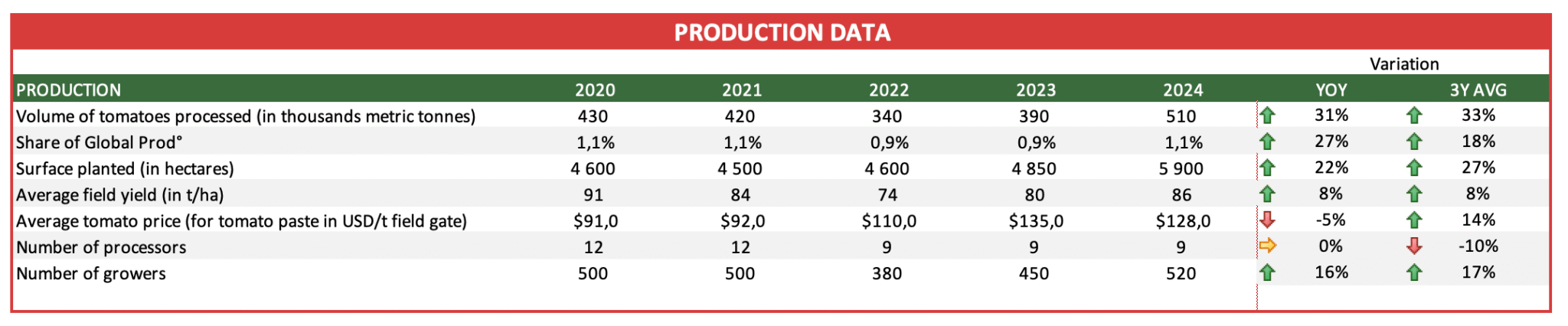

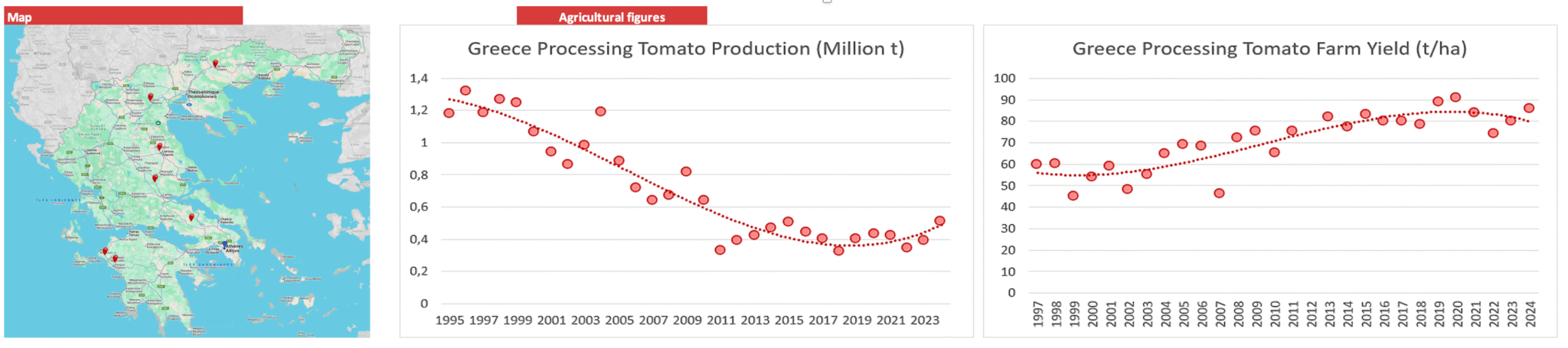

With about half a million tonnes processed annually in the mid 2020’s, tomato production in Greece is currently back on an upward trend after years of decline after heydays of about 1.2 million tonnes processed annually in the 1990s. The industry has now restructured itself with fewer but stronger industries and in highly productive areas, promising efficient, low-cost production with high quality diversified products.

Greece is a very mountainous country and agricultural acreage only covers a little more of 10% of the total surface of the country. Processing tomatoes are mainly grown in plains close to rivers and lakes or in regions surrounded by mountains.

Currently, most of the growing and processing is carried out in three geographical areas:

- The Central region (Thessaly and Boeotia), with about 75% of the production but only about 50% of the total surfaces thanks to the excellent agricultural yields (100 to 110 t/ha) achieved by local growers. The region offers arable land stretching over some 100 000 hectares, of which about 3 000 are currently dedicated to growing processing tomatoes, offering a potential for further growth.

- The Peloponnese which accounts for about 20% of the production. The performances of processing tomato growers in the north-eastern part of the Peloponnese have noticeably progressed in recent years to achieve average yields of up to 90 t/ha. Most of the crops are within a 15 to 40 km radius around the processing plants, and the companies that are active in the area focus particularly on their relationships with medium to large sized growers (20 to 60 hectares) by encouraging the planting of a smaller number of larger sized fields.

- The Northern Region (Macedonia-Thrace), with about 5% of the production. This area has seen a dramatic drop in production due to the fact that a lot of industries in the area closed.

Drip irrigation is generalised and represents more than 95% of the surfaces. Soils are medium type with variable predominance of clay and sand, rich in organic matter and well drained. Fields are varying from area to area, with the more traditional areas around 10 hectares and the newest areas around 25 hectares. Seeds utilized are almost 100% hybrids and transplants account for about 95 % of the surfaces. Thanks to the intensive work carried out by both factories and local growers’ organizations, the yields and fruit quality are steadily increasing.

There are currently nine processing factories in Greece, with the four largest ones handling over 80% of the total volume. The country is proud to have two companies with a history of over 100 years, having been founded in 1915. The long and rich processing history of the country is presented in detail at the Industrial Tomato Museum in Santorini, established in 2014, where one of the oldest tomato factories in the country was converted into an Industrial Museum dedicated into offering its visitors a journey back to the industrial past.

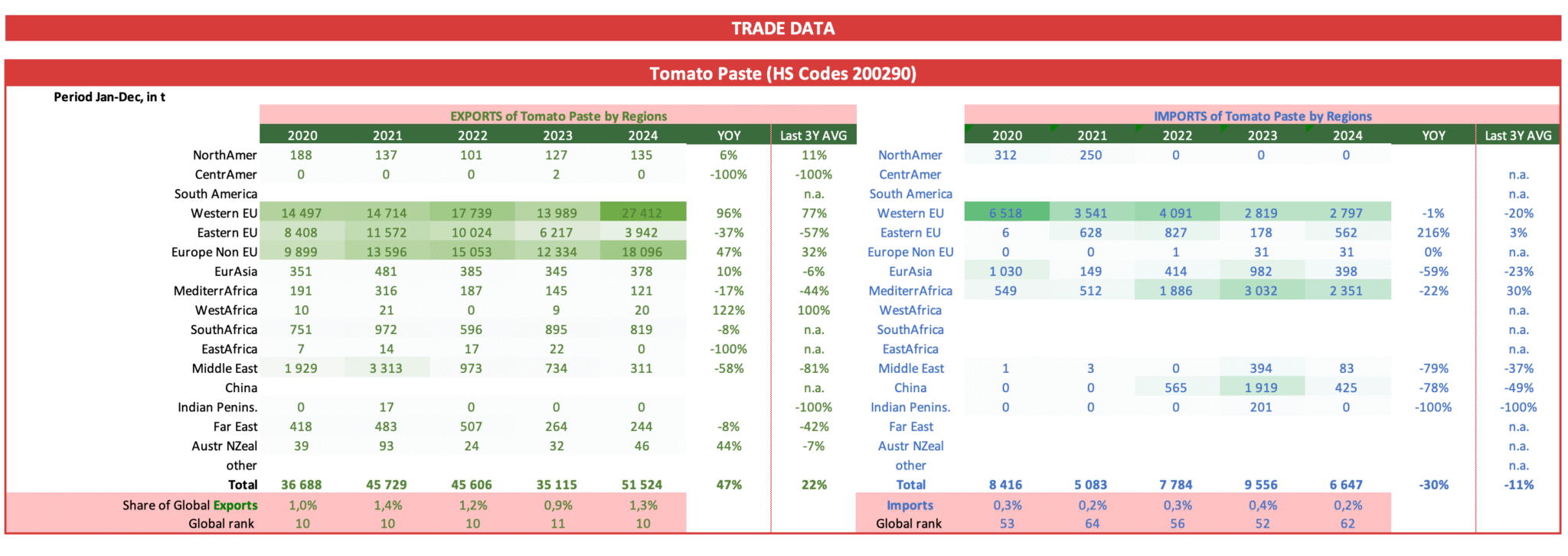

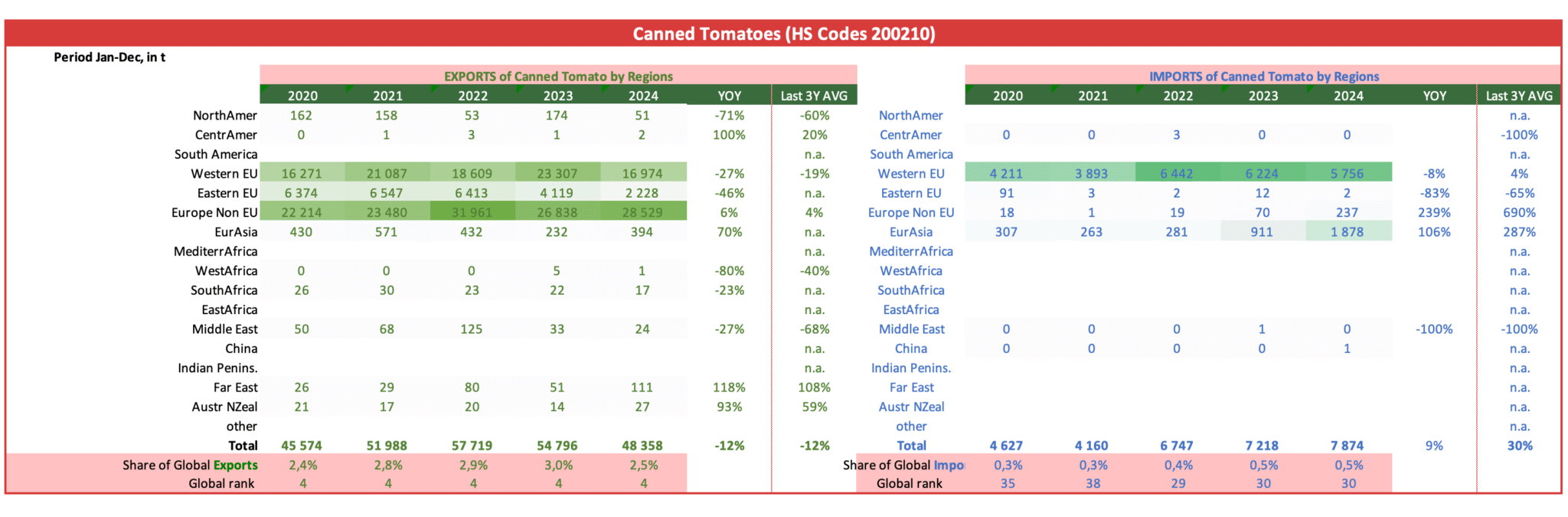

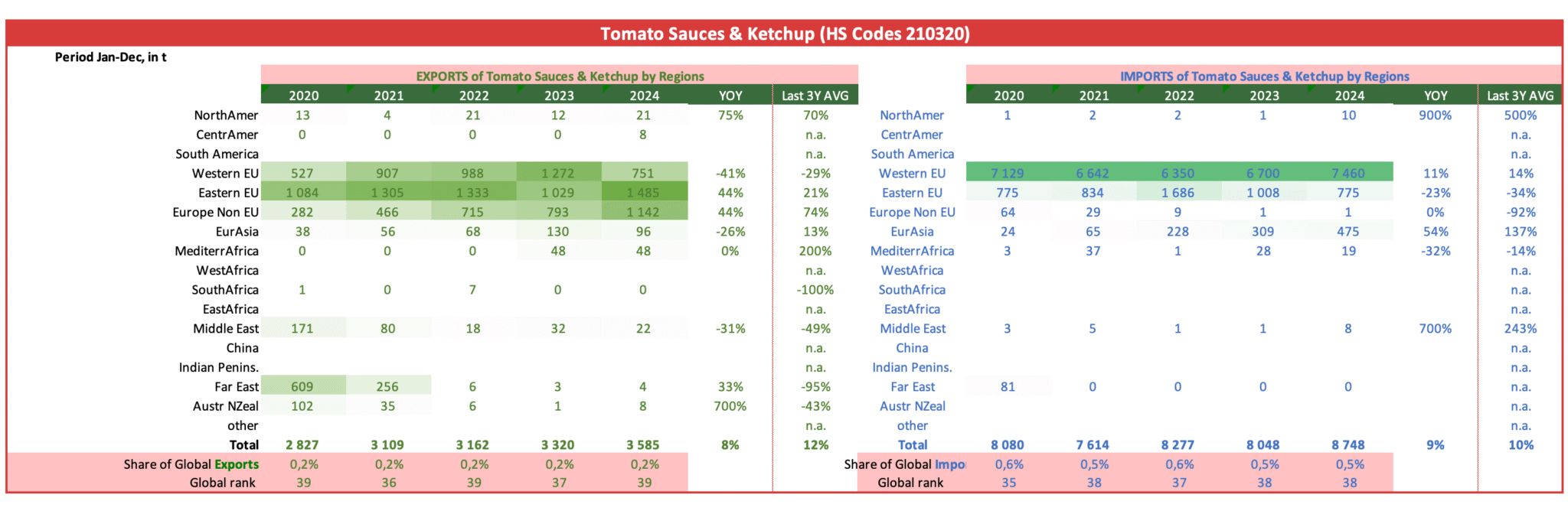

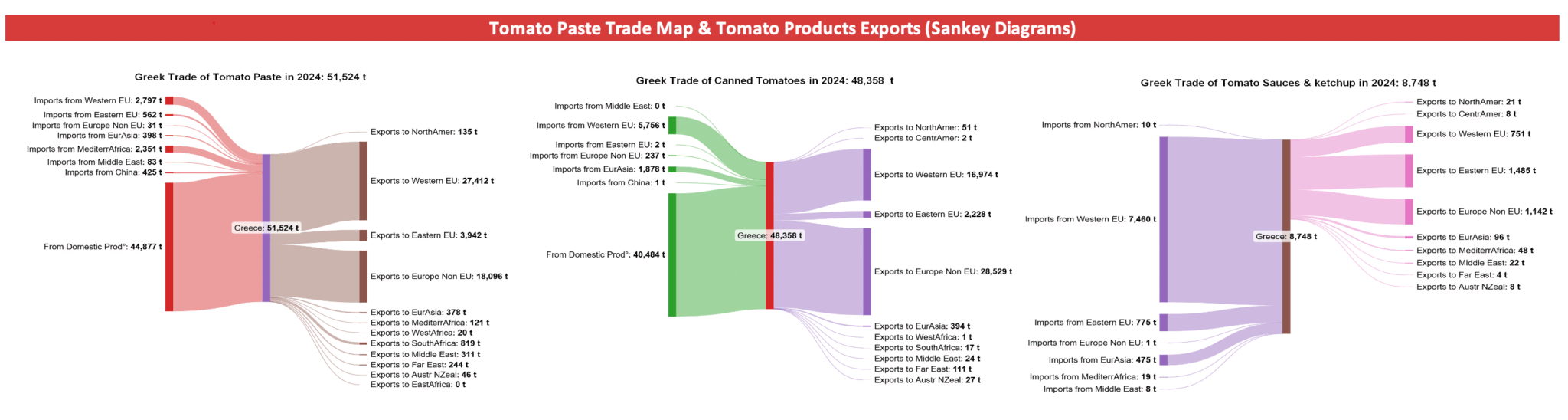

The Greek production is predominantly export oriented (about 70% of the total volume). The majority is high quality industrially packed tomato products, like paste, diced, sauces etc. in aseptic bulk packaging. Major export markets are the European Union and other European countries, with smaller volumes to Japan and Gulf countries. A significant part is also packed in retail sizes destined both to domestic market as well as to exports.

PEK

The Greek industry is represented within the AMITOM and WPTC by PEK, the Greek Canners Association. Established in 1945, it is a founding member of AMITOM. Its members companies account for about 65-70 % of the total Greek production.

(click on any of the images to expand it)