News

The results of the last few years show that global consumption was boosted by an increase in demand during the Covid pandemic, but then slowed by a reduction in the quantities of processed products due to the vagaries of the weather.

Background

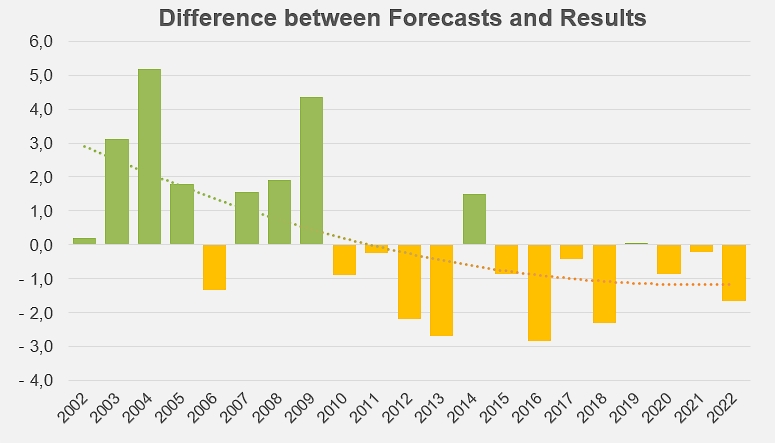

Over the past fifteen years, the global industry initially sought to compensate for the disastrous effects of the over-abundant 2009 campaign, then struggled to raise the level of processing activity to meet global demand. Of the fourteen seasons between 2009 and 2022, eleven ended with results well below initial processing targets. The accumulation of these production shortfalls, combined with the spectacular rise in demand during the Covid pandemic between 2020 and 2022, largely explains the surge in world prices for tomato products in recent years.

Climatic hazards, health crises, political tensions, environmental pressure, social expectations, inflationary pressures and the growing reluctance of growers to commit themselves to this risky crop, have for several years maintained a dynamic of underproduction that has confronted the processing sector on several occasions with a near-total disappearance of stocks at the end of the marketing year. Paradoxically, against a backdrop of growing demand, consumption has been physically limited by the insufficient quantities of products available in the retail and food-service distribution channels.

Global trade

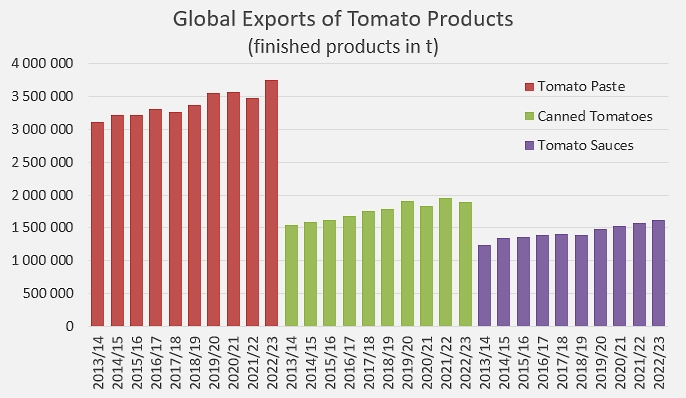

Despite this, thanks to the extensive use of available quantities of finished products, quantities exported by the major processing countries reached record levels in 2022/2023, particularly in the categories of tomato pastes (HS codes 200290) and tomato sauces & ketchup (HS codes 210320).

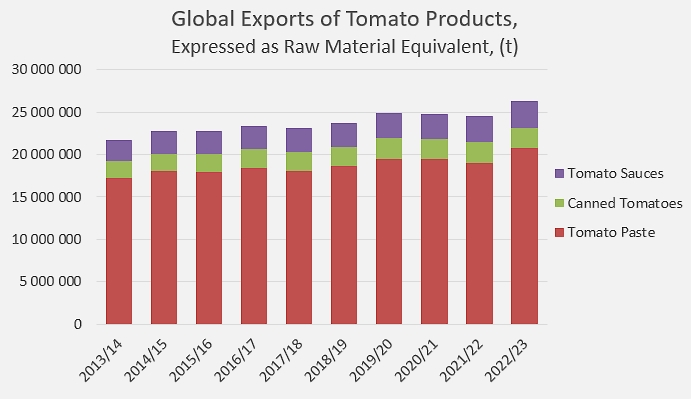

Volume of processed quantities absorbed annually by worldwide export operations, expressed in raw material equivalent.

Last year, nearly 3.746 million metric tonnes (t) of pastes (finished products) were exported worldwide, 6% more than the average for the previous three years. Similarly, 1.625 million t of sauces & ketchup were exported, 6.6% more than over the 2019/2020 – 2021/2022 period. With a fluctuating volume of 1.898 million t in 2022/2023, foreign sales of canned tomatoes remained particularly stable, only 530 t (-0.03%) below the average of the previous three years.

Exports of tomato products, by category.

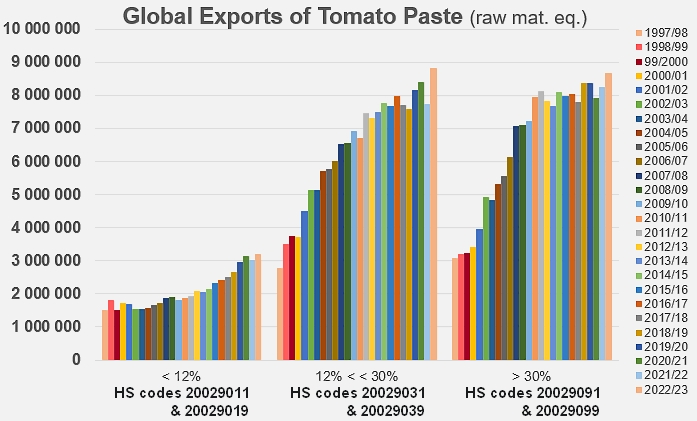

Tomato paste exports, by segment.

Ultimately, the quantities of raw materials absorbed by exports of finished products in 2022/2023 can be estimated at around 26.3 million t of fresh tomatoes, a figure that represents more than 68% of the quantities processed during the 2022 campaign (38.45 million t), whereas world trade only absorbed an average of just over 64% of the products available over the three previous marketing years, which were nevertheless marked by a sharp rise in demand in the context of the pandemic.

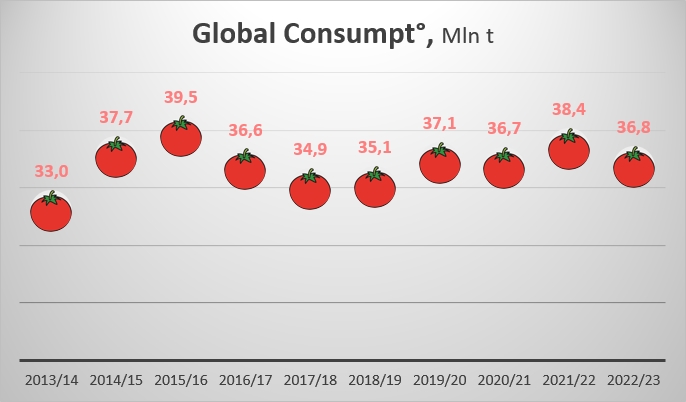

Overall consumption in 2022/2023

The results of this 15th edition of the consumption survey confirm the dynamics commented on in our previous editions, in particular during the 14th (virtual) Congress organized in 2022 by the Argentinean industry.

After the sharp slowdown observed between 2016/2017 and 2018/2019, the momentum of global consumption was boosted by an acceleration in sales of tomato products in retail distribution channels, as opposed to the foodservice sector, in the context of the measures imposed in many countries during the Covid pandemic. This rebalancing between the different marketing channels is clearly documented by a recent study of the global market for tomato products (or food items containing tomato products) carried out by Euromonitor, presented at the Tomato News Conference in Parma in October 2023 and in the following pages.

The results of this 15th edition of the consumption survey confirm the dynamics commented on in our previous editions, in particular during the 14th (virtual) Congress organized in 2022 by the Argentinean industry.

After the sharp slowdown observed between 2016/2017 and 2018/2019, the momentum of global consumption was boosted by an acceleration in sales of tomato products in retail distribution channels, as opposed to the foodservice sector, in the context of the measures imposed in many countries during the Covid pandemic. This rebalancing between the different marketing channels is clearly documented by a recent study of the global market for tomato products (or food items containing tomato products) carried out by Euromonitor, presented at the Tomato News Conference in Parma in October 2023 and in the following pages.

The acceleration in sales and the rise in demand, however, came up against against the obstacle of increasingly reduced product availability during the 2019/2020 – 2022/2023 marketing years, which ended with a drastic reduction in available inventory. Processing and trading data suggest that consumption levels were between 36.5 and 38.5 million tonnes (raw material equivalent). For the last year under review, the results show a further decline, bringing overall consumption below the 37 million t threshold. The cause of what may appear to be a readjustment after several years marked by the "Covid effect" is probably to be found more in the quantities available than in any change in purchasing behavior. In fact, Euromonitor estimates that annual volume growth (for all quantities involving tomato products) reached around 2% between 2021 and 2022, and should continue at a similar pace over the next few years.

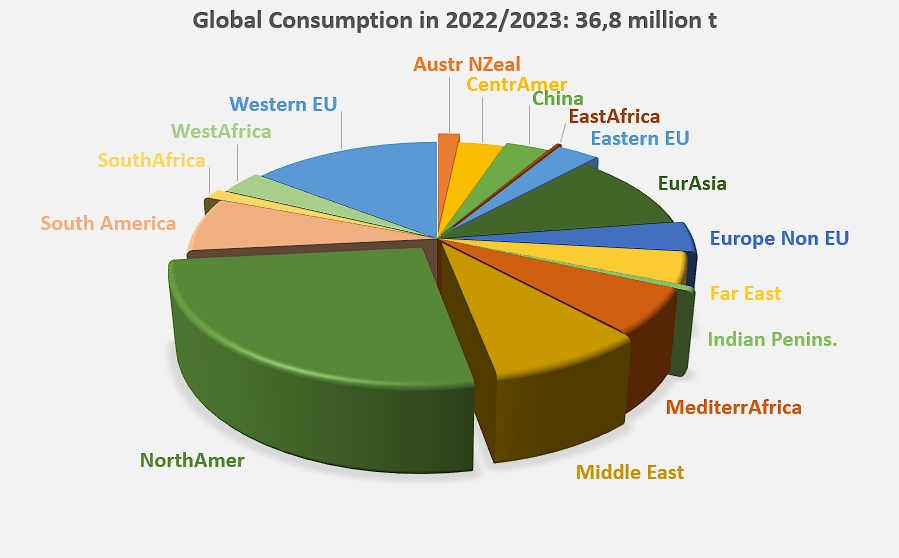

Consumer hubs

Although slightly down (-1%) on the average for the previous three years, North America (USA, Canada, Puerto Rico, etc.) remains the undisputed world leader, consuming more than a quarter of the annual volume of tomato products. The 27 member countries of the European Union accounted for around 18% of the world total, rising to 22% when the non-EU European component (UK, Switzerland, Norway, etc.) is included, also down on previous years.

The third group, comprising the countries of Eurasia (Turkey, Russia, Afghanistan, Ukraine, etc.), accounts for around 11% of global consumption. Volumes consumed in this region were slightly up on the average for the previous three years.

Although slightly down (-1%) on the average for the previous three years, North America (USA, Canada, Puerto Rico, etc.) remains the undisputed world leader, consuming more than a quarter of the annual volume of tomato products. The 27 member countries of the European Union accounted for around 18% of the world total, rising to 22% when the non-EU European component (UK, Switzerland, Norway, etc.) is included, also down on previous years.

The third group, comprising the countries of Eurasia (Turkey, Russia, Afghanistan, Ukraine, etc.), accounts for around 11% of global consumption. Volumes consumed in this region were slightly up on the average for the previous three years.

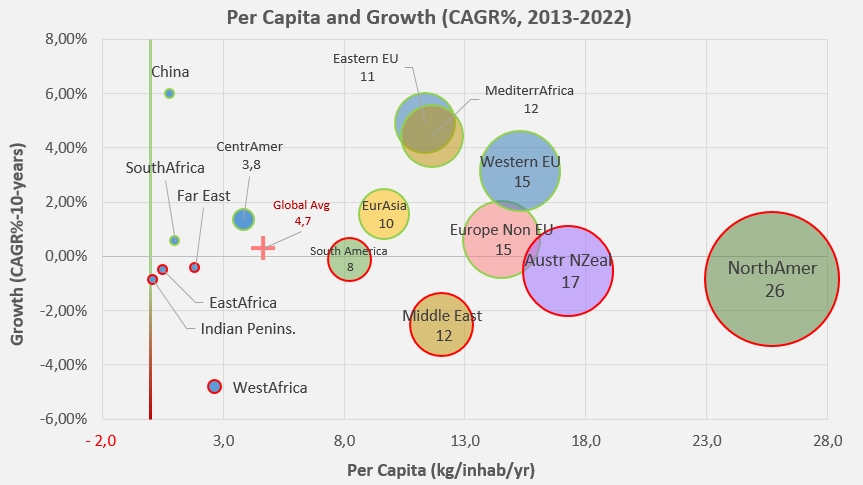

Relative importance of different markets and average annual growth rates (CAGR %) over the 2013/2014 – 2022/2023 period.

Conversely, the quantities absorbed by the Middle East (Iran, Iraq, Saudi Arabia, Israel, etc.) recorded sales that were down 4% on the previous three years. By 2022/2023, they represented around 9% of global consumption volumes.

With the quantities consumed last year, South America (Brazil, Argentina, Chile, etc.) recorded a significant increase over the previous three years. In 2022/2023, the five main regions alone accounted for more than two-thirds of total consumption of tomato products.

With the quantities consumed last year, South America (Brazil, Argentina, Chile, etc.) recorded a significant increase over the previous three years. In 2022/2023, the five main regions alone accounted for more than two-thirds of total consumption of tomato products.

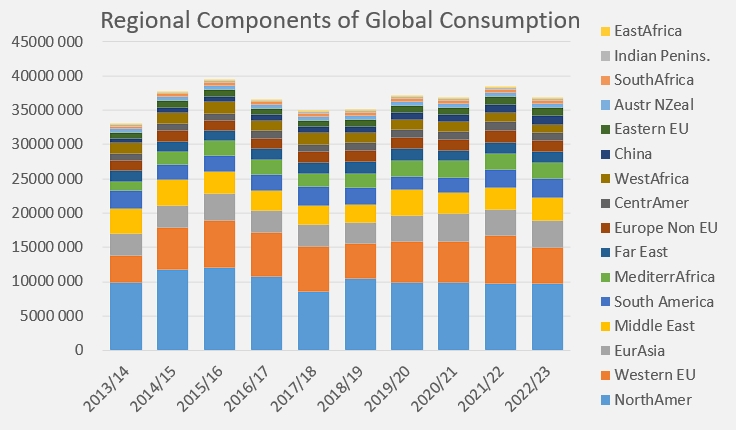

Trends in regional components of overall consumption of tomato products.

On a global scale, available data indicates a slight decline in consumption for the year 2022/2023, of around 1.7% compared to the average for the previous three years. On a broader level, the general trend seems to be heading towards an increase in the relative "weight" of emerging regions (South America, Mediterranean Africa, the Far East, Central America, etc.) over the past ten years, at the expense of the historically more significant consumer regions.

Individual consumption

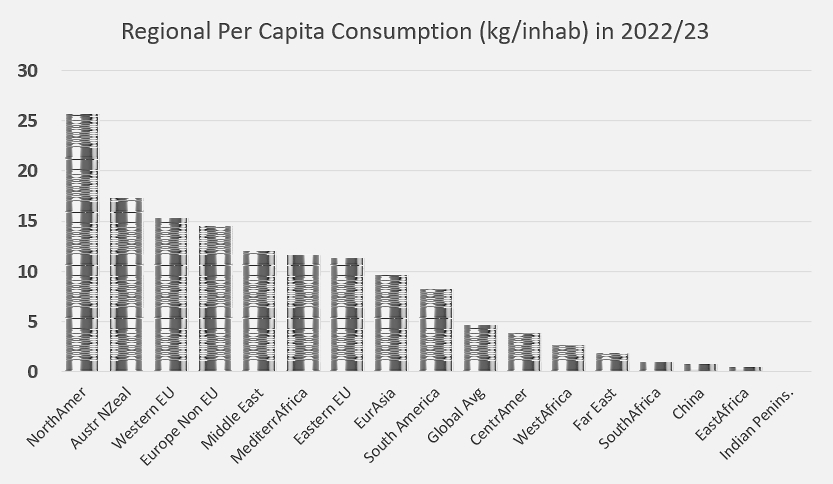

The North American region, number one in terms of volume, is also number one in terms of individual consumption, which has been recorded at just under the raw tomato equivalent of 26kg per capita per year.

The 2022/2023 hierarchy of countries in terms of individual consumption is in line with our previous consumption studies, with the Australia-New Zealand region in second place (17kg/person/year), ahead of the Western European Union (15kg) and non-EU Europe (14.5kg). The Middle East, Mediterranean Africa and the Eastern EU rank next, with levels close to 12kg/person/year. The individual global average remains below 5kg/year, with Central America, West Africa and the Far East below this with levels of between 2 and 4kg per person per year, and a few regions with very low and difficult-to-specify levels below the 1kg per person threshold.

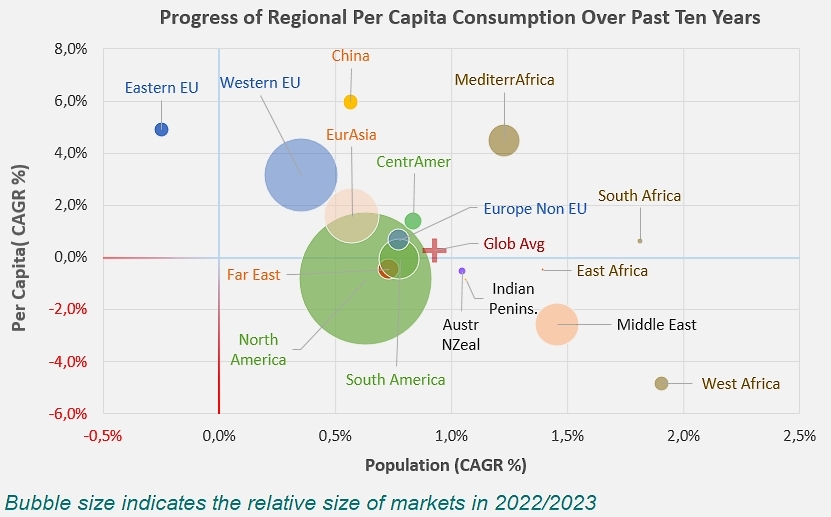

Available data shows that global consumption growth over the last ten years has been relatively low: the first of its two components, the demographic one, has recorded an average annual growth rate (CAGR) of close to 1%; the second, defined by individual consumption, is around 0.3%, so that between 2013/2014 and 2022/2023, global consumption should have increased by 1.2% per year.

This pace, which reflects neither the intensity of demand nor variations induced by consumer behavior or the vagaries of agro-industrial activity, is the result of highly contrasting regional dynamics. Thus, two markets comparable in size in 2022/2023, the Eastern EU and West Africa, are driven, in the first instance, by an acceleration in individual consumption (CAGR +4.9%) within a slightly declining population (-0.25%), while the other is driven by a significant increase in population (CAGR +1.9%) in a context of sharply declining individual consumption of tomato-based products (-4.8%).

Similarly, some regions are benefiting from positive developments both in terms of demographics and individual consumption: this is the case in China, Eurasia, Mediterranean Africa, the Western European Union, etc.

The combination of slow population growth (+0.6%) and a decline, albeit slight, in individual consumption (-0.8%) over the past decade has resulted in a virtually stagnant North American dynamic (CAGR -0.2%). Closer to the average global profile, moderate consumption growth in non-EU Europe (CAGR 1.4%) over the period 2013/2014 – 2022/2023 is based on slow population growth (0.8%) and measured individual consumption growth (+0.6%).

The combination of slow population growth (+0.6%) and a decline, albeit slight, in individual consumption (-0.8%) over the past decade has resulted in a virtually stagnant North American dynamic (CAGR -0.2%). Closer to the average global profile, moderate consumption growth in non-EU Europe (CAGR 1.4%) over the period 2013/2014 – 2022/2023 is based on slow population growth (0.8%) and measured individual consumption growth (+0.6%).

This article is published in the 2024 Processing Tomato Yearbook published by Tomato News and distributed free of charge to participants of the Congress organized by the Hungarian tomato processing industry, in Budapest, from June 9 to 12, 2024.

Sources: Trade Data Monitor

{kind=link}