News

Brazil: Tomato Products Trade (2024–Nov 2025)

Brazil’s trade balance for tomato products shows a chronic deficit, largely driven by imports of tomato paste and canned tomatoes; Italy and Chile are the main beneficiaries of the current situation.

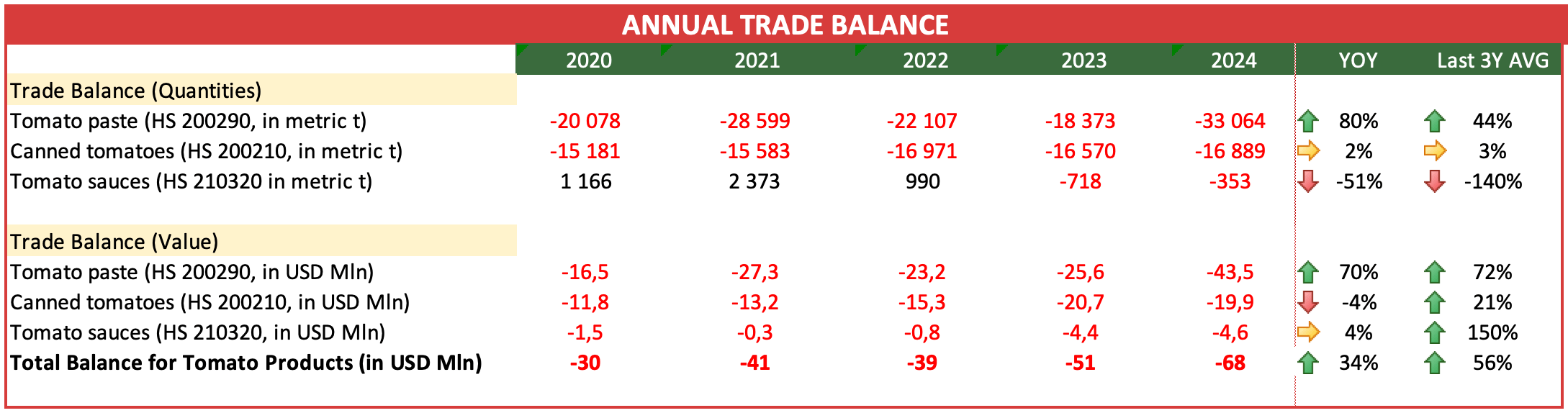

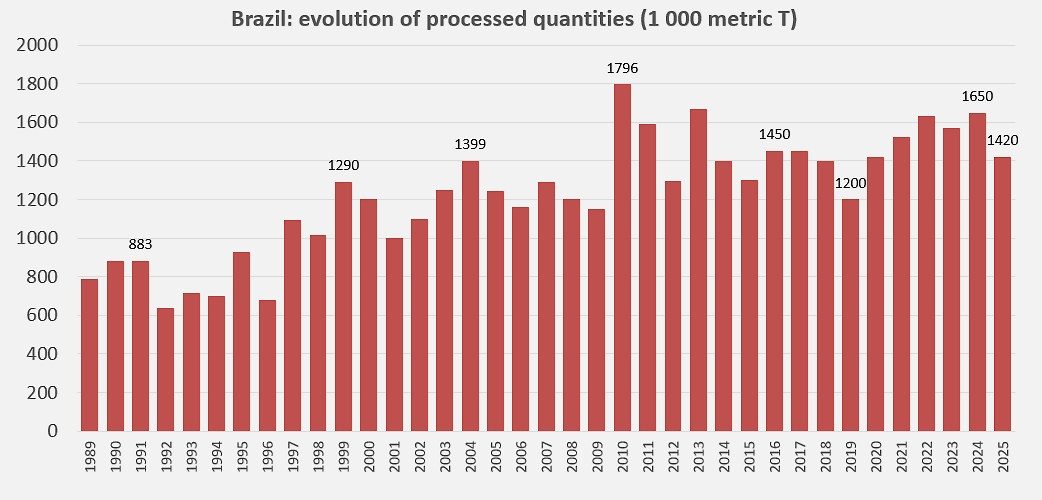

Despite a domestic sector capable of processing over 1.5 million tons of fresh tomatoes on average over the last five years, thus positioning it globally between Iran and Portugal, Brazil is unable to fully meet domestic demand. Significant imports of tomato paste, canned tomatoes, and, to a lesser extent, sauces and ketchup, supplement domestic production of industrial tomato products: in 2024, Brazil’s trade balance for tomato paste (HS code 200290) showed a deficit of 33,000 metric tons, an increase of 44% compared to the average of the three preceding years. In the first eleven months of 2025, the deficit reached 32,700 tons, 4% higher than in the January-November period of 2024.

The situation regarding canned tomatoes supplies (HS codes 200210) is less critical: for this sector, the Brazilian trade deficit shows only a 3% increase in volume in 2024, with external purchases fluctuating between 16,000 and 17,000 tons over the last three years. A comparison of activities for the periods January-November 2024 and 2025 reveals a slight improvement (-4%) in the balance of trade for canned tomatoes, which decreased from 15,600 tons in 2024 to 15,000 tons in 2025.

The sauces and ketchup sector (HS code 210320) has, in recent years, gone from a very slight surplus to a deficit; the quantities involved do not exceed a few hundred tons, and the first eleven months of 2025 reversed this trend, with a surplus of nearly 1,000 tons, whereas the deficit for the same period in 2024 was 300 tons.

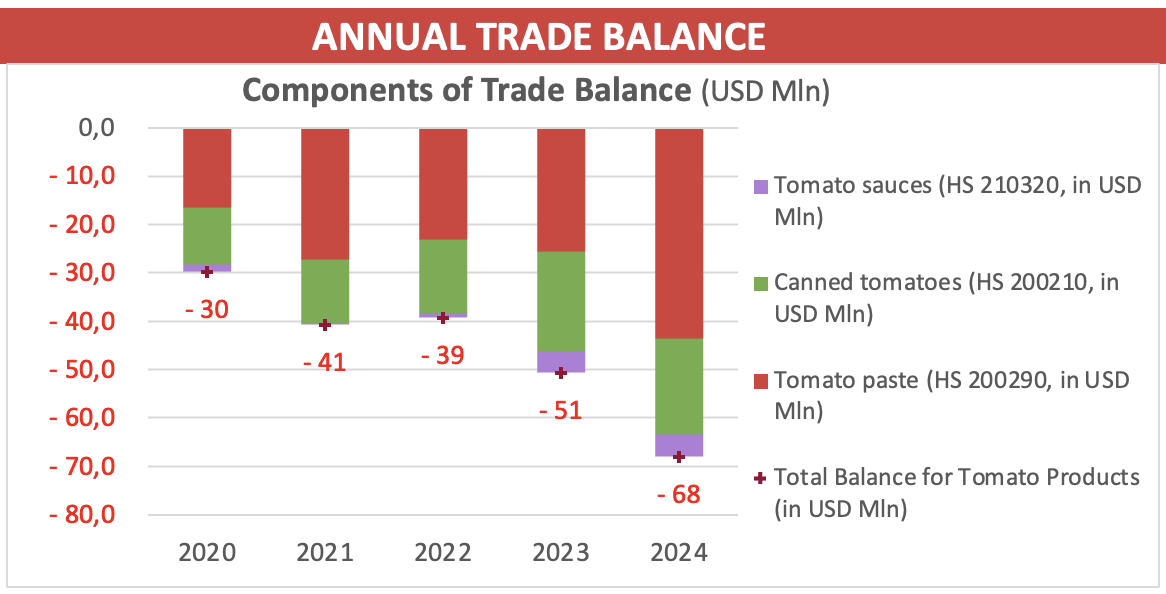

Brazil’s partial dependence on imports results in a persistent trade deficit. In 2024, the net trade deficit reached approximately USD 68 million, up 34% compared to 2023 and 56% compared to the annual average (USD 44 million) for the period 2021-2023. However, it should be noted that the first eleven months of 2025 significantly reversed this trend, reducing the deficit by approximately 16%, from nearly USD 65 million for the period January-November 2024 to just USD 54 million for January-November 2025.

Over the last three years (2022 to 2024), the majority (58%) of the Brazilian trade deficit was related to external purchases of tomato paste; imports of canned tomatoes and sauces and ketchup accounted for a large third (35%) and 6% of the total deficit, respectively.

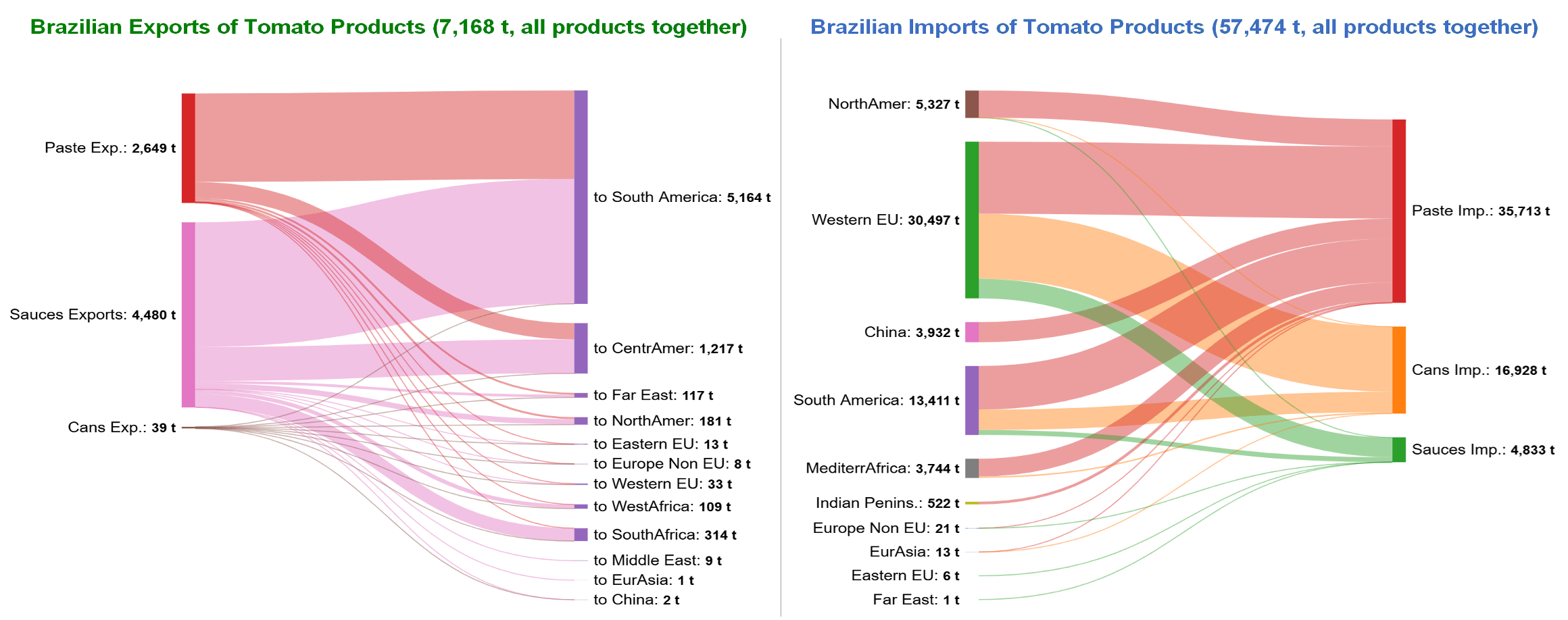

Processing countries in Western Europe and South America are the main beneficiaries of the current situation. Whether it’s tomato paste, canned tomatoes, or sauces, Italy almost single-handedly handles all European exports to Brazil. Tomato pastes from the United States, Chile, and, to a lesser extent, Peru, Argentina, Egypt, and China, supplements supply to the Brazilian market.

Brazilian demand for canned tomatoes is primarily met by the Italian sector; Argentinian products are also very prevalent on the Brazilian market.

In the sauce sector, Italy is by far Brazil’s leading supplier, followed by Chile.

In total, of the $68 million deficit projected for 2024 in Brazil’s tomato products trade balance, $40 million went to Italian operators. $11 million USD to Chilean operators, $5.5 million USD to the United States, $5.4 million USD to China, and $4.7 million USD to Egypt.

Some complementary data

Evolution of quantities processed by the Brazilian sector since 1989.

You can consult the country profile for Brazil here.

Sources: TDM, WPTC

{kind=link}