News

United Kingdom, imports: contrasting trends according to the various categories

While purchases of canned tomatoes and sauces from abroad stagnated or decreased, imports of tomato paste soared.

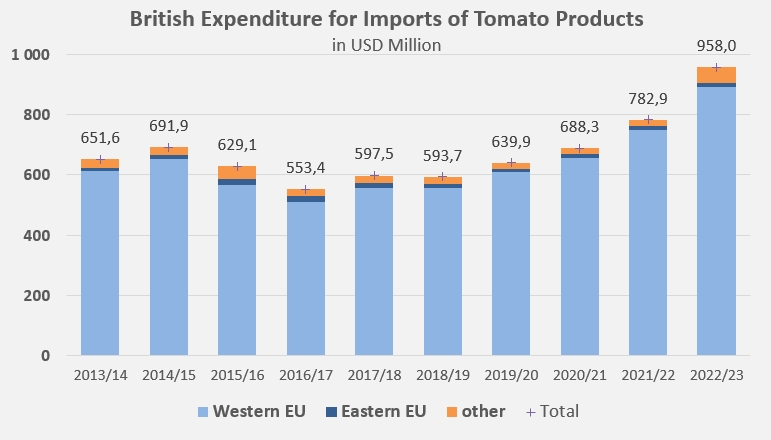

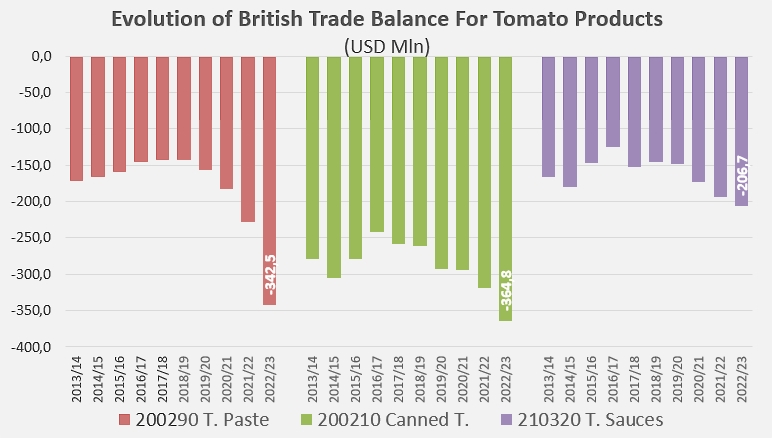

For many years, the UK has been one of the world's leading consumers of tomato products, totally dependent on foreign suppliers for its required quantities. In 2022/2023, its trade deficit exceeded the USD 900 million threshold for the first time (USD 914 million, EUR 871 million).

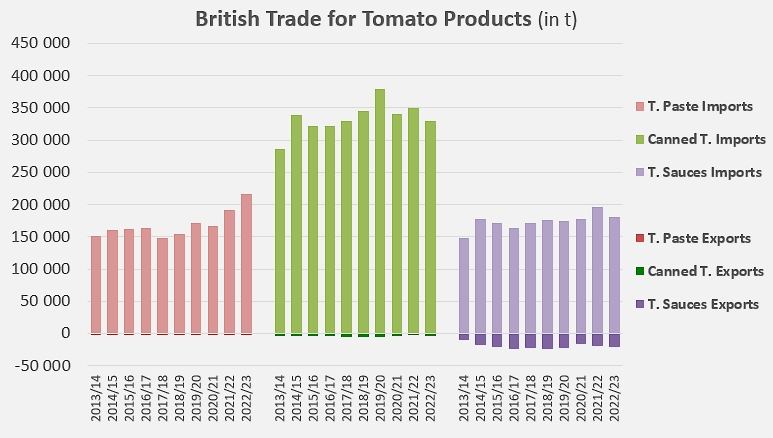

Last year, supplying the British market with tomato products required the import of almost 216,000 metric tonnes (t) of tomato paste (codes 200290), almost 330,000 t of canned tomatoes (codes 200210) and 181,000 t of sauces and ketchup (codes 210320). The quantities absorbed by these last two categories were significantly down on the previous year (-6% for canned tomatoes and -7% for sauces) and on the average for the previous three years (-8% and -1% respectively). In contrast, paste imports have risen sharply in 2022/2023, by 12% compared with the 2021/2022 marketing year and by 22% compared with the period running 2019/2020-2021/2022.

Lastly, a comparison of the year just ended with the three-year period preceding the UK's official exit from the EU (January 31, 2020) and the Covid pandemic (March 11, 2020) reveals an impressive increase (+57,500 t, +36%) in the quantities of pastes imported into the UK, while at the same time, foreign purchases of sauces have risen by just 4% (+7,200 t) and imports of canned tomatoes have fallen by 6% (-22,000 t).

While the various crises that have marked the supply dynamics of the British market in recent years have led to a significant increase in the quantities and, above all, the cost of these foreign purchases, the pre-eminence of European countries in the pool of suppliers has remained virtually unchanged. Over the last five years, European countries, led by Italy and Spain, have supplied 92.8% of the pastes, 98.7% of the canned tomatoes and 98.3% of the sauces shipped to the UK market. However, in 2022/2023, Europe's dominance has been challenged in the categories of tomato paste and sauces, with incursions into those markets from China, the US, Turkey, Israel, Tunisia, Chile and Egypt. These have altered the geographical sourcing profile and raised the share of expenditure to non-EU sources to around 5 to 6% of the total (USD 958 million).

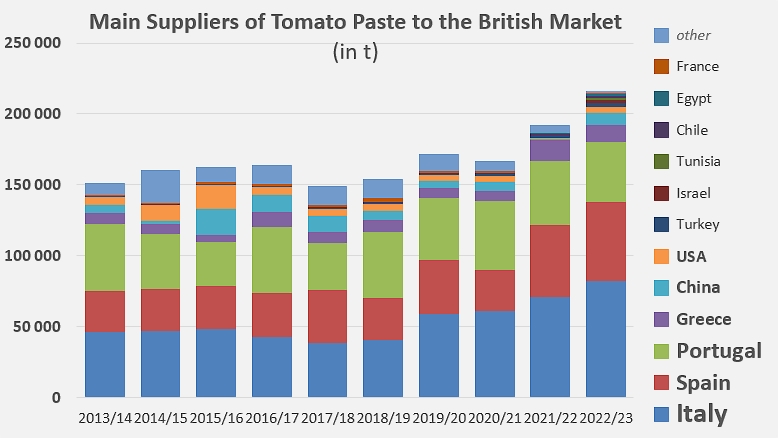

In the paste category, by far the one that has seen the greatest variations in recent years, the increase of over 23,000 t in imports recorded in 2022/2023 has not benefited all sectors that usually export to the UK in the same way.

2022/2023 was a year of growth for Italian and Spanish products, confirming the spectacular progress made by these two countries compared with the previous three marketing years and with pre-Covid performances. In contrast, Portugal's latest results show a noticeable downturn, leaving Portuguese sales to the UK at a level only slightly higher than before the health crisis. Sales of Greek tomato pastes, despite a significant dip compared with the previous year (2021/2022), remain higher than the results of the last three years and well above the pre-Covid period.

All in all, the performance of EU countries on the UK market is likely to remain around one-third higher in 2022/2023 than it was before Covid. But this good performance should not overshadow that of the other major players on the world market, whose UK sales, which had reached a "low point" in 2021/2022, recorded their second-best ever result in 2022/2023, up by 12,000 t (+119%) on the previous three years and by almost 8,000 t (+56%) on the average recorded during the pre-Covid period (2017/2018-2019/2020).

2022/2023 was a year of growth for Italian and Spanish products, confirming the spectacular progress made by these two countries compared with the previous three marketing years and with pre-Covid performances. In contrast, Portugal's latest results show a noticeable downturn, leaving Portuguese sales to the UK at a level only slightly higher than before the health crisis. Sales of Greek tomato pastes, despite a significant dip compared with the previous year (2021/2022), remain higher than the results of the last three years and well above the pre-Covid period.

All in all, the performance of EU countries on the UK market is likely to remain around one-third higher in 2022/2023 than it was before Covid. But this good performance should not overshadow that of the other major players on the world market, whose UK sales, which had reached a "low point" in 2021/2022, recorded their second-best ever result in 2022/2023, up by 12,000 t (+119%) on the previous three years and by almost 8,000 t (+56%) on the average recorded during the pre-Covid period (2017/2018-2019/2020).

Some complementary data

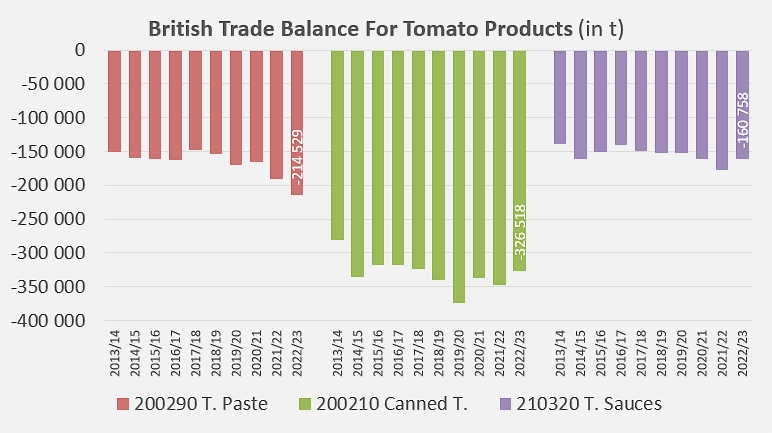

Evolution of UK trade balances for the different tomato product supply categories.

Evolution of UK trade balances for the different tomato product supply categories.

Source: TDM

{kind=link}