News

Outlook 2019–2030: From Organic Expansion to Strategic Consolidation

The following is an analysis of Euromonitor data for the global processed tomato market, covering market values from 2019 to 2030. This report highlights the shifting dynamics between mature and emerging markets, distinguishing between historical performance and future projections.

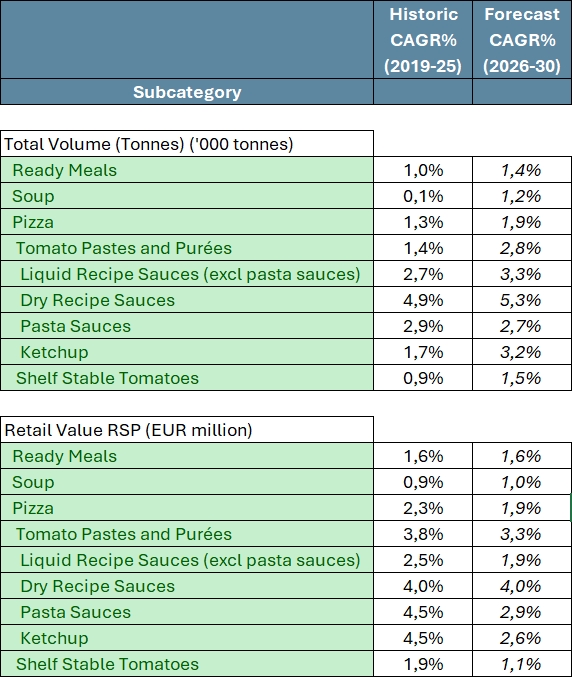

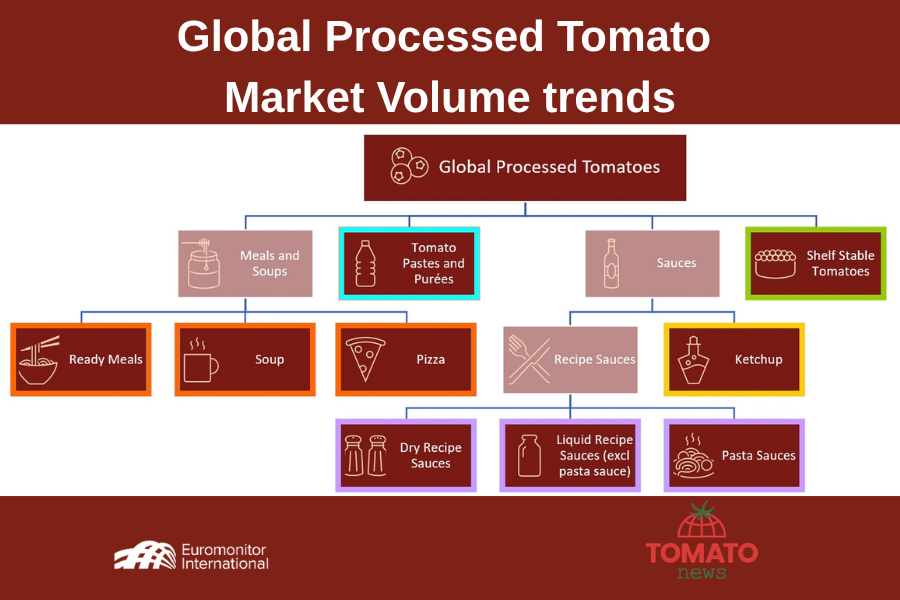

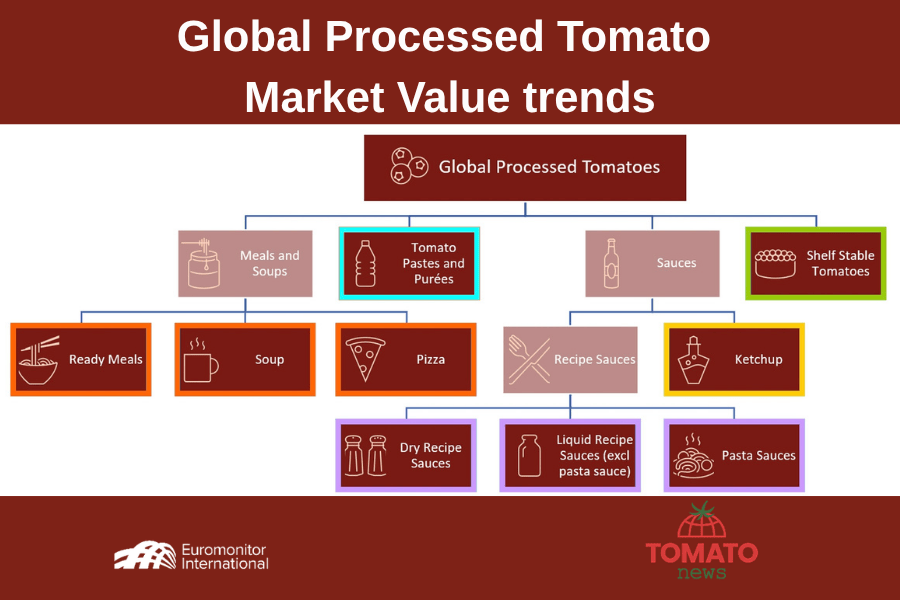

Euromonitor’s analysis scheme of the global tomato products market is structured around four main product categories: Meals and Soups, Tomato Paste and Purées, Sauces and Shelf Stable Tomatoes.

The Meals and Soups group is composed of several distinct categories, beginning with Ready Meals, which offer a high degree of convenience across shelf-stable, chilled, and frozen formats. These products are typically complete, ready-to-heat or ready-to-eat options and can include “meal centers” within the shelf-stable segment. Similarly, the Soup category encompasses all pre-packaged varieties, such as dried, chilled, and frozen formats, though it strictly excludes liquid stocks, broth cubes, and traditional Asian herbal soup mixes. Finally, the Pizza category covers all retail-packaged chilled and frozen pizzas designed for heating, specifically excluding those made on-site.

Tomato Pastes and Purees are defined as both simple tomato-based concentrates, typically containing only tomatoes, water, and salt or citric acid without additional seasonings. The main difference lies in their consistency: tomato paste is cooked for hours and reduced into a thick, rich concentrate, while tomato puree is cooked briefly to create a thick liquid.

The term Sauces brings together, alongside Ketchup, three distinct types of products: Liquid Sauces are liquid or paste-based “convenience sauces” (such as marinades, liquid gravies, or masala mixes) used during the cooking process. While they include liquid hot pot sauces, they specifically exclude dry versions and non-recipe-specific table sauces like ketchup, mayo, or soy sauce. Dry Sauces consist of powdered recipe mixes that require the addition of water or milk. This category includes powder marinades and spice mixes named after specific dishes (e.g., fajita or bolognese), but excludes any powdered product not linked to a specific recipe. Finally, Pasta Sauces are pre-packaged sauces (shelf-stable, chilled, or frozen) designed to be added directly to pasta or heated with fresh ingredients. Common varieties include pesto and carbonara; however, dehydrated versions requiring liquid are classified as dry sauces.

Shelf Stable Tomatoes consist of ambient/shelf stable typically sold in tins, glass jars, aluminum/retort tomatoes packaging or brick liquid cartons such as Tetra Recart or Combisafe. This includes sun-dried tomatoes as well as products with added seasoning (e.g. with chilli, garlic or herbs).

The analysis of Euromonitor data for the processed tomatoes market reveals contrasting dynamics between 2019 and 2030, marking a clear transition from a phase of organic growth to a period of projected consolidation. These figures dissect historical trends and future forecasts based on Compound Annual Growth Rates (CAGR) for Total Volumes (expressed in thousands of tons) and Retail Value (RSP) expressed in millions of Euros.

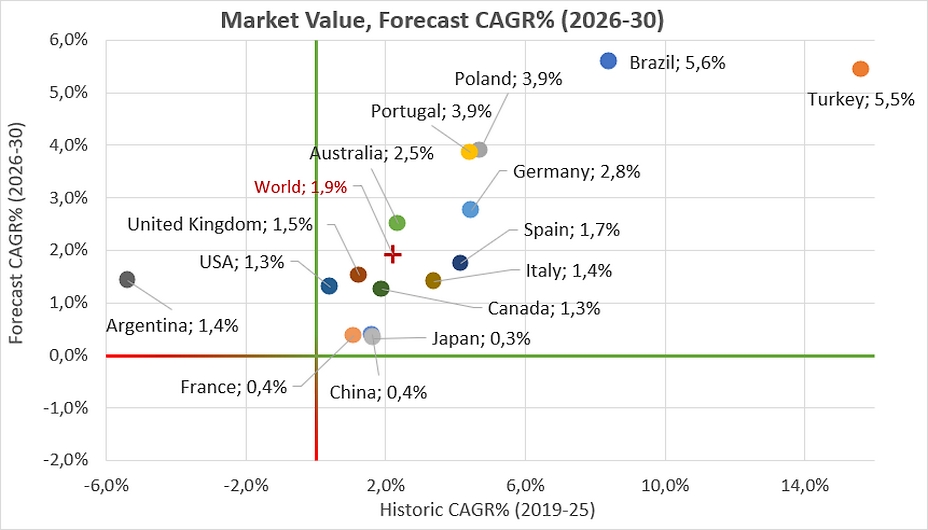

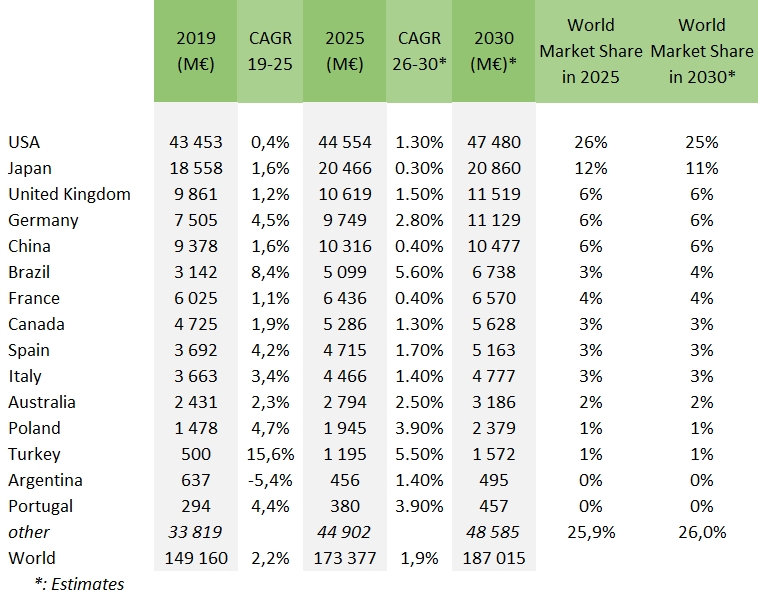

Between 2019 and 2025, the global market was characterized by a sharp duality: slow organic growth in developed nations versus rapid expansion in specific emerging economies. Turkey emerged as the most spectacular growth engine in the panel, posting an exceptional CAGR of 14.2%, however, it must be emphasized that the growth in value recorded in Türkiye is largely due to high levels of inflation. This momentum allowed the Turkish market to more than double its value, rising from 500 million Euros in 2019 to over 1.2 billion Euros by 2026. Brazil followed a similar trajectory with robust annual growth of 8.1%, confirming the increasing appetite for processed products in South American markets.

In Europe, more nuanced dynamics appeared. Poland (+4.7%) and Germany (+4.2%) showed dynamism above the regional average, contrasting with the slow growth of historical “heavyweights” such as the United Kingdom.

Conversely, this period saw a severe erosion of the Argentine market, which declined at a rate of -4.3% per year—likely due to inflation and deteriorating exchange rates—while global leaders such as the United States, France, Japan, and China remained stalled at approximately 1.1% annual growth. Technical observations suggest market saturation in these regions, where value growth is primarily driven by inflation and unit price increases rather than a massive rise in actual consumption.

Shifting to the 2026–2030 forecast, the data indicates a global paradigm shift defined by a widespread slowdown in growth rates. Turkey’s market development is expected to decelerate drastically to 5.5%, a level almost identical to Brazil’s (5.6%). While these rates remain among the highest in the group, they mark a natural readjustment following the rapid expansion of the previous decade.

According to Euromonitor figures, large Asian markets, China and Japan, will enter a phase of near-total stagnation with marginal growth of 0.4% and 0.3%, respectively. Western Europe is expected to follow a similar consolidation trend, with projected rates for Germany, France, Italy, and Spain all falling below their historical performance. The dynamics in Latin America are marked by a striking contrast between Brazil and Argentina. Brazil remains the region’s engine, where expected growth (5.6%) is set to be driven by product diversification, premiumization, and the influence of social media. Conversely, Argentina is grappling with high inflation, forcing consumers to prioritize more affordable solutions such as home cooking and the use of tomato paste over ready meals. Following a price surge between 2022 and 2023, exacerbated by local currency depreciation and rising raw material costs, the market has stabilized. Euromonitor highlights a trend toward gradual price increases in 2026; Brazil is responding by leveraging innovation to add value to its products, while Argentine consumer choices remain dictated by purchasing power, suggesting a modest recovery with positive growth of 1.4%.

Meanwhile, the USA market—which remains the largest in the world by absolute value—is expected to see a slight acceleration in growth to 1.3%, reaching a historic peak of 47.48 billion Euros by 2030.

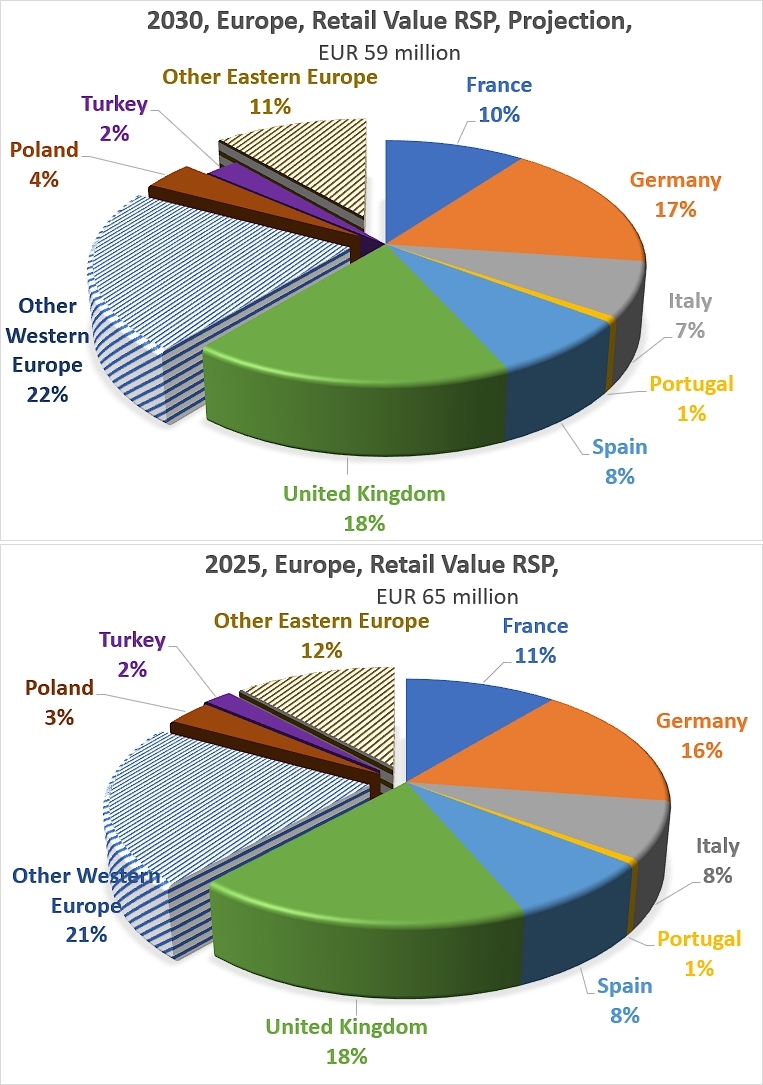

An analysis of the competitive structure in extended Europe (including the UK and Turkey) for 2030 reveals a massive concentration of value in Northern consumption hubs. The United Kingdom (11.5 billion Euros) and Germany (11.1 billion Euros) will dominate the European landscape, each capturing approximately 17%% of the regional market share. France will maintain third place at 10%, ahead of Spain (8%), Italy (7%), and Poland (4%).

This hierarchy highlights a persistent industrial paradox: although Italy and Spain are major global centers for production and processing, the monetary value captured at the retail level remains concentrated in net-importing countries. Technical observations suggest this is accentuated by the power of organized retail and strong “premium” national branding in these Northern consumer markets.

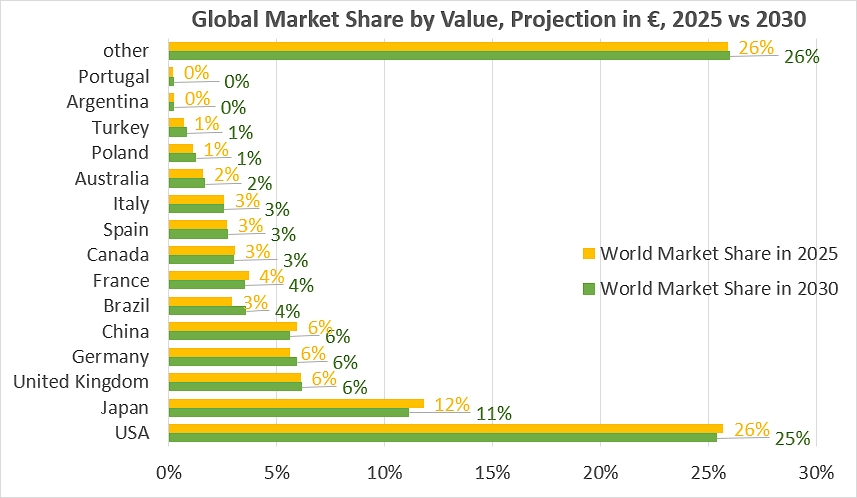

The 2030 projections highlight several critical insights into the future of the global processed tomato market. Most notably, American hegemony remains undisputed; the USA continue to be the dominant force, capturing nearly 38% of the total value among these 15 key markets (25% of the world as a whole). Its large population and extensive distribution network ensure this country a market share more than twice that of their main competitor.

Within the mature tier, Japan maintains a significant 16.6% share. This reflects its status as a highly valuable, albeit slow-growing, market through the late 2020s. In Europe, the leadership is shared between the United Kingdom and Germany. With almost identical weights of approximately 6% each, these two nations represent the primary core of European consumption value.

A clear distinction remains between emerging and mature economies. While countries such as Turkey and Brazil have posted the most impressive growth rates, their overall weight in global retail value is still relatively small compared to the established “heavyweights.” Nevertheless, their role as future growth drivers is critical as mature markets reach a point of saturation. Ultimately, this distribution confirms that while the “engine” of growth is shifting toward the East and South, the “vault” of retail value remains firmly anchored in the West and Japan.

In summary, Euromonitor’s data paints a picture of a rapidly changing global processed tomato market. The 2020s are marked by a paradigm shift in growth drivers: the boom seen in Turkey and Brazil is expected to give way to a phase of normalization. Mature markets in North America and Western Europe are expected to enter an era of consolidation and value-driven growth (upmarket positioning) rather than volume-driven growth, while Asia could experience prolonged stagnation. By 2030, the market structure will remain dominated by US hegemony and, in Europe, by a German-British consumer duopoly, which will capture the most part of regional value.

Some complementary data

2030 Values and Relative Global Weight: this table summarizes the final projections for 2030, calculating each country’s share relative to the total studied group (125.7 billion Euros).

Source: Euromonitor

{kind=link}