News

US Inventories as of March 1, 2026 (comment)

The high inventory levels in June 2025, in spite of the increase in apparent consumption, are expected to result in a slightly excess inventory position at the end of the 2025-2026 marketing year.

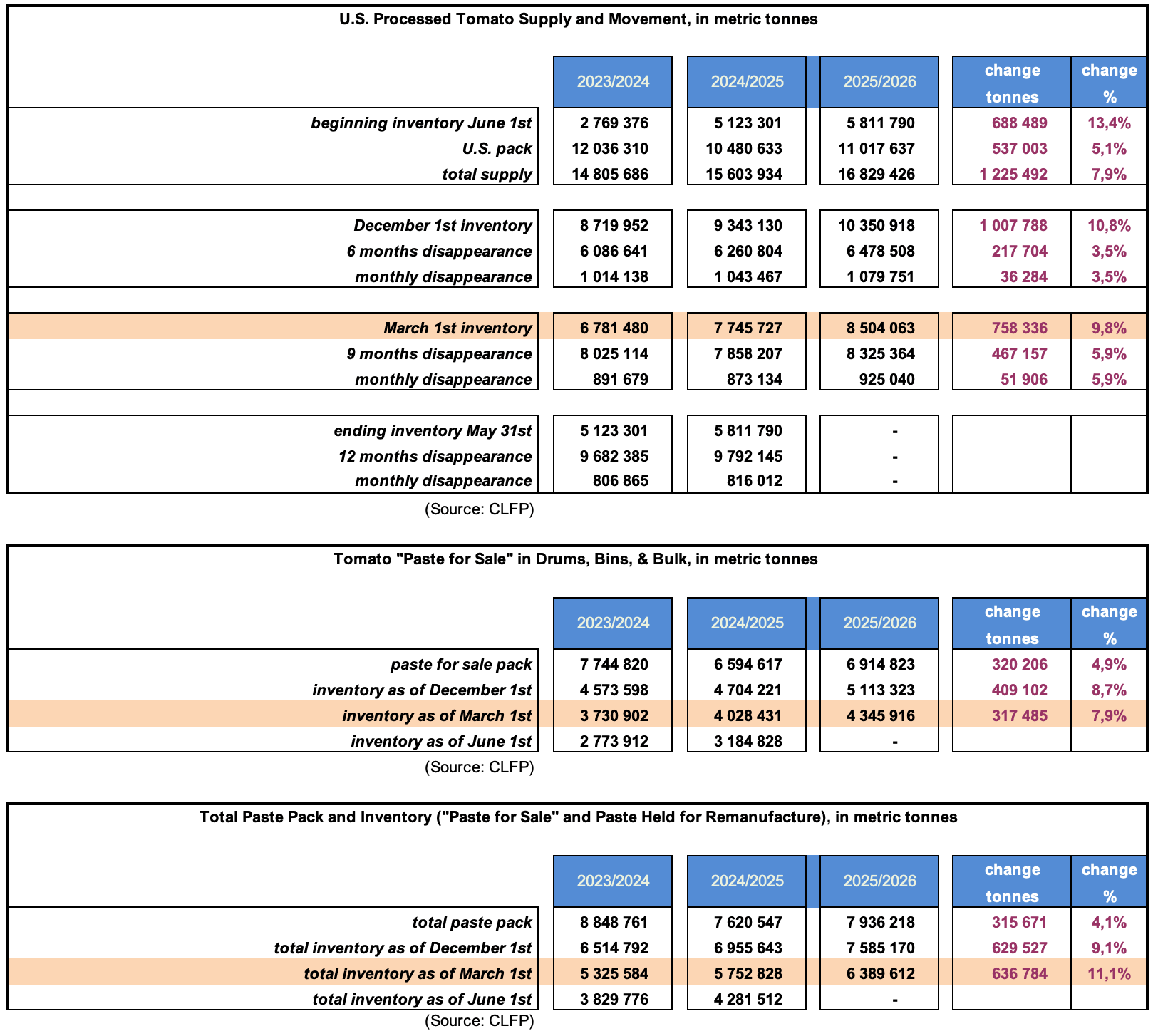

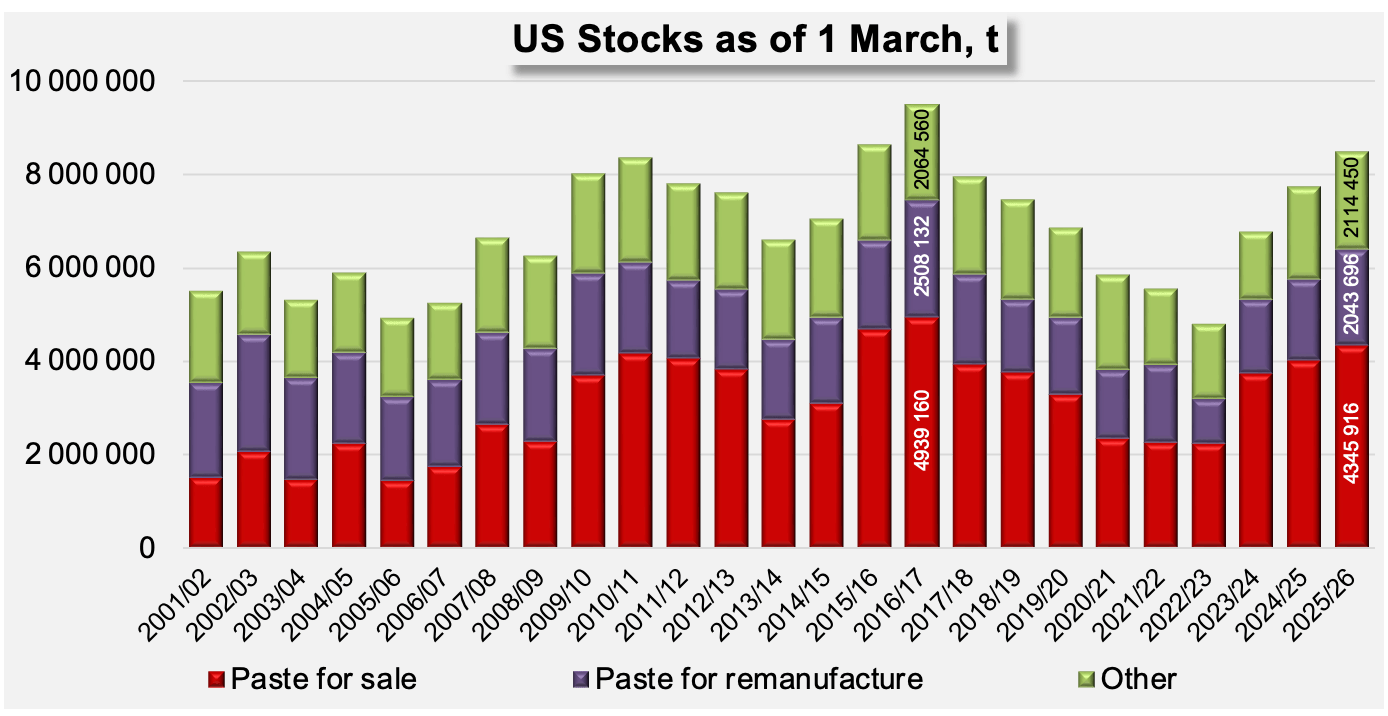

According to figures published by the California League of Food Producers (CLFP) on March 19, total US stocks of tomato products (expressed in fresh tomato equivalent) stood at approximately 8.5 million metric tons (t) as of March 1, 2026. As a consequence of the unexpected increase in processing activity (+5.1%) during the last season, the high level of stocks as of June 1, 2025 (5.81 million t, up 13.4% compared to June 2024) and in spite of the increase in apparent consumption over the past nine months (8.32 million t, up 5.9%), those factors have led to a significant increase (9.8%) in the quantities physically present in US warehouses as of March 1, 2026.

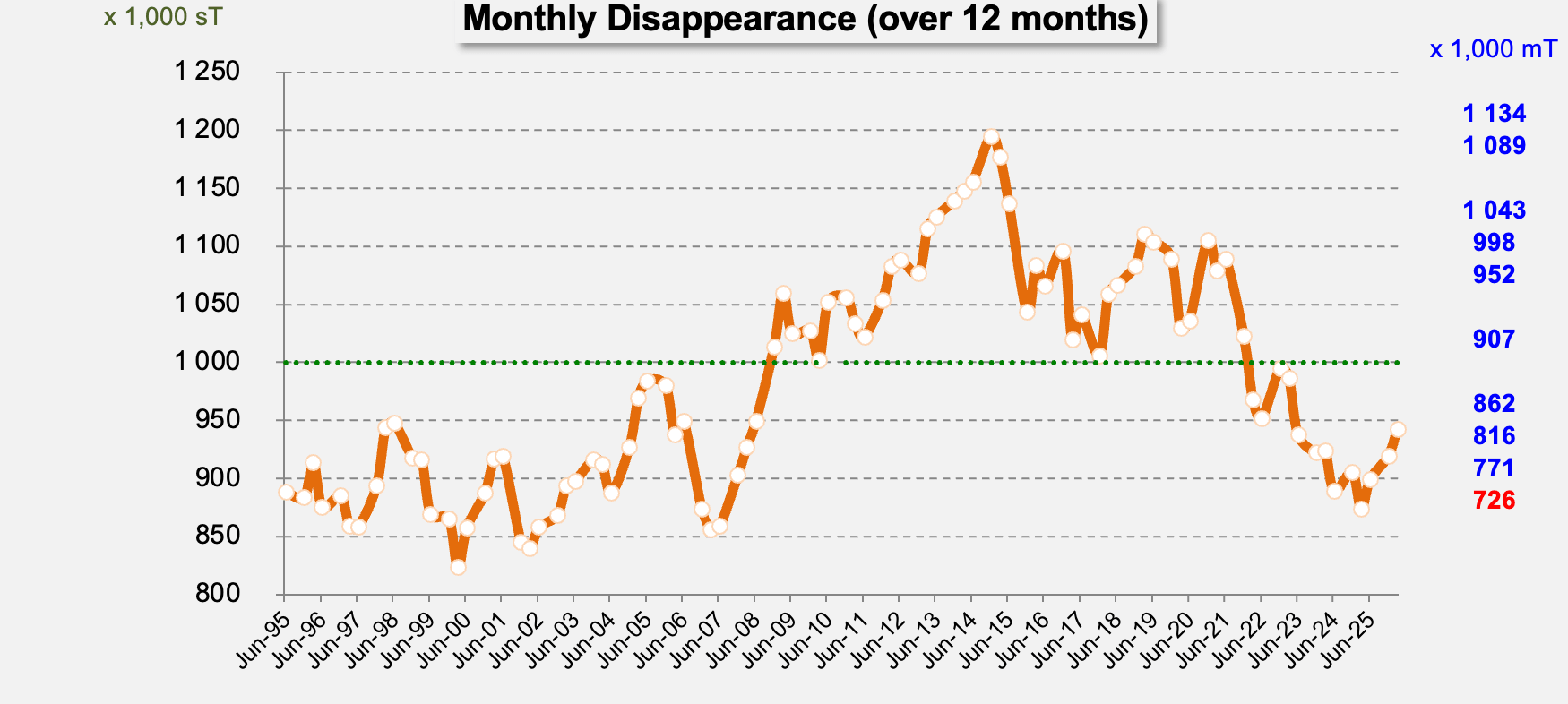

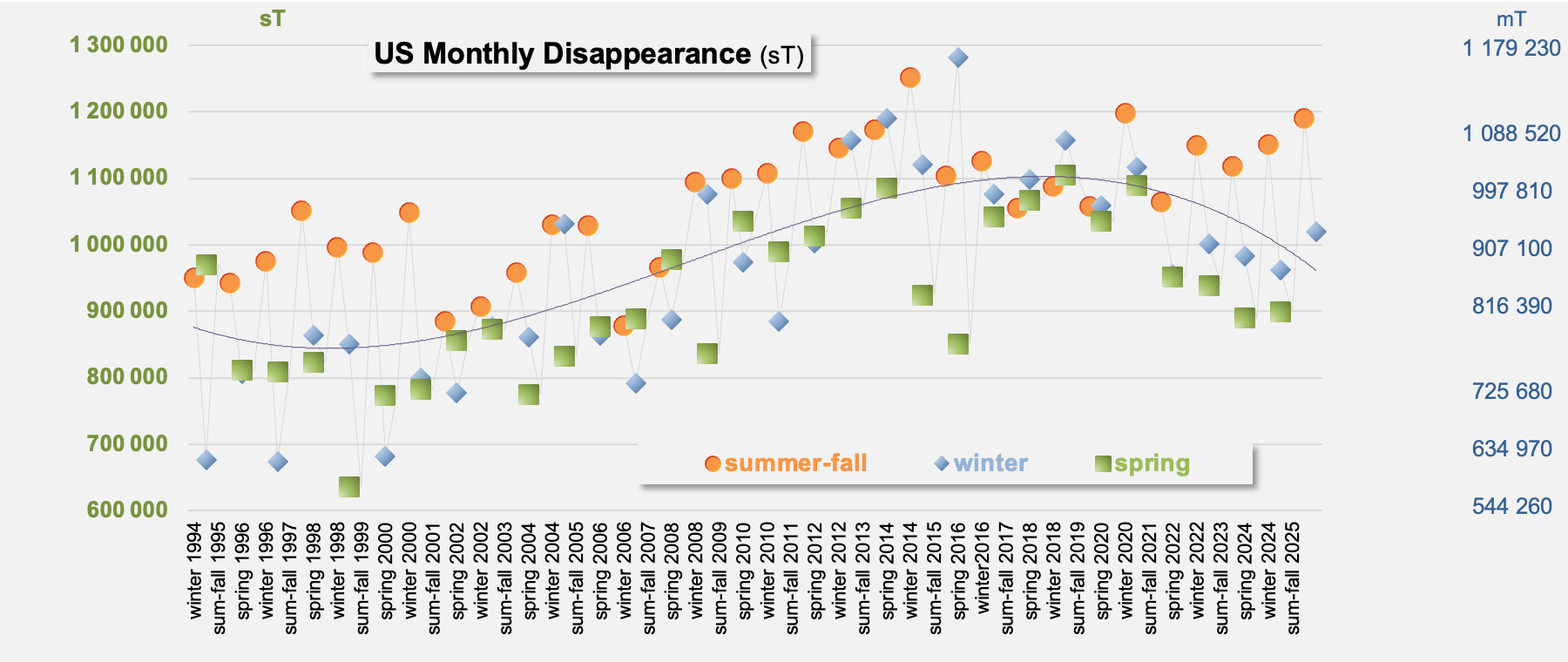

Apparent consumption over the past three months has seen a significant increase: over the past twelve months as a whole, this results in a monthly absorption rate of around 855,000 t, 5,9% higher than that of March 2025 (780,000 t).

The total quantities of tomato products recorded in CLFP stocks (8.504 million t, some of which have already been sold but not yet delivered) show a significant increase (+758,000 t, or +19.8%) compared to March 2025; three-quarters of these quantities consist of tomato paste (6.38 million t), of which 4.34 million tonnes of bulk tomato paste are intended for sale, particularly for export. As of March 1, 2026, tomato paste inventories (for sale and for reprocessing) show a respective increase of 11.1 and 7.9% compared to those in March 2025.

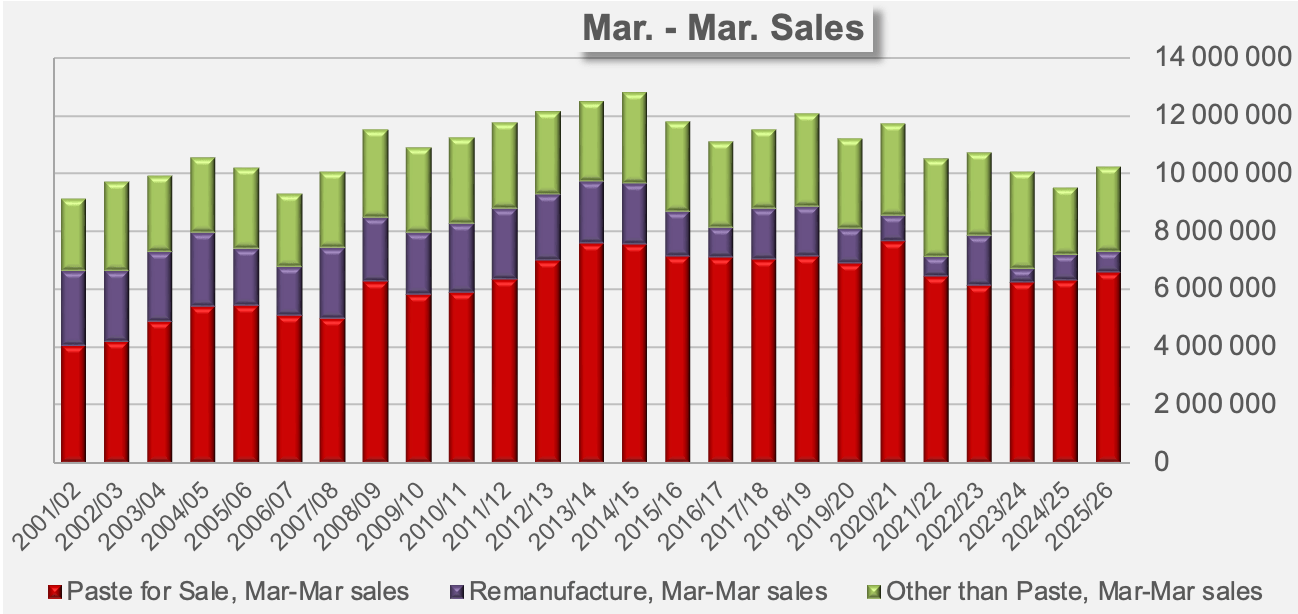

These figures result from annual sales (March 2025-March 2026) estimated at more than 7.3 million tonnes of finished products, a slight increase of 1.5% compared to the rate recorded in March 2025, which combines sales of 6.6 million tonnes of bulk tomato paste (an annual increase of 4.6%) and 0.7 million tonnes intended for reprocessing (a decrease of 27.6% compared to the performance recorded in March 2025).

Alongside the paste sector, annual sales of “other” products have increased by more than 600 thousand tonnes, an increase of more than 21% in one year.

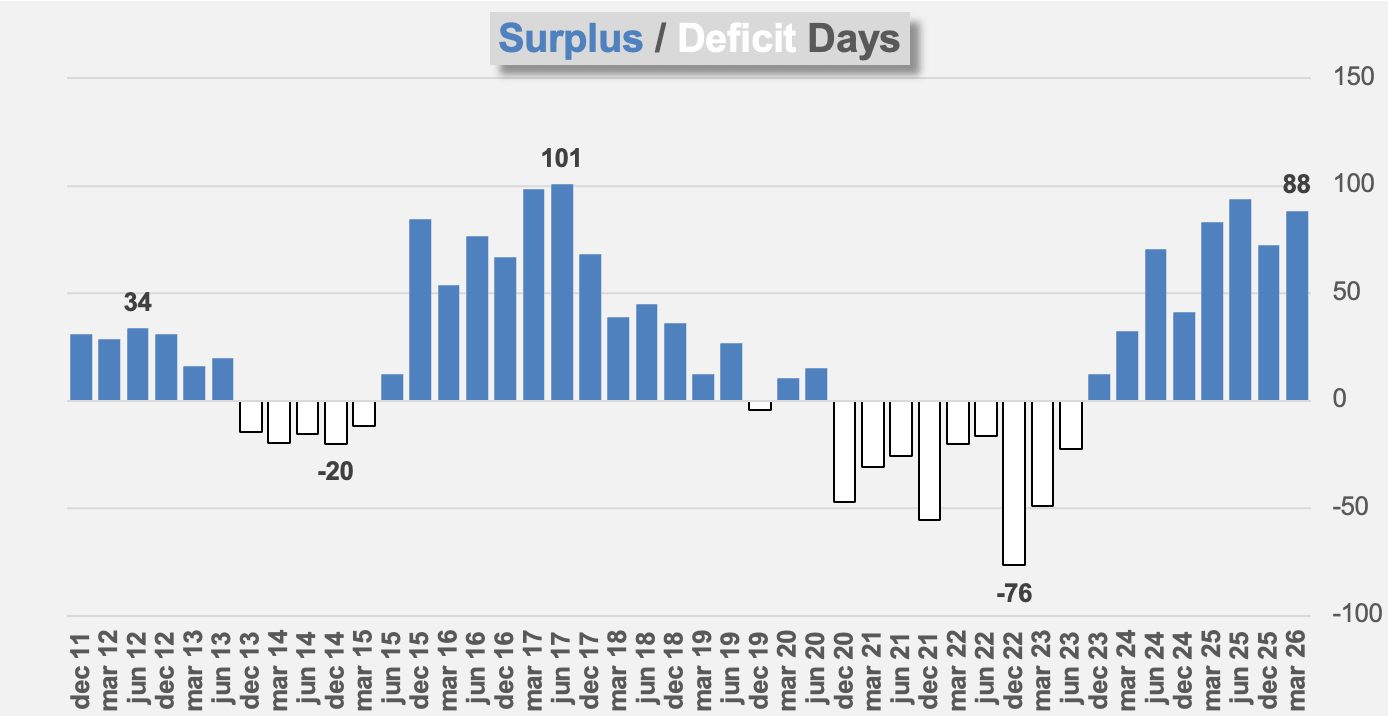

Given the current state (as of March 1, 2026) of available quantities (8.504 million tonnes) and the apparent monthly consumption rate (domestic and exports, 855,000 tonnes), the US industry has quantities equivalent to just under ten months of consumption, a slightly surplus situation compared to the seven-month threshold generally considered satisfactory at the end of winter.

The inventory data as of March 1, 2026, reveals a U.S. tomato processing industry in a position of significant, yet calculated, strength. While the 9.8% year-over-year increase in total stocks to 8.5 million metric tons might traditionally signal a surplus, it serves as a critical buffer during a period of global market sensitivity.

With an apparent monthly consumption rate of 855,000 tons—the highest since 2007—demand remains exceptionally robust. The current supply, equivalent to nearly ten months of consumption, provides a vital insurance policy as the world watches California’s production landscape. This “surplus” is not merely an excess of goods, but a necessary safeguard to maintain market stability and fulfill export commitments in the face of future supply tightening.

Some complementary data

Changes in US stocks of tomato products as of March 1

US monthly apparent consumption of tomato products, summer-fall, winter, and spring components.

Sources: CLFP

{kind=link}