News

The US market for tomato products

US tomato products market:

a radical shift is needed

a radical shift is needed

For decades, the US tomato canning industry has been offering consumers "long-life" products of a high quality that is both reliable and regular. These preserved products, which include items like crushed or diced tomato as well as sauces and paste, are among the usual cooking ingredients of American households.

Yet, as far as can be deduced by the information regularly published by the CLFP, the dynamics of apparent disappearance in the US mainly depend on exports, which have been "assisting" the domestic market for the past seven or eight years while it has been searching for a second wind… Because of the economic and commercial mechanisms, which have been extensively commented in recent months, these foreign sales have not been able to act as the drivers or "buffers" that they could have in the second half of 2015, and the US industry has found itself, for the time-being at least, lacking adequate outlets.

What are the reasons for which national US consumption – which is currently of such high importance – has been slowing in recent years? Local experts have confirmed: the canned tomato sector, one of the major components of the US domestic market for tomato products, has been undergoing major difficulties in recent years, and this has slowed its development. These difficulties stem from the changes in attitudes and purchasing behavior of consumers, and they currently have a major impact on the commercial context of the tomato processing industry in the United States, and will probably continue to do so for many years.

What are the reasons for which national US consumption – which is currently of such high importance – has been slowing in recent years? Local experts have confirmed: the canned tomato sector, one of the major components of the US domestic market for tomato products, has been undergoing major difficulties in recent years, and this has slowed its development. These difficulties stem from the changes in attitudes and purchasing behavior of consumers, and they currently have a major impact on the commercial context of the tomato processing industry in the United States, and will probably continue to do so for many years.

A segment under pressure

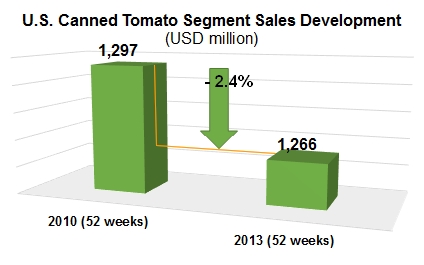

Like with many other food segments displayed on the shelves of the "center store*", canned tomato products have in recent years been recording disappointing sales performances. According to the data provided by AC Nielsen and quoted in a report published by SIG Combibloc, the category recorded a 4.2% drop in volume between 2010 and 2013. Along with the decrease in the number of units sold, tomato products also underwent a 2.4% erosion of their sales value over the same period.

Like with many other food segments displayed on the shelves of the "center store*", canned tomato products have in recent years been recording disappointing sales performances. According to the data provided by AC Nielsen and quoted in a report published by SIG Combibloc, the category recorded a 4.2% drop in volume between 2010 and 2013. Along with the decrease in the number of units sold, tomato products also underwent a 2.4% erosion of their sales value over the same period.Whereas a number of factors can influence the sales value of canned tomatoes, the experts recognize that the segment is currently having to face an extremely detrimental banalization, which has been actively aggravated by massive promotions on prices (for example, "10 cans for just 10 USD") and the growing share occupied by private label products in the supermarket aisles.

This penetration of private labels in the tomato products segment amounted to about 44% in 2013, a significantly higher proportion than the average level of penetration of private labels, at 23%, in the US retail food sector as a whole. These two trends (low prices and standardization) are two of the main reasons that lead consumers to increasingly consider tomato products as undifferentiated products, with no real identity, and which cannot present any justification for a high purchase price. Only the sub-segments that provide specific quality features, like organic tomato, a few imported products or some specialties from select brands, are still able to demand a "higher end" retail price.

This penetration of private labels in the tomato products segment amounted to about 44% in 2013, a significantly higher proportion than the average level of penetration of private labels, at 23%, in the US retail food sector as a whole. These two trends (low prices and standardization) are two of the main reasons that lead consumers to increasingly consider tomato products as undifferentiated products, with no real identity, and which cannot present any justification for a high purchase price. Only the sub-segments that provide specific quality features, like organic tomato, a few imported products or some specialties from select brands, are still able to demand a "higher end" retail price.

Shifting clientele and a lack of real innovation

Shifting clientele and a lack of real innovationThe shrinkage of sales volumes and value for the tomato products segment is an illustration of the changes that are afoot in the ways people consume and in the attitudes of buyers to the "center shop" and to preserved food products in general. It is increasingly obvious that Generation Y consumers (or millennials), born between the early 1980s and the early 2000s, thanks to their influence and their growing buying power, will be the ones to decide on these shifts in purchasing behavior, and will dictate in coming years their preferences in terms of products. This population segment currently includes 80 million consumers in the United States who enjoy an annual buying power valued at approximately USD 600 billion. It is estimated that this amount will reach 1 400 billion by 2020, and that it will then account for a third of total retail sales. According to a survey carried out by the Hartman group, "Millennials predominantly characterize their food and beverage brands and product choices as more healthy, organic, and natural. They also indicate an expectation of higher prices for higher-quality food and beverage experiences."

Brand owners in other categories of preserved foods on offer in the center store have decided to innovate (often successfully), guided by a specific approach to packaging and to the concept, or to the use of products, in order to grab the attention of consumers and keep it. The classic example is broths, which is a segment that has really taken off thanks to a complete rethink of the conditioning and a much wider range of suggested uses. At the same time, brands have put pressure on distributors to get them to move their products from center store to the aisles on the perimeters, in order to stay tuned in to shifting customer habits.

In sharp contrast with these innovative approaches, the tomato products category has seen very limited innovation over the past decade. In 2013, 99% of all tomato products were still being offered in nothing but a metal can, and the segment seemed to be inseparably linked to the traditional center store aisles. For several years, no real innovation or extension of the range (in terms of products, conditioning or usage) has occurred to shake up the world of the canned tomatoes being offered to consumers: the main sales features put forward have been linked to the brand and its promise of quality, to the origin of raw materials, to the type of product (paste, diced tomato, crushed tomato, sauce, whole-peeled tomato, etc.) and to price promotions. To quote a report put out by SIG Combibloc, "the total sum of innovations in the segment has been flavor variations and the use of on-pack claims." From the consumer's point of view, the industry has not done any more than that to put forward new arguments in order to increase the number of sales or the product value, or to develop the volume of tomato products consumed.

The challenge of using the technology of aseptic carton packs

Unlike European offers, which have been extremely varied and diversified for several decades in terms of products and packaging, the canned tomato products on offer to US consumers are mostly sold in traditional metal cans, whereas requirements in terms of packaging have clearly evolved. An immediate consequence of this situation is that consumers consider it is not justified to pay a higher price for canned tomatoes, as they are a basic product, a fact that limits their sales price to a range that is generally of a relatively low level.

Unlike European offers, which have been extremely varied and diversified for several decades in terms of products and packaging, the canned tomato products on offer to US consumers are mostly sold in traditional metal cans, whereas requirements in terms of packaging have clearly evolved. An immediate consequence of this situation is that consumers consider it is not justified to pay a higher price for canned tomatoes, as they are a basic product, a fact that limits their sales price to a range that is generally of a relatively low level.

In an analysis published last year, SIG Combibloc also pointed out the large number of products that are very similar, with very few differentiating features, and underlined the virtual absence of premium products.

Tim Kirchen, Head of Marketing and Business Development with SIG Combibloc North America, states that "these days, US consumers look at food packaging differently from the way they did five years ago. Especially millennials, those consumers born from the early 1980s to the early 2000s, are beginning to understand that packaging not only has a protective function, but it should also be a sound choice in commercial and environmental respects. In the US, food waste is a major issue and consumers want packaging units that match their own needs. It's in the nature of things that a single-person household or one with elderly people needs smaller portion sizes than a family. And environmental awareness is also playing a more important role in the US. Eco-friendly packaging made from renewable raw materials is increasingly sought-after. This is where aseptic carton packs for foods and beverages come into play."

As shown by the comparative data published in a previous report (see the January 2016 issue of Tomato News), aseptic carton conditioning technology is very well positioned among the many options that could provide concrete innovative solutions for US processors who want to re-energize their offer in the canned tomato segment and adapt the product/packaging tandem to the requirements of their domestic market. The carton pack also carries with it a number of sales arguments that are a good fit with current social and environmental concerns (ecological impact, consumption of fossil fuels, recyclability, etc.), supported by many Life Cycle Assessments. It is therefore likely to attract the attention of populations that are currently in a situation to consume and will continue to do so in future years.

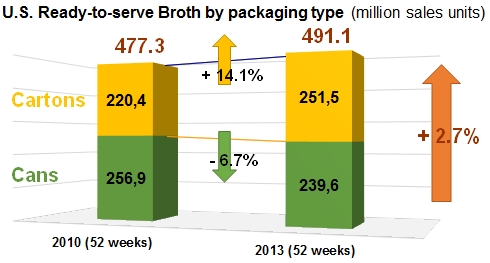

Returning to the example of ready-to-use broths and stocks, which had previously only been available in a metal-can version, data provided by AC Nielsen shows that between 2010 and 2013, the part of this segment that was conditioned in aseptic cartons increased by 14.1%, and that this development drove a growth rate of the broth sector – for all packaging types – of 2.7% over the period considered. This episode promoted aseptic carton packs to the top of the conditioning methods used by the sector, well ahead of metal cans.

The use of aseptic carton packs for a number of tomato products is a well-established concept. As early as 1985, aseptic cartons were being used in Italy, to condition diced tomatoes and sauces. Since then, aseptic cartons have progressively increased their market shares in Europe and been adopted by key brands like Pomi, Knorr, Nestlé and Heinz. In 2013, the market share held by aseptic cartons already accounted for 19% of the canned tomato market, a proportion that has increased since aseptic carton packs have been adopted by processors for their products intended for retail sale, as they were convinced of the advantage in terms of efficiency and of a better match with shelf-life requirements. This is the kind of argument that convinced Sainsbury's to switch in 2010 from tin cans to aseptic carton conditioning for its whole range of tomato products under private label, in order to reduce the volume of its packaging. The example of this British retailer has now been followed by a large number of European distribution chains.

The issue of differentiation on the shelves

In addition to the aging concept of the metal can, tomato products sold on the US market suffer from an obvious lack of differentiation on store shelves. Market experts are used to saying that "consumers face a uniform wall of metal cans". With its original block shape and its "advertising sign" effect, carton packaging can represent a "noticeable" alternative on the shelf where tomato products are sold. Furthermore, the aseptic carton solution can improve sales and profitability performances: the oblong shape of the packs can lead to a 40% saving of space on the shelves, compared to tin cans, meaning that more space can be freed up for front-facing visibility of the products in any given sales context, thereby minimizing the need for redisplay and lowering handling costs.

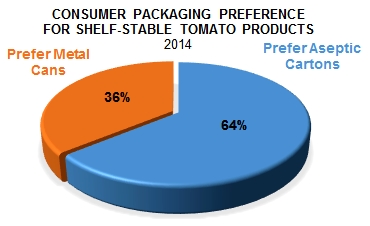

According to Tim Kirchen, "the segments that are most likely to evolve and progress in terms of growth are the ready-to-use tomato products and premium soups. Consumer surveys have shown that, in customers' minds, carton packs are associated with greater quality, organic products and premium brands." A study carried out by Perception Research Services in 2014 actually showed that 65% of American consumers prefer carton packs for the conditioning of tomato-based products.

For the head of SIG Combibloc North America, "More and more consumers are finding out about the great strengths of carton packs – their convenience, their product protection qualities and their good environmental characteristics. In the future, this will outweigh the fact that in the United States carton packs as a packaging solution are not yet on all consumers’ radars. We’re very confident that carton packs are becoming much more widely known and accepted, and in the US and Canada too, they will be more than just a packaging alternative for long-life foods. From 2012 to 2016, we’re anticipating a growth rate of more than 10% for long-life food products in carton packs."

For the head of SIG Combibloc North America, "More and more consumers are finding out about the great strengths of carton packs – their convenience, their product protection qualities and their good environmental characteristics. In the future, this will outweigh the fact that in the United States carton packs as a packaging solution are not yet on all consumers’ radars. We’re very confident that carton packs are becoming much more widely known and accepted, and in the US and Canada too, they will be more than just a packaging alternative for long-life foods. From 2012 to 2016, we’re anticipating a growth rate of more than 10% for long-life food products in carton packs."

A viable and well-accepted alternative

Aseptic carton packs have clearly progressed in terms of their acceptance among consumers and therefore represent a viable and trustworthy alternative among the conditioning choices that are available in the current technological context in the USA. Surveys carried out among American consumers have shown that:

- The products presented in aseptic cartons are perceived as fresher and more nourishing than those presented in traditional packagings;

- They are perceived as being of higher quality;

- The carton pack is considered as a packaging solution that is more eco-friendly;

- The carton pack is perceived to make handling easier, compared to the usual packagings for tomato products.

Even more encouraging, the study showed that, in their buying habits, consumers take account of the value mark-up of a tomato product depending on the type of conditioning: the interest of a consumer for a product remains high even when the price of the product in an aseptic carton is 20% higher than an equivalent product in a metal can. So it is not surprising that pioneering US retail chains like Whole Foods and Trader Joe's are distributing significantly higher volumes of food products conditioned in carton packs, in order to respond to the demand of buyers who are sensitive to issues of quality, shelf-life and freshness. Furthermore, convenience is likely to play a leading role in purchasing behavior: the wide variety of safe and easy opening systems ("twist caps", "pre-perforated", etc.) available with carton packaging represents an important argument for brands that are concerned with responding to consumer expectations.

For processors of the US tomato industry, the "aseptic carton pack" approach, which has already shown its worth in terms of innovation, growth and enhanced value, should become a vector for change and greater consumer proximity; and it could support a retail pricing “trade-up strategy” for higher performance processing equipment, compatible both with the requirements of the market and with the economic constraints of the business.

Getting a trend started

The concept of conditioning tomato products in aseptic carton packs was first introduced to the United States by Pomi products, imported from northern Italy where they are processed by one of the Italian leaders of the sector, the Consorzio Casalasco del Pomodoro. Pomi managed to build a regular customer base and developed its penetration of the retail market.

After that, typical American brands like ConAgra launched tomato products conditioned on the same model. The first tomato products filled in aseptic carton packs on US soil were varieties of chopped tomatoes (diced or crushed), launched in 2013 by premium tomato product brands Dei Fratelli and Cento.

Co-packing: a solution for progressive change

To add a new packaging solution to their portfolio, food manufacturers do not need to invest directly – and at high cost – in their own filling and packaging lines. Co-packing is an intermediary and progressive solution that can enable them to add new products to their range. Manufacturers can contract out conditioning operations to allow them to bring products to the market in innovative packaging solutions according to consumer trends. In the United States, the Hirzel Canning Company, for instance, offers co-packing options, and has decided to depend on the flexible technology of SIG Combibloc packing equipment.

According to Tim Kirchen: "For food manufacturers, another crucial requirement is that a packaging system and the corresponding filling machines offer a high level of flexibility, […making it] possible to change volumes, formats and products in unmatched short time," thereby keeping production extremely flexible and profitable.

Durability, human health and purchasing habits

The new and growing awareness of consumers to arguments linked to durability and health (quality and nutritional content, freshness of the products, etc.) are to be seen as a long-lasting development that US operators need to take into account. Clearly, millennial consumers have literally shifted their attention towards brands and products that match their increasingly intentional lifestyle. This type of approach is fundamentally altering the way consumers see and evaluate product and packaging choices: this population of highly aware consumers drives trends that evolve rapidly and is always seeking new products, but also ones that are available in alternative conditioning options that correspond to their concept of consumption and fit their expectations in terms of shelf-life, freshness, food safety and health benefits. And it is now accepted that the metal can, as the standard packaging form for tomato products, must face up to some new challenges, given that it is no longer able to properly meet the legitimate requirements of consumers.

For the initiators of this survey, the US tomato products industry has come to a crucial turning point in its history. Most of its business depends on a domestic market that has been stagnating in recent years, even shrinking, in terms of consumption, and this is demonstrated by the drop in commercial value and in the overall turnover of the industry. The segment has long been constrained by its limited offer and lack of product differentiation and of perceived value according to packaging formats. So with the fairly recent arrival of new types of packaging and new products on the domestic market, the US industry will face increasing pressure from a dynamic proportion of demanding consumers, who are expecting their purchasing and consumption habits to be properly and fully addressed by the tomato canning industry.

For the initiators of this survey, the US tomato products industry has come to a crucial turning point in its history. Most of its business depends on a domestic market that has been stagnating in recent years, even shrinking, in terms of consumption, and this is demonstrated by the drop in commercial value and in the overall turnover of the industry. The segment has long been constrained by its limited offer and lack of product differentiation and of perceived value according to packaging formats. So with the fairly recent arrival of new types of packaging and new products on the domestic market, the US industry will face increasing pressure from a dynamic proportion of demanding consumers, who are expecting their purchasing and consumption habits to be properly and fully addressed by the tomato canning industry.

US processors will need to adapt their product offer and their filling options in order to satisfy an ever more demanding market, and extend the potential usage and value of tomato products, failing which the segment is likely to continue its decline.

Some complementary data

* Center store: the aisles of a supermarket that are generally used for displaying ambient foods, like cans and jars, drinks, confectionery, coffee and tea, etc., in contrast with fresh products, delicatessen ranges, freezer aisles, and chilled or positive cold ranges (milk and dairy products, meats and meat-based products, fish, etc.).

{kind=link}