News

Carbon Pricing State and Trends for Agribusiness

The freshly minted World Bank report on the state and trends of carbon pricing in 2026 confirms that environmental compliance has officially cemented itself as a core economic pillar of international trade. For the global tomato processing sector, an industry structurally reliant on extensive thermal energy for paste concentration and perfectly timed supply chains, these updates represent shifting baselines for global competitiveness.

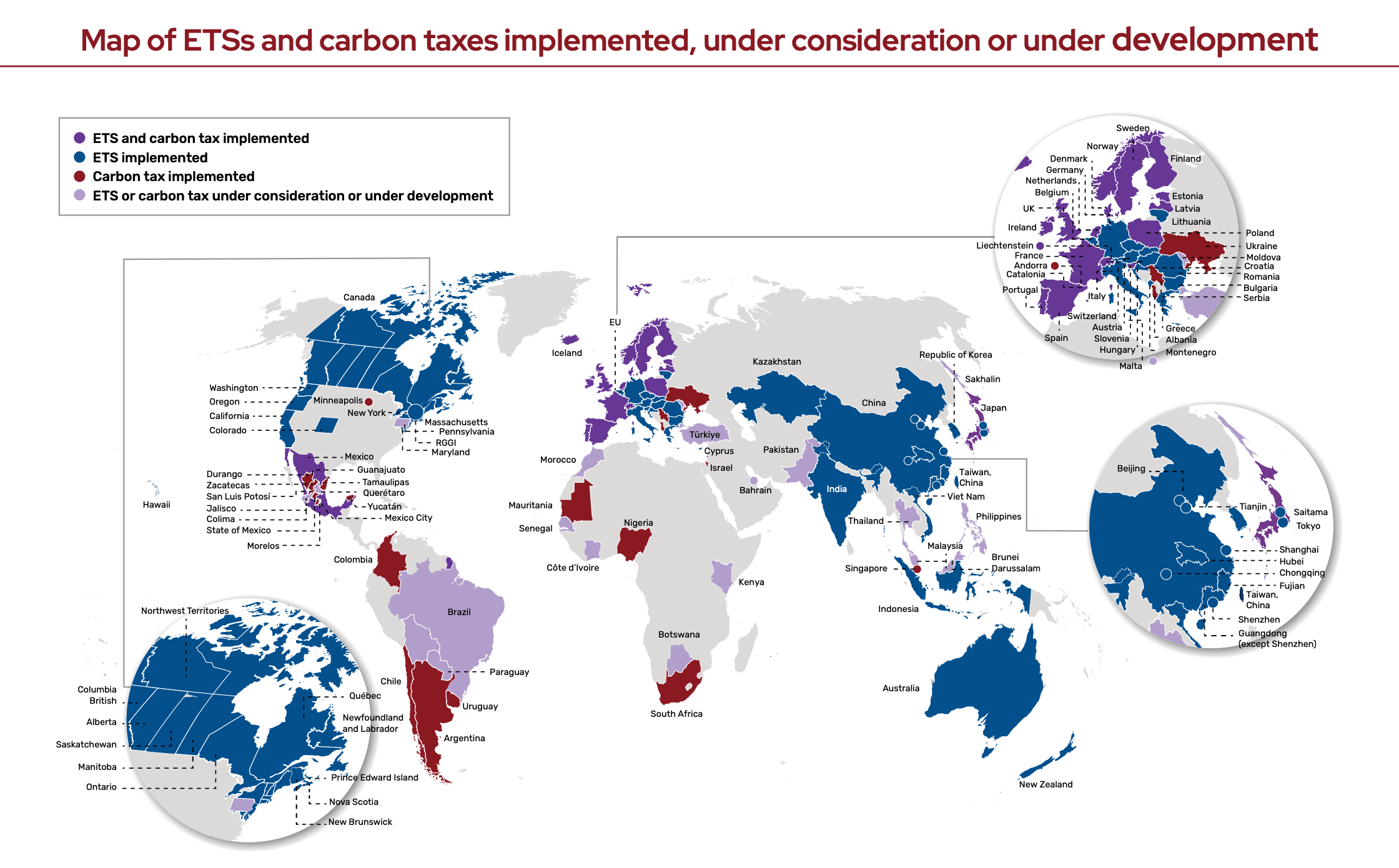

When analyzing the comprehensive global map provided in the report, the rapid spread of compliance frameworks becomes visually undeniable. Regional policies are no longer confined to historical European borders, as major processing and agricultural hubs across the Americas, Asia, and the Mediterranean basin have implemented or are actively developing their own Emissions Trading Systems and carbon taxes.

For us, this expanding grid changes the calculation for cross-border logistics. As major import regions progressively penalize the embedded emissions of industrial goods, exporting countries are establishing domestic mechanisms to capture those tax revenues locally rather than forfeiting them at foreign arrival ports. This transition means that operating in an entirely unregulated territory is fast becoming a thing of the past, requiring processors worldwide to track carbon policy with the same rigor they apply to traditional trade tariffs.

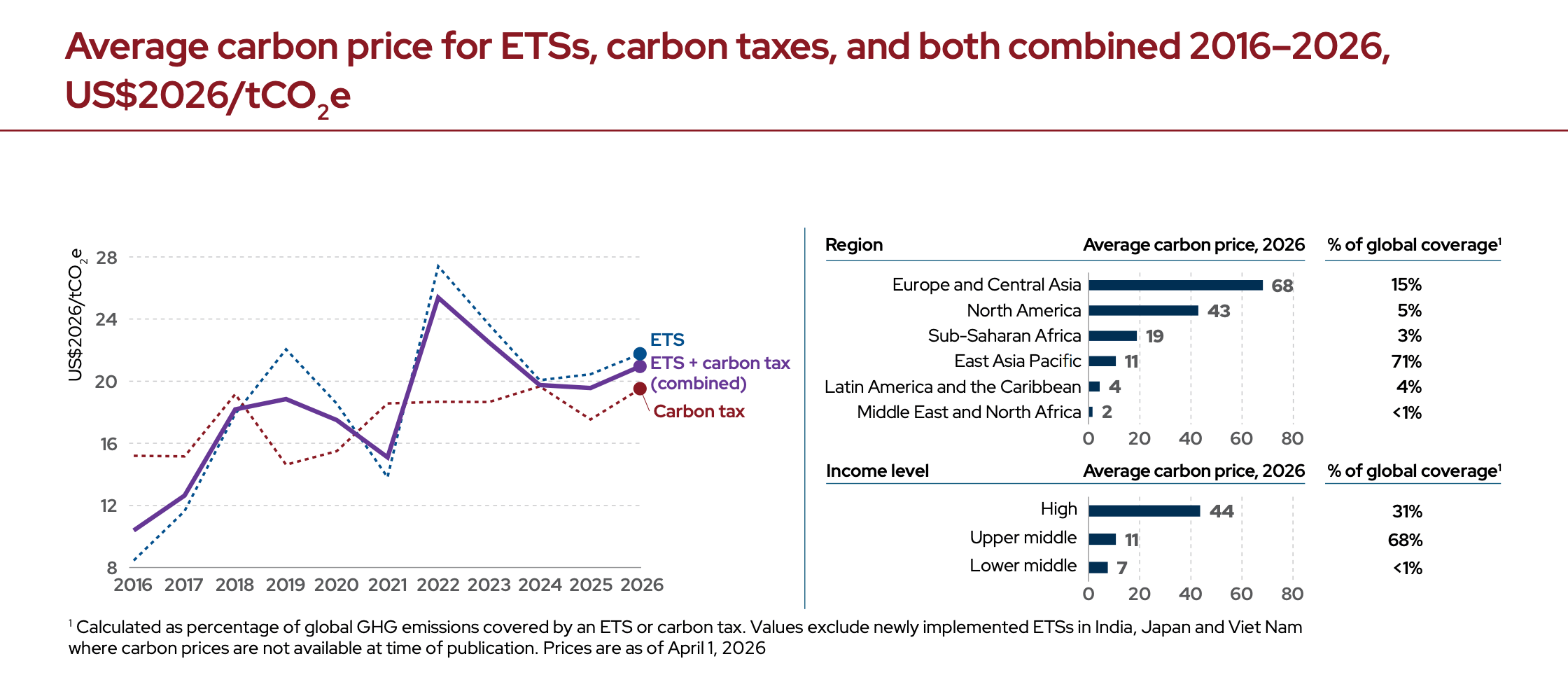

The practical financial weight of these regulations is clearly charted on this chart, which tracks the average carbon price across different pricing systems. Globally, the combined average cost has climbed toward a new baseline, but the critical narrative for agribusiness lies in the stark geographical and income-level disparities. Industries operating within Europe and Central Asia face steep costs averaging sixty-eight dollars per metric ton of CO2 equivalent, whereas competitors in East Asia Pacific or Latin America navigate vastly lower regional baselines of eleven dollars and four dollars respectively.

Because transforming raw tomatoes into concentrated paste is inherently energy-intensive—requiring continuous industrial steam usually derived from gas—this pricing gap influences the bottom-line margin of every ton produced. While lower-income processing regions currently maintain a cost cushion, the ongoing implementation of border adjustment taxes by high-price jurisdictions is explicitly designed to level this playing field, forcing all global actors to look toward thermal efficiency as a baseline economic defense.

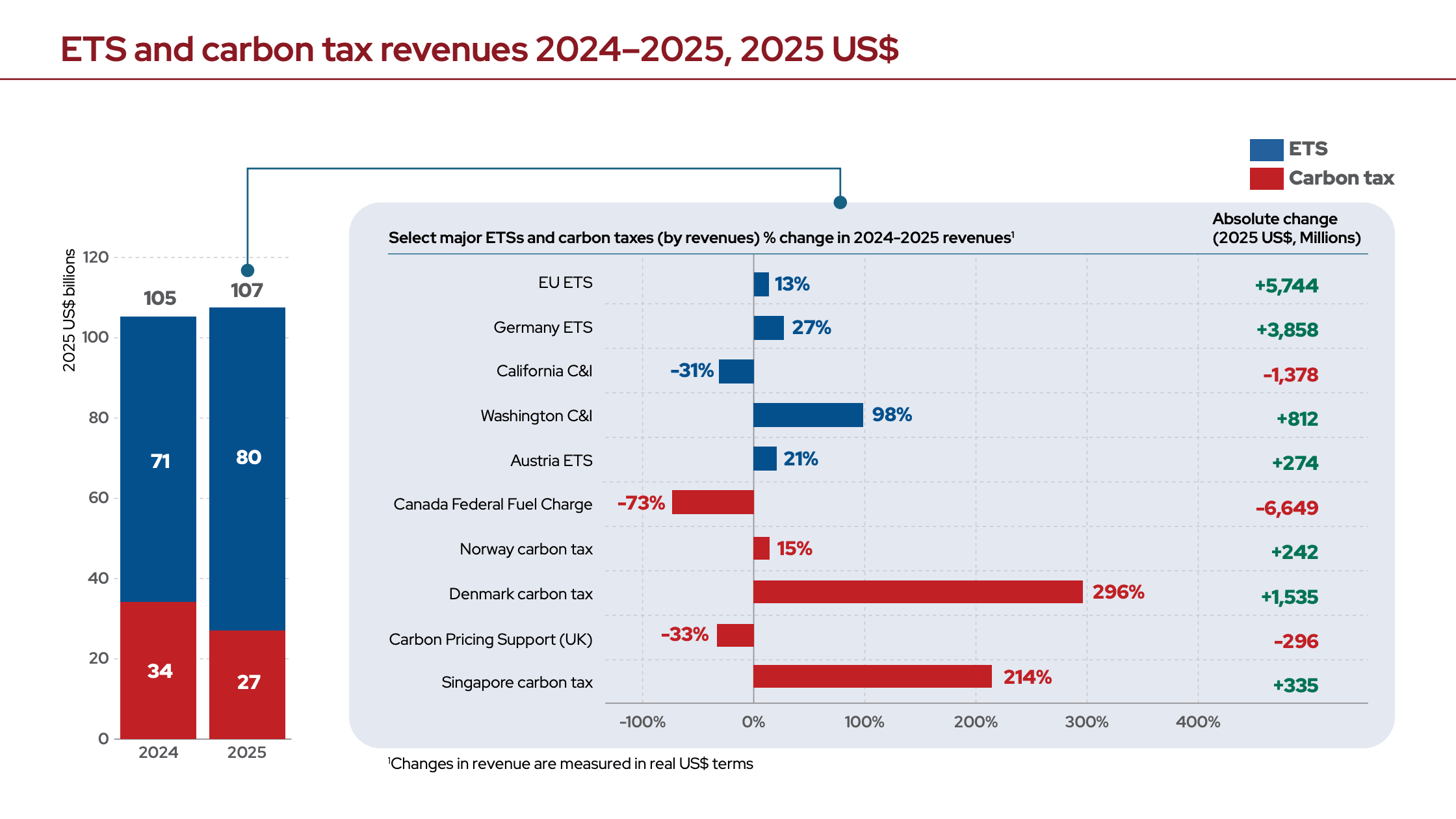

The fiscal scale of these policies is laid bare in the revenue chart below, showcasing total global revenues climbing to one hundred and seven billion dollars. The data reveals that revenue from Emissions Trading Systems has risen to eighty billion dollars, while direct carbon tax revenues have dropped slightly to twenty-seven billion dollars. On a closer look, certain regions show massive changes, such as steady revenue gains in the EU and Germany alongside sharp, triple-digit percentage jumps in Denmark and Singapore.

This multi-billion-dollar pool of money matters because much of it is being handed back to industries through green subsidies and modernisation grants. For tomato processors, the strategy is clear: while traditional, fossil-fuel plants face growing financial penalties, those who upgrade their equipment can use these very funds to help pay for high-efficiency evaporators or cleaner energy systems.

The speed at which these trends are moving from policy reports to hard enforcement is best illustrated by a landmark vote from the European Parliament’s Environment Committee. Lawmakers have decisively backed rules to strengthen the Carbon Border Adjustment Mechanism (CBAM) by targeting systemic loopholes and eliminating previous safety nets. Most notably, the committee completely deleted proposed safeguards that would have allowed imported goods to be temporarily removed from carbon taxation during sudden global price shocks. Instead, they implemented strict anti-circumvention rules,including closing online import loopholes and penalizing businesses that slightly process or split shipments to avoid compliance thresholds. They also blocked the use of international carbon credits to offset these border obligations, signaling a rigid refusal to dilute the financial impact of carbon pricing.

For the global tomato processing value chain, this tightening of borders represents a significant shift. While the mechanism is expanding its immediate scope to a long list of downstream industrial goods like steel and aluminum, the structural blueprint being built by European lawmakers directly threatens agricultural cushions. Crucially, to protect EU farmers and food processors hit by rising operational costs, the committee voted to advance a Temporary Decarbonisation Fund (TDF) starting in 2027. This fund specifically opens up financial support to strategic food security inputs like fertilizers—including urea and ammonium nitrate—as well as all downstream operators who use carbon-covered goods in their production. As Europe aggressively shields its internal agribusiness framework while systematically blocking evasion tactics from foreign exporters, waiting to optimize factory footprint is no longer a viable commercial strategy. The regulatory wall at the border is rapidly hardening, making immediate thermal efficiency and supply chain transparency an urgent priority for any global processor wishing to maintain competitive access to premium markets.

Sources: The World Bank Group Report, European Commission

{kind=link}