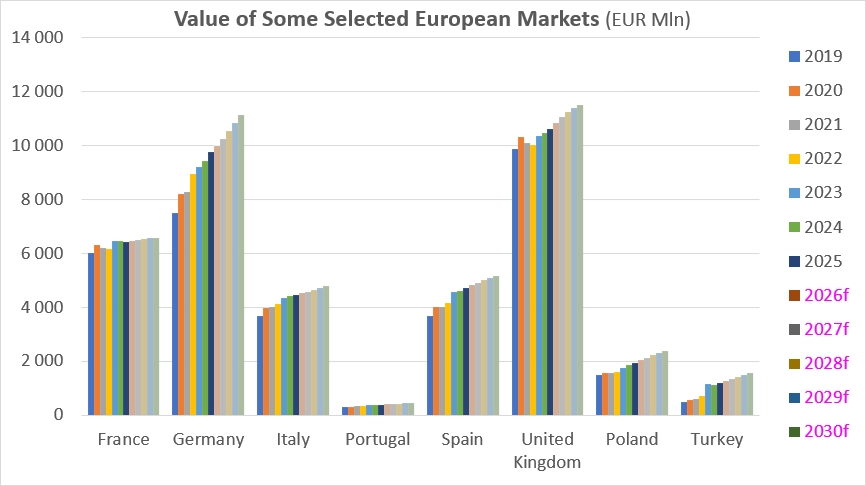

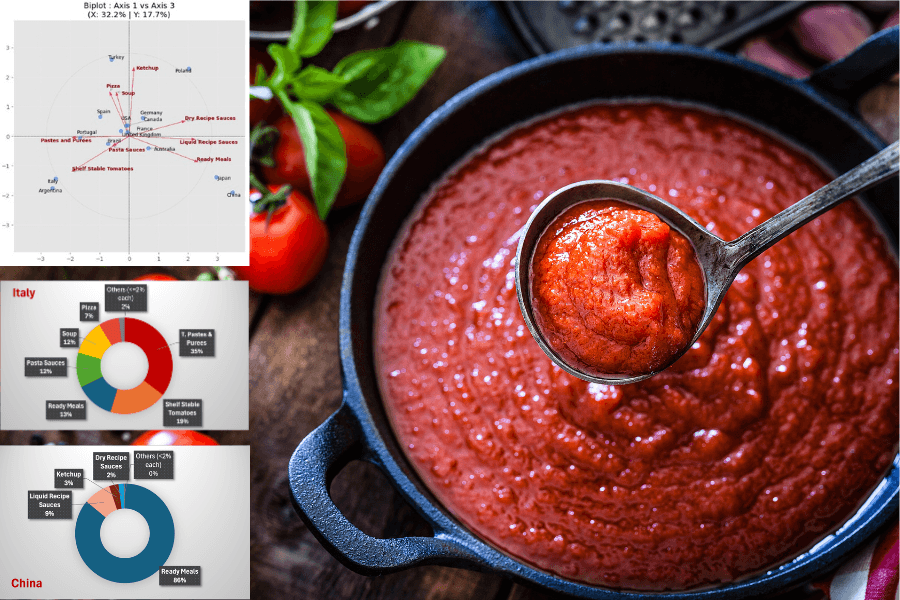

At the top of the volume pyramid, Germany and the United Kingdom clearly stand out as market leaders, displaying consumption structures geared toward convenience. In Germany, the leading market by volume with a total of 2.24 million tonnes, the Ready Meals category literally crushes the rest of the market on its own with 1.03 million tonnes, representing nearly half of the country’s total consumption. The United Kingdom follows a similar logic across its total market of 1.96 million tonnes, where ready meals account for 696,600 tonnes, complemented by a very strong presence of the Pizza category at 444,400 tonnes. For these two nations, the sum of ready meals, pizzas, and soups accounts for the vast majority of volumes, illustrating a clear preference for high-value-added, quick-to-prepare meal solutions.

Conversely, still in 2025, radically different cultural profiles emerge within the Italian, Spanish, and Turkish markets. In Italy, a country renowned for gastronomy and home cooking, the total market of 1.17 million tonnes is spectacularly dominated by raw or semi-processed ingredients: Tomato Pastes and Purées represent the largest segment with 433,400 tonnes, followed very closely by traditional canned tomatoes (peeled, crushed, or diced), which stand at 270,300 tonnes. Together, these two basic ingredient categories capture more than 60% of Italian consumption, while ready meals remain highly marginal at only 136,200 tonnes. Spain shares this identical market structure, with 259,900 tonnes of pastes and purées combined with a significant volume of pizzas and soups, confirming this attachment to intermediate culinary products. The case of Turkey is even more radical: out of a total volume of 451,200 tonnes, tomato paste alone accounts for 224,200 tonnes—exactly half of the national market—complemented mainly by ketchup at 134,500 tonnes, while categories such as pasta sauces or raw canned tomatoes are virtually non-existent there.

France occupies a pivotal and particularly balanced position, acting as a bridge between Northern and Southern European culinary cultures. Out of a total market of just over one million tonnes, no single segment asserts overall hegemony. Ready meals hold a significant place with 386,800 tonnes, quite far ahead of pasta sauces, which reach a remarkable 149,200 tonnes—the highest volume for this segment among the eight countries in the sample. French consumption is then distributed fairly evenly between soups (136,200 tonnes), pizzas (132,300 tonnes), and pastes (104,800 tonnes), reflecting a hybrid culinary practice that regularly alternates between assembling basic ingredients and purchasing fully prepared meals.

Finally, the smaller-scale markets of Poland and Portugal display notable peculiarities. Poland, despite being close to the Eastern European consumption profile, shows a strong appetite for ketchup with 112,800 tonnes, a volume higher than the ready meals category recorded in 2025 at 107,100 tonnes. Portugal brings up the rear with an overall market of 91,500 tonnes, distinguished by a proportionally very high consumption of tomato pastes and purées at 27,300 tonnes—a behavior that links it directly to the habits of its Mediterranean basin neighbors.

Foodservice vs. Retail: Western vs. Eastern Europe

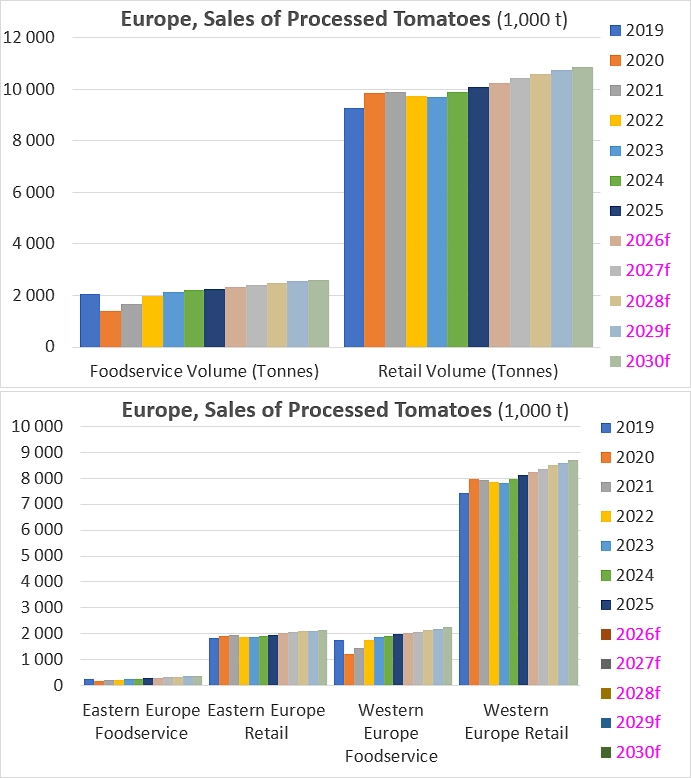

This Euromonitor dataset introduces an essential strategic perspective by breaking down European processed tomato consumption into two distinct distribution channels: Retail (sales for household consumption) and Foodservice (out-of-home catering). The analysis of these figures highlights a structural transformation in consumption habits, characterized by a powerful revival in foodservice, which is particularly dynamic in the Eastern part of the continent.

Across the entire European market, Retail distribution channels remain the undeniable historical pillar, capturing the vast majority of volumes. In 2019, retail sales already accounted for 9.27 million tonnes out of a total of 11.31 million tonnes, and projections for 2030 expect it to reach 10.86 million tonnes. However, this traditional outlet is locked into a linear and highly stable growth dynamic, showing a compound annual growth rate (CAGR) perfectly flat at 1.4% across both the historical period (2019-2025) and the forecast period (2026-2030). The true structural shift occurs on the Foodservice side: after suffering a brutal halt in 2020 with a historical drop to 1.41 million tonnes—a clear reflection of lockdowns linked to the health crisis—out-of-home catering rebounded vigorously to reach 2.25 million tonnes in 2025. Far from losing steam, this sector stands out as the primary market accelerator for the future, with a forecast CAGR expected to nearly double to 3.0% between 2026 and 2030, driving foodservice volumes to 2.62 million tonnes.

When considering the European continent by isolating its Western and Eastern geographical components, striking contrasts in maturity come to light. Western Europe behaves as a high-inertia reconsolidation market. Accounting for the bulk of European volume, Western European sales in the retail channel are progressing slowly, moving from 7.44 million tonnes in 2019 to a projected 8.72 million tonnes in 2030, with a pace that is losing steam very slightly, shifting from a historical CAGR of 1.5% to a forecast 1.4%. In return, Foodservice sales in Western Europe demonstrate solid vitality: after recovering from their 2020 low point of 1.21 million tonnes, their growth could accelerate to reach a forecast CAGR of 2.6% (compared to 1.8% historically), allowing this distribution channel to absorb 2.25 million tonnes of tomato derivatives by the end of the decade.

Yet, it is in Eastern Europe that the most spectacular phenomenon occurs, taking the form of a genuine boom in out-of-home catering. While retail channel sales in Eastern Europe follow a classic and moderate growth trajectory, rising from a CAGR of 1.3% to 1.6% to bring the sector to around 2.15 million tonnes in 2030, Eastern European Foodservice commercialization is undergoing a radical transformation: virtually marginal in 2019 with only 273,000 tonnes, and heavily shaken in 2020 at 196,000 tonnes, this outlet climbed to 280,000 tonnes in 2025. Projections for the 2026-2030 period anticipate an explosion in demand with a remarkable CAGR of 5.5%, representing the strongest growth dynamic across all sub-categories combined. This leap forward would allow Eastern European Foodservice to clear the 368,000-tonne threshold in 2030.

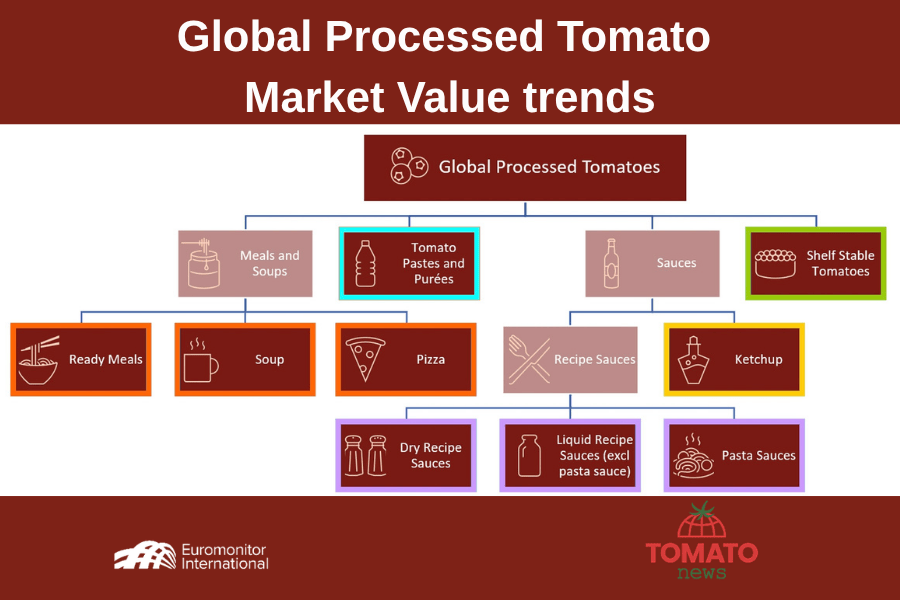

Contrasts Between Foodservice and Retail Across Different Segments

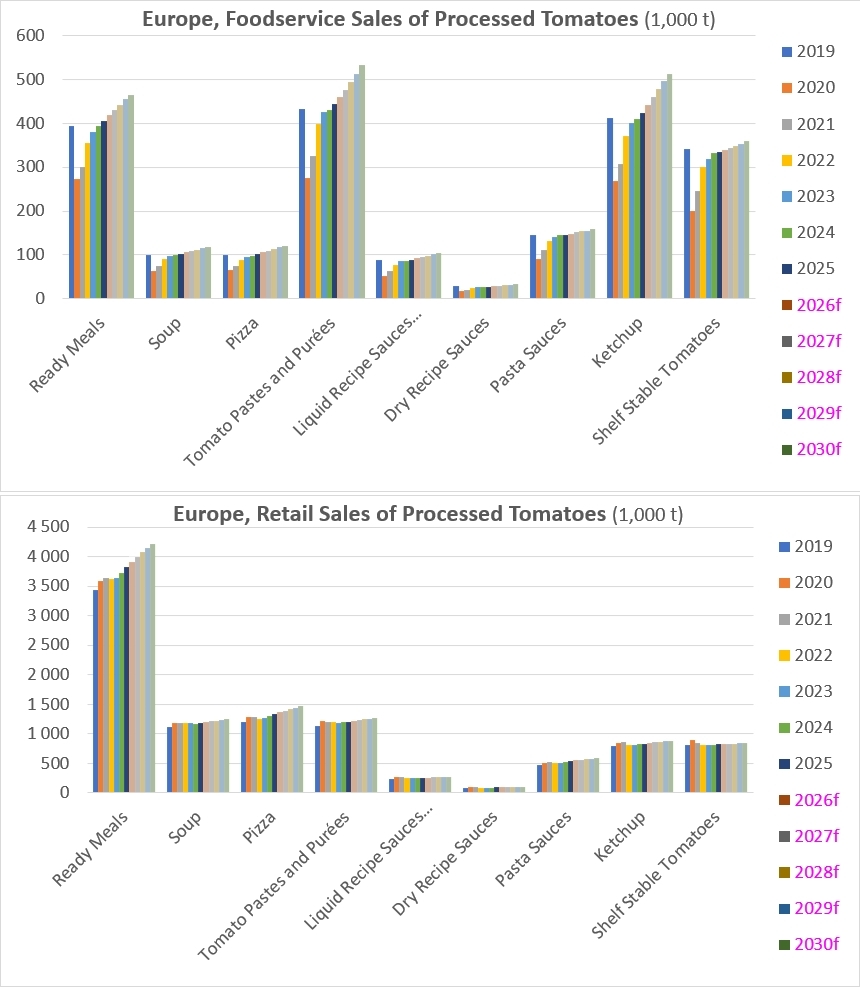

The cross-analysis of distribution channel data and finished product types confirms the marked acceleration of the out-of-home catering sector, which is establishing itself as the primary growth driver against retail channels that are globally more mature, despite their massive volumes.

At the out-of-home catering scale, the European market shows strong forecast momentum for the 2026-2030 period, having overcome a widespread historical trough in 2020 caused by health-related closures. Tomato pastes and purées commercialized in foodservice represent the leading segment by volume with 432,000 tonnes in 2019, reaching 443,000 tonnes in 2025 to culminate at 533,000 tonnes in 2030, driven by a solid forecast CAGR of 3.8%. However, the sharpest accelerations within this channel are found in convenience or festive products: pizzas sold in foodservice display one of the strongest expected increases with a 3.4% CAGR likely to bring the sector to 121,000 tonnes in 2030, preceded by foodservice sales of ketchup, whose projected growth (3.8% CAGR) should bring sales volumes (512,000 tonnes in 2030) into the immediate vicinity of pastes and purées. The projected progression of ready meals—the third-largest sector by sales volume with 405,000 tonnes in 2025—aligns just around the average of all sectors combined in out-of-home catering, with an annual growth outlook of 2.7% over the 2026-2030 period for an expected volume of 464,000 tonnes. Even historically declining segments, such as dry sauces and pasta sauces, which posted negative foodservice CAGRs of -0.3% and -0.1% between 2019 and 2025, are shifting into positive territory to reach future growth rates of 3.5% and 1.5% respectively.

On the retail side, the volumes at stake are significantly higher, and growth rates logically reflect an advanced level of maturity. Once again, the segment of ready meals consumed at home crushes the rest of the market by volume, rising from 3.42 million tonnes in 2019 to 3.82 million tonnes in 2025, with a forecast CAGR of 1.9% for a stable projection of 4.21 million tonnes by 2030. At-home pizzas also maintain a steady pace of 1.8% to reach 1.47 million tonnes in 2030. In contrast, retail sales of pasta sauces—which were the major historical driver with a growth of 2.4% between 2019 and 2025—could register a notable slowdown, with the forecast CAGR contracting to 1.5% for a final volume of 583,000 tonnes.

Other “traditional” products intended for households are either stagnating or showing sluggish growth. Retail prospects for growth in soups and tomato pastes are dropping back below the 1% mark, settling at 0.9% each, to reach 1.24 million and 1.26 million tonnes respectively in 2030. The observation is even harsher for retail sales of traditional canned tomatoes, whose growth remains frozen across both periods at a near-zero level of 0.3%, merely shifting from 807,000 tonnes in 2019 to 839,000 tonnes by 2030.

Foodservice vs. Retail: 2025 vs. 2030

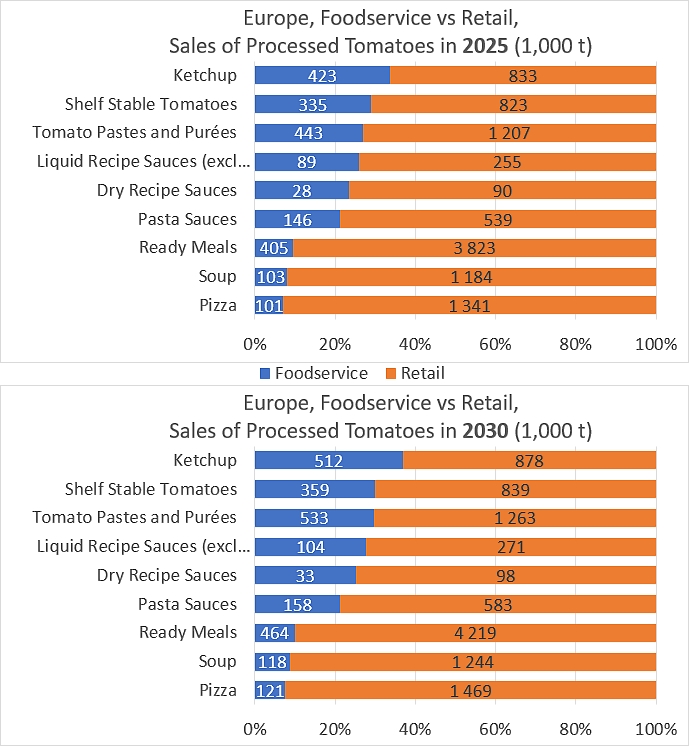

A comparison of distribution channel dynamics between 2025 and 2030 (projections) reveals overall stability in the breakdown of channels, but highlights two major trends.

First, total European volume is continuously progressing, rising from 12.17 million tonnes in 2025 to 13.26 million tonnes in 2030. This increase benefits both channels; the Retail sector remains ultra-dominant in absolute volume, climbing from 10.10 to 10.86 million tonnes, while the Foodservice sector asserts itself as the most active growth driver, moving from 2.07 to 2.40 million tonnes.

Second, the penetration structure by product remains almost unchanged over these five years, but it confirms highly distinct positionings. Ketchup remains the product most geared toward out-of-home catering, with more than 33% of its volumes sold in Foodservice in both 2025 and 2030. It is followed closely by canned tomatoes, pastes, and liquid sauces, whose sales all hover around a constant ratio of 25% to 30% in out-of-home catering. Conversely, volume-heavy categories such as ready meals, soups, and pizzas remain massively anchored in retail sales and at-home consumption, which systematically capture more than 90% of sales across both periods.

Geographical Breakdown of Sales in Europe

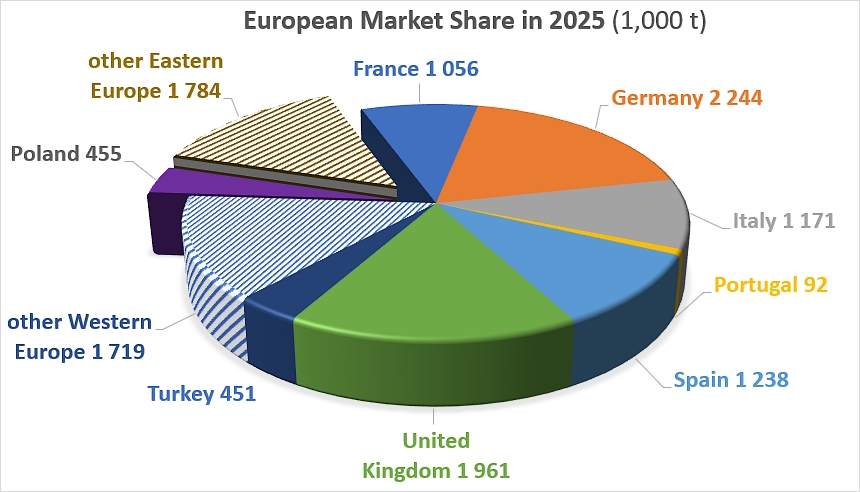

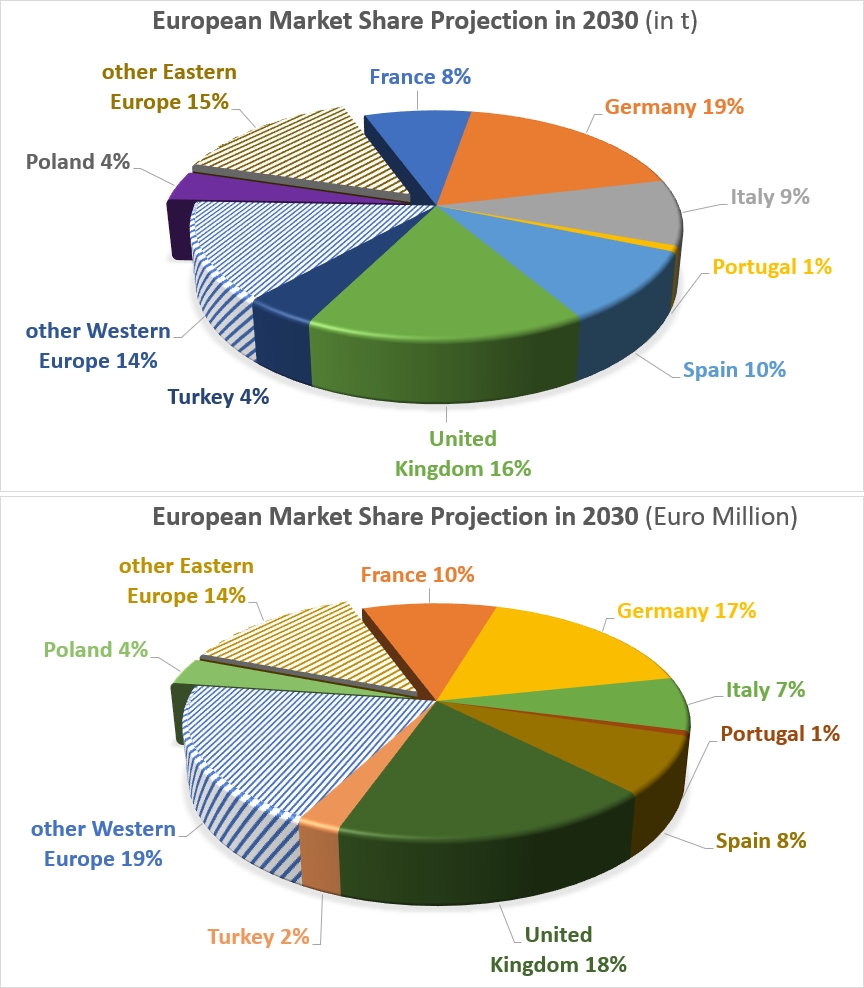

The comparative analysis of the European processed tomato market’s geographical components in 2025 and 2030 (projections) highlights a remarkable stability in overall market shares across the continent. This occurs against a backdrop of rising volumes and slight internal adjustments that confirm a gradual shift in momentum toward certain Eastern and Central European markets.

On a continental scale, the overall European market continues its expansion in terms of volumes, supported by an acceleration in its average annual growth, which is set at a rate of 1.7% for the future period compared to 1.2% historically. However, when translating this increase into relative national market shares, the structure of the European ecosystem remains largely frozen. The macro-regional breakdown undergoes no major modification: the combined share of other Western European countries not individually listed remains strictly at 14%, while that of the bloc of other Eastern European countries retains its constant position at 15% of the European pie across both periods (see additional data at the end of the article).

In terms of the national forces involved, the five historical pillars of the market continue to establish their dominance, capturing on their own nearly two-thirds of the continent’s consumption. Germany consolidates its position as the undisputed leader and proves to be the only Western giant to gain ground, with its market share rising from 18% in 2025 to 19% in 2030, driven by a volume growing from 2.24 million to 2.46 million tonnes. Conversely, the United Kingdom, the second-largest market, sees its share stagnate at 16% although its volumes climb from 1.96 million to 2.11 million tonnes. Spain and Italy also display perfect stability, maintaining their respective shares of 10% and 9% of the European market. France, however, stands out as the only major country in relative decline; its market share is eroding, falling from 8.7% in 2025 to 8.2% in 2030. Although French volume technically progresses from 1.06 million to 1.09 million tonnes thanks to the timid return of a future 0.7% growth, this pace remains too weak compared to the continental average, explaining its relative loss of momentum.

Finally, on the side of intermediate-sized markets, positions remain globally frozen but conceal asymmetric internal growth trajectories. Poland and Turkey each maintain an identical market share of 4% in both 2025 and 2030, just like Portugal, which remains anchored to its marginal share of 1%. Yet, the actual volumes of these countries are increasing significantly under the effect of highly sustained growth dynamics. Turkey notably benefits from the strongest acceleration in the panel, with a forecast growth rate of 4.4%, which should allow it to increase its volume from 451,000 tonnes to 558,000 tonnes. Poland follows a similar trend with growth projected at 3.7% to reach 550,000 tonnes in 2030. While these remarkable performances allow this duo to secure their positions and widen their lead over the rest of Eastern Europe, they still remain insufficient on a global scale to disrupt the hierarchy of the charts and alter European market share percentages.

Some complementary data

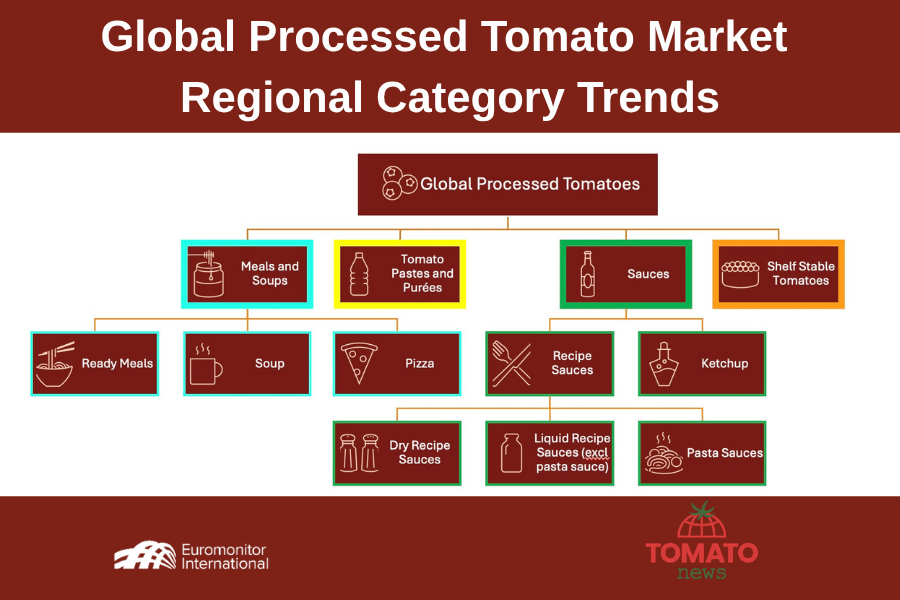

Euromonitor product definitions and list of countries per region

Pasta Sauce

These pre-packaged/prepared sauces are either added directly to cooked pasta or heated up for a few minutes beforehand. Alternatively, they can be added to fresh ingredients (e.g. meat or vegetables), and then heated up to make a sauce which will then be added to cooked pasta. Pasta sauces include ambient or shelf-stable as well as chilled (in refrigerators) and frozen formats. Dehydrated pasta sauces which need addition of water or wine are excluded and tracked in dry sauces. Product types include: Pesto, bolognese, carbonara, mushroom, vegetable, etc.

Canned Tomatoes

Ambient/shelf stable tomatoes typically sold in tins, glass jars, aluminium/retort packaging or brick liquid cartons such as Tetra Recart or Combisafe. This includes sun-dried tomatoes. Products with added seasoning (e.g. with chilli, garlic or herbs) are also included. Note that tomato pastes, passata and purées are all excluded and tracked within sauces, dressings and condiments.

Tomato pastes and Purées

Tomato paste, or tomato concentrate, consists of tomatoes that have been cooked for several hours, strained and reduced to a thick, rich concentrate. Tomato purée consists of tomatoes that have been cooked briefly and strained, resulting in a thick liquid. They typically only have 2-3 ingredients like water, tomatoes, salt or citric acid. They don’t contain any other spices/seasonings that are typical in pasta sauces.

Pizza

Pizza covers both, chilled and frozen pizza, typically in a ready-to-heat format. Any type of packaged, ready-made pizza sold in chiller/refrigerator and retail freezer cabinets are included. Pizza made on site is excluded.

Liquid Recipe Sauces (excl. pasta sauces)

Liquid cooking sauces and pastes are convenience products added before or during cooking, such as marinades or bases for stir-frys and stews. Categorized by specific cuisines or recipes, they include liquid gravies and dish-specific spice mixes, like liquid masala. While they serve as the liquidcounterpart to dry sauces, they exclude basic herbs and spices. Notably, this category includes liquid hot pot bases but excludes multipurpose “table sauces” like soy sauce, ketchup, or mayonnaise, which are tracked separately even if used during the cooking process.

Soup

Soups is the aggregation of dried (dehydrated formats), shelf stable and chilled and frozen soups. Includes: Ready-made, pre-packaged soup, regardless of format. Excludes: Liquid stocks and or stock/bouillon cubes. These are tracked in sauces, dressings and condiments, under cooking ingredients. Herbal soup mixes common in Asia are also excluded.

Ready Meals

This is the aggregation of shelf stable, dried, chilled and frozen ready meals. They have a high degree of readiness and convenience. In most instances they are ready-to-heat or ready-to-eat. Ready meals are generally accepted to be complete meals that require few or no extra ingredients. However, in thecase of shelf stable ready meals, the term also encompasses meal ‘centres’.

Dry Recipe Sauce

Dry sauces are recipe mixes in powdered formats ie products in this category are named as the dish itself. Requires the addition of boiling water or milk before consumption. Other powdered products not attached to a specific recipe should be excluded from dry sauces. Includes dry recipe powder mixes, dry recipe seasoning mixes (ie, fajita spice mix), hot pot sauce mixes in powder format, and dry powder marinades. It often goes by the name of the recipe/dish it makes. Liquid versions should be in cooking sauces. Other product types include: hollandaise sauce, white sauce, pepper sauce, sweet and sour sauce, spaghetti bolognaise, satay sauce, etc.

Western Europe

Andorra, Austria, Belgium, Cyprus, Denmark, Finland, France, Germany, Gibraltar, Greece, Iceland, Ireland, Italy, Liechtenstein, Luxembourg, Malta, Monaco, Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, Turkey, United Kingdon.

Eastern Europe

Albania, Belarus, Bosnia and Herzegovina, Bulgaria, Croatia, Czech Republic, Estonia, Georgia, Hungary, Kosovo, Latvia, Lithuania, Moldova, Montenegro, North Macedonia, Poland, Romania, Russia, Serbia, Slovakia, Slovenia, Ukraine

Note: Euromonitor’s forecasting methodology integrates quantitative econometric modeling with qualitative local expertise. At its core, the system utilizes regression-based frameworks to link historical sales data with key macroeconomic drivers—such as GDP, inflation, and disposable income—which are updated quarterly.

Beyond statistical modeling, the approach incorporates structural factors like demographics and urbanization, while analysts apply an “expert layer” to account for industry-specific trends, innovation, and channel shifts. This hybrid model also allows for scenario and shock modeling, ensuring that projections remain market-realistic and adaptable to potential economic disruptions.

Source: Euromonitor

Part 2 will be published soon

{kind=link}