News

Trade in 2015: the main market destinations

20 countries absorb 80% of the worldwide trade in tomato products; import volumes for the twentieth country are 10 times lower than those of the world's first importing country

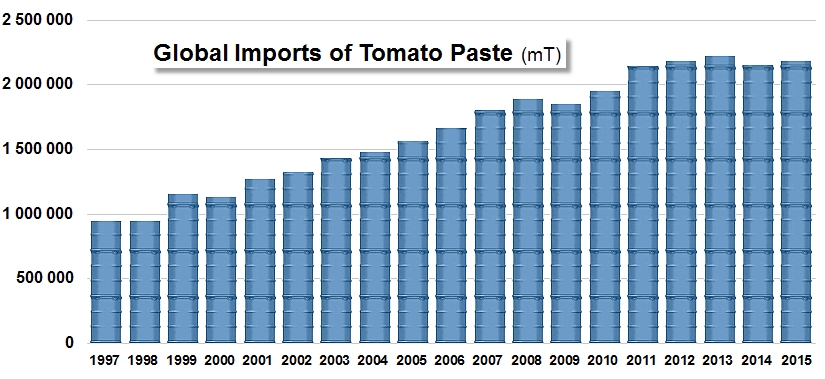

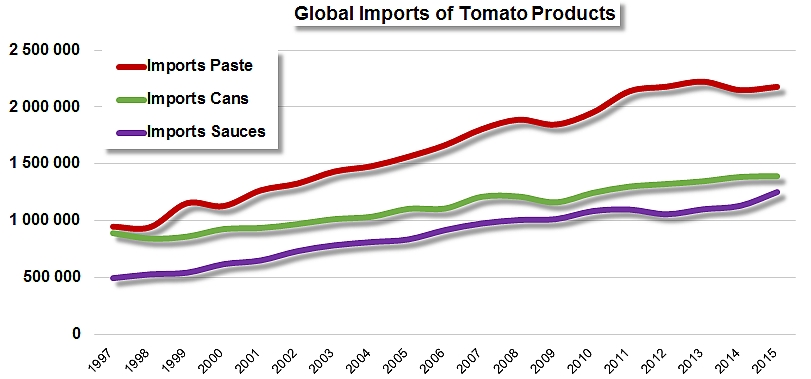

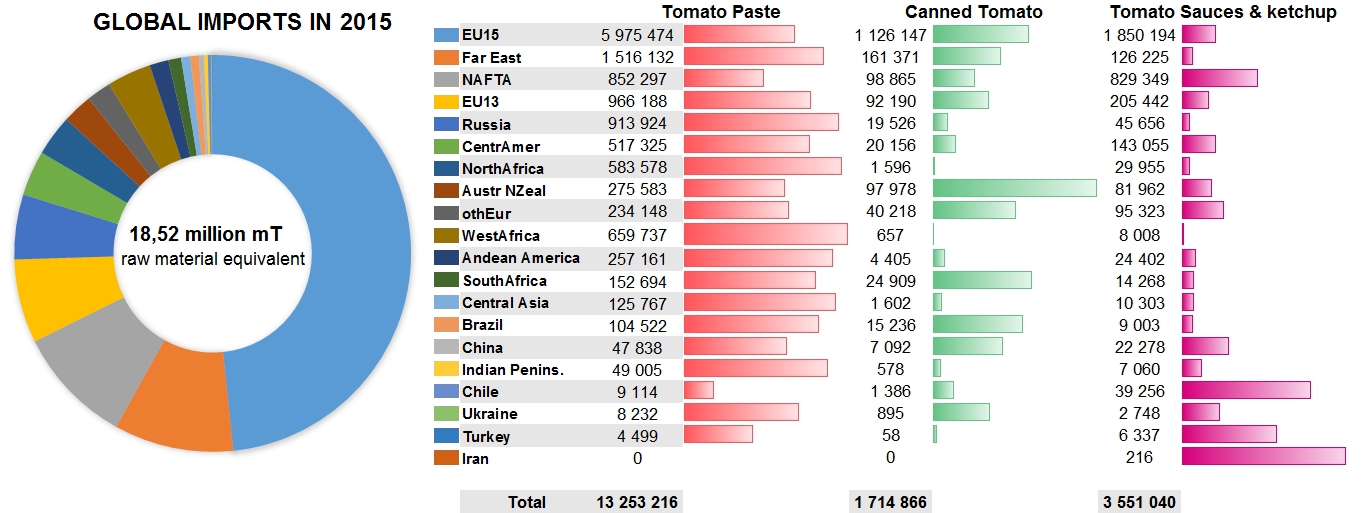

After the slight contraction recorded for the paste trade in 2014, worldwide imports of tomato paste seem to have recovered somewhat in 2015: overall, recorded import movements (which accounted, depending on the categories considered, for between 70% and 95% of the quantities of finished products that were actually traded) absorbed last year 2.18 million metric tonnes (mT) of tomato paste, 1.4 million mT of canned tomatoes (peeled, unpeeled, diced, sliced, etc.) and 1.25 million mT of sauces & ketchup. The paste category, which was the hardest hit by the slowdown in trade last year (-3.3%), rebounded by 1.3%, whereas the categories of canned tomatoes and sauces & ketchup continued their progression, slowly in the case of canned tomatoes (+0.5%) and fast in the case of ketchup & tomato sauces (+10.5%).

Ranking by country

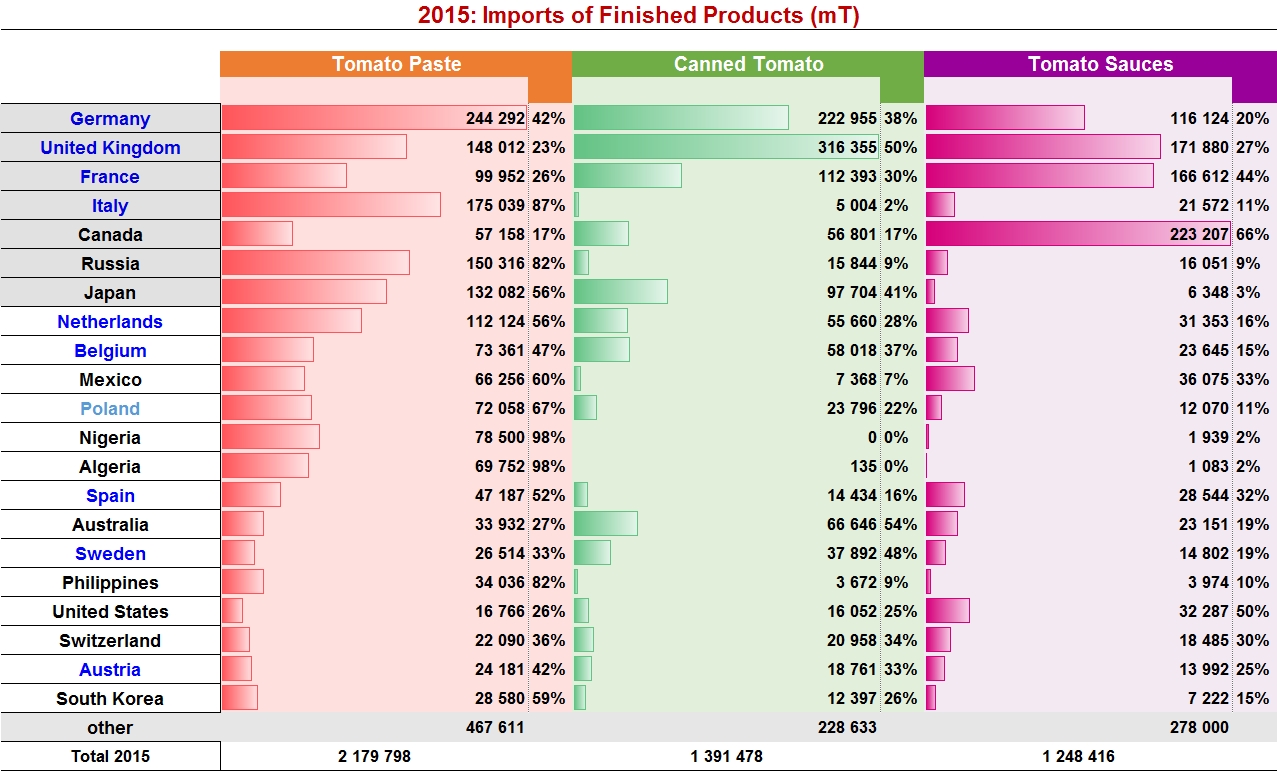

In 2015, Germany ranked in top place once again as the world's first destination for tomato product purchases. Last year, German imports absorbed the processed equivalent of 2.09 million metric tonnes of raw tomato. With these volumes increasing by 9% compared to 2014, Germany alone absorbed more than 11% of the quantities of tomatoes exchanged worldwide (expressed in farm weight equivalent). For this country, which for many years has been the main outlet of the tomato industry, paste purchases have been the biggest item of expenditure: 244 000 mT were purchased from abroad (for an amount approaching EUR 248 million), accounting for 42% of the total quantities of finished products imported into Germany in 2015. Canned tomato purchases (223 000 mT, 38% of the total quantities) cost EUR 157 million, while sauces (116 000 mT, 20% of the total) cost EUR 144 million.

The second place occupied by the United Kingdom in this worldwide ranking of importing countries is paradoxical insofar as British expenditure (GBP 419 million, or approximately EUR 578 million) was noticeably higher than the expenditure of Germany (EUR 549 million). Although British imports only absorbed last year the equivalent of 1.78 million mT of processed tomato (slightly less than 10% of the declared quantities imported worldwide), they mobilized product categories that are clearly more costly: no less than 316 000 mT of canned tomatoes were imported, accounting for 50% of total purchases and leading to expenditure estimated at EUR 269 million. The sauces & ketchup sector also weighed heavily on British expenditure, with quantities approaching 172 000 mT (27% of imports) for a total amount estimated at EUR 170 million. Paste imports (148 000 mT, 23% of total imports) cost approximately EUR 140 million.

Although France enjoys an efficient processing industry, it nonetheless ranks third worldwide among the countries that are least self-sufficient in terms of tomato products. Its level of operations remains well below what would be necessary to satisfy national demand. Last year, France's foreign purchases amounted to the equivalent of 1.22 million mT of tomato in processed forms, or approximately the same quantity as in 2014 and about 6.5% of the imports recorded worldwide. Unlike Germany or the United Kingdom, whose respective expenditure is mostly dedicated to buying pastes or canned tomato, France mostly imports tomato sauces & ketchup. In 2015, imports in this category amounted to almost 167 000 mT (44% of total French purchases), for an amount approaching EUR 185 million. Shipments of paste (100 000 tonnes, 26% of the imported total) and canned tomato (112 000 tonnes, 30% of the total) took total French expenditure to approximately EUR 375 million. (See our article in the June 2016 issue of Tomato News.)

The Italian import profile is heavily marked by the industrial and commercial outlook of the country. The shipments recorded for the canned tomato sector (5 000 mT in 2015) most likely correspond to returned goods rather than real imports, and purchases of sauces & ketchup only represented slightly more than 21 000 mT. These two category items only accounted for slightly more than EUR 25 million in terms of expenditure, out of the 180 million that Italy spent on its imports in total. The rest of 2015 expenditure was spent on paste imports, amounting to 175 000 mT of finished products, which accounted for 87% of the total quantities imported that year. A big share of this tonnage was more specifically intended for remanufacturing companies set up in the south of Italy, part of the 656 000 mT of paste exported last year by Italy. Overall, the quantities of tomato products imported by Italy in 2015 accounted for 1.13 million mT in farm weight equivalent. (See the June 2016 issue of Tomato News.)

Canada is the first non-European country in this worldwide ranking of tomato product importers, and came in fifth place last year by recording an import profile that is strongly affected by its own industrial operations. In 2015, Canadian imports accounted for 1.05 million mT in farm weight equivalent, of which a major proportion entered the country in the form of sauces & ketchup. 223 000 mT of sauces & ketchup were purchased abroad, accounting for two thirds of the volumes of finished products imported and costing the country close on USD 233 million. Imports of paste (57 000 mT) and canned tomatoes (also 57 000 mT) account for the remainder of these purchases, bringing the total Canadian expenditure to approximately USD 333 million last year. (See the May 2016 issue of Tomato News.)

Last year, Canada was also the last of five countries that imported tomato products amounting to more than 1 million tonnes in farm weight equivalent. Russia, ranking sixth worldwide, only imported the equivalent of 980 000 mT of tomatoes, mostly in the form of paste (150 000 mT, or 82% of the total volumes imported). Total Russian expenditure amounted to more than USD 160 million, of which 12 million were used for importing canned tomatoes (16 000 mT) and USD 15 million for purchases of sauces & ketchup (16 000 mT also).

| The 21 main tomato product importing countries absorbed in 2015 almost 80% of recorded quantities. Germany, which was n°1 in this worldwide ranking last year, imported the equivalent of 2.09 million tonnes of tomato in processed form – accounting for approximately 11% of worldwide imports. |

With 209 000 mT of tomatoes in farm weight equivalent, South Korea ranked 21st among the world's importers in 2015, absorbing 1.1% of the total imports for the year, which is 10 times less than Germany.With the foreign purchases of Japan (7th in the worldwide ranking with 940 000 mT of farm weight equivalent), the group made up of the seven main importing countries in the world absorbed last year half of the quantities officially recorded for import shipments.

Ranking by category

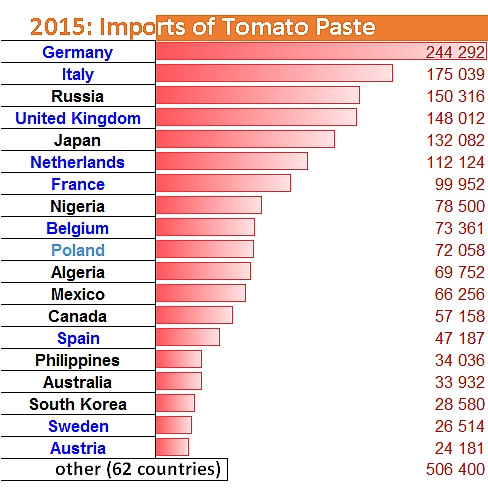

Several of the countries already mentioned among the worldwide leaders for imports logically occupy the first places among the countries that import tomato paste. So Germany, which is the world's n°1 for all categories, grabbed first place in 2015 in the sector of paste imports, ahead of Italy, Russia, the United Kingdom…

Due to measures implemented by Nigeria's newly elected government last year, the country has noticeably reduced (at least officially) its foreign purchases in order to promote national processing operations. With 78 000 mT imported, the country nonetheless ranked last year in the top group of importing countries, ahead of Belgium, Poland, Algeria, etc. In 19th place, Austria imported slightly more than 24 000 mT of finished products, which is 10 times less than Germany, and places the country last among a group of countries that absorbed 77% of the world's imports of paste. Among the countries whose customs statistics are recognized as being sufficiently reliable to be used by worldwide organizations, about 60 imported a total last year of slightly more than 506 000 tonnes of paste.

Due to measures implemented by Nigeria's newly elected government last year, the country has noticeably reduced (at least officially) its foreign purchases in order to promote national processing operations. With 78 000 mT imported, the country nonetheless ranked last year in the top group of importing countries, ahead of Belgium, Poland, Algeria, etc. In 19th place, Austria imported slightly more than 24 000 mT of finished products, which is 10 times less than Germany, and places the country last among a group of countries that absorbed 77% of the world's imports of paste. Among the countries whose customs statistics are recognized as being sufficiently reliable to be used by worldwide organizations, about 60 imported a total last year of slightly more than 506 000 tonnes of paste.

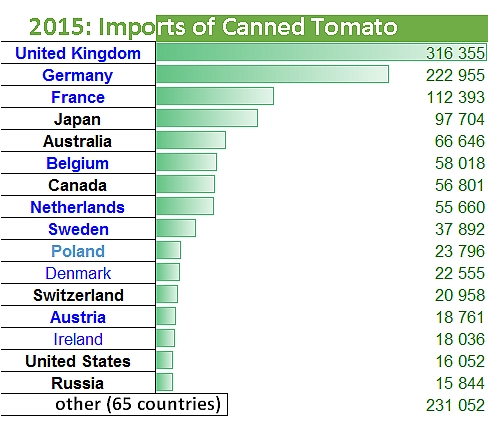

The canned tomatoes market is very polarized in terms of supply sources, but is also very concentrated in terms of outlets: last year, about 15 countries accounted for more than 83% of the import quantities recorded around the world, or 1.16 million tonnes of finished products, while the remainder of recorded quantities (230 000 mT) was shared by 65 other destinations.

The canned tomatoes market is very polarized in terms of supply sources, but is also very concentrated in terms of outlets: last year, about 15 countries accounted for more than 83% of the import quantities recorded around the world, or 1.16 million tonnes of finished products, while the remainder of recorded quantities (230 000 mT) was shared by 65 other destinations.

The canned tomatoes market is very polarized in terms of supply sources, but is also very concentrated in terms of outlets: last year, about 15 countries accounted for more than 83% of the import quantities recorded around the world, or 1.16 million tonnes of finished products, while the remainder of recorded quantities (230 000 mT) was shared by 65 other destinations.

The United Kingdom is by far the world's biggest importer of canned tomatoes. In 2015, the country on its own absorbed close on one quarter of the world's import shipments of canned tomatoes, with more than 316 000 mT of finished products, for an amount close on GBP 195 million (approximately EUR 269 million). These quantities are almost one-and-a-half times higher than those of Germany, which ranked second worldwide with an impressive total quantity of imports of 223 000 mT last year (and a cost estimated at EUR 157 million). With more than 112 000 mT of canned tomatoes imported, France ranked third among the world's importing countries for this category. French expenditure for its canned tomato supplies amounted in 2015 to more than EUR 88 million. This is slightly more than Japan spent on the 98 000 mT it imported last year. In total, this group of four countries absorbed in 2015 more than half (54%!) of the quantities shipped abroad around the world.

Australia, Belgium, Canada and the Netherlands were also among the strategic destinations for this category last year, with purchases exceeding 50 000 mT of finished products. Several other countries imported considerable quantities of canned tomatoes, like Poland (24 000 mT), Switzerland (20 000 mT), Ireland (18 000 mT). In 15th and 16th place, the United States and Russia were almost equal (approximately 16 000 mT imported for each of them), with volumes that are 20 times lower than those imported into the United Kingdom.

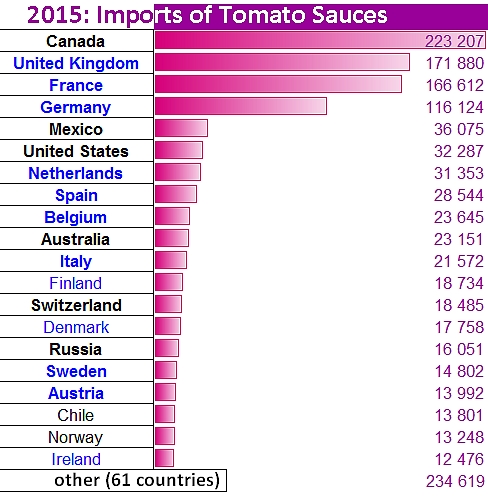

The market for sauces & ketchup was even more polarized than the canned tomatoes market. Last year, just four countries were enough to account for more than half (54%, or almost 680 000 mT of finished products) of the import shipments recorded, while imported quantities for the other 77 countries that keep records only accounted for 570 000 mT.

In first place worldwide, Canada, whose imports of sauces & ketchup amounted in 2015 to 223 000 mT of finished products (18% of worldwide import shipments), for an expenditure estimated at USD 233 million. Another big importer for this category, the United Kingdom imported last year close on 172 000 mT of sauces, absorbing 14% of the world's tonnage for an amount close on GBP 123 million (EUR 170 million). Ranking third in this list of sauce importers, France paradoxically spent more than the United Kingdom (EUR 186 million) for lower quantities (167 000 mT), accounting for 13% of the world's sauce imports in 2015. Finally, the top group of countries includes Germany, whose 116 000 mT of imports absorbed more than 9% of the world's shipments and led to expenditure of close on EUR 144 million. Most probably due to the proximity of its influential US neighbor, Mexico was an active importer of sauces. In 2015, 36 000 mT were shipped into Mexico (approximately 3% of the worlds' total volumes), for an amount estimated at USD 41 million.

In first place worldwide, Canada, whose imports of sauces & ketchup amounted in 2015 to 223 000 mT of finished products (18% of worldwide import shipments), for an expenditure estimated at USD 233 million. Another big importer for this category, the United Kingdom imported last year close on 172 000 mT of sauces, absorbing 14% of the world's tonnage for an amount close on GBP 123 million (EUR 170 million). Ranking third in this list of sauce importers, France paradoxically spent more than the United Kingdom (EUR 186 million) for lower quantities (167 000 mT), accounting for 13% of the world's sauce imports in 2015. Finally, the top group of countries includes Germany, whose 116 000 mT of imports absorbed more than 9% of the world's shipments and led to expenditure of close on EUR 144 million. Most probably due to the proximity of its influential US neighbor, Mexico was an active importer of sauces. In 2015, 36 000 mT were shipped into Mexico (approximately 3% of the worlds' total volumes), for an amount estimated at USD 41 million.

Despite operational levels that make them the world's leaders for this category, the USA, the Netherlands, Spain and a few other countries also feature in good place in this worldwide ranking of countries that are importers of sauces ketchup. However the quantities involved remain well below those of the four biggest operators for this market category, with the result that Ireland (20th worldwide importer in 2015) imported almost 18 times fewer products than the world's n°1 importer, which is Canada.

Overall, the EU stands out as the world's main importing region for tomato products. It is estimated that total imports for the 28 countries that make up the EU accounted last year for the equivalent of more than 10.2 million mT of raw tomato in processed form, or more than 55% of the import volumes recorded worldwide. Among EU countries, the presence of heavyweights like Germany, the United Kingdom and France is partly the reason for this preponderant role of the European Community on the international scene. But the EU 28 also owes this position to the high consumption levels in most of its member States, for one or the other of the product categories, whether it be the Netherlands, Belgium, Poland, Spain, Romania, etc. In the end, these countries make the region the world's main outlet for each of the three categories considered (paste, canned tomatoes, sauces).

Worldwide imports of tomato products in 2015: the regions are ranked by order of total imported volume in farm weight equivalent, broken down by category.

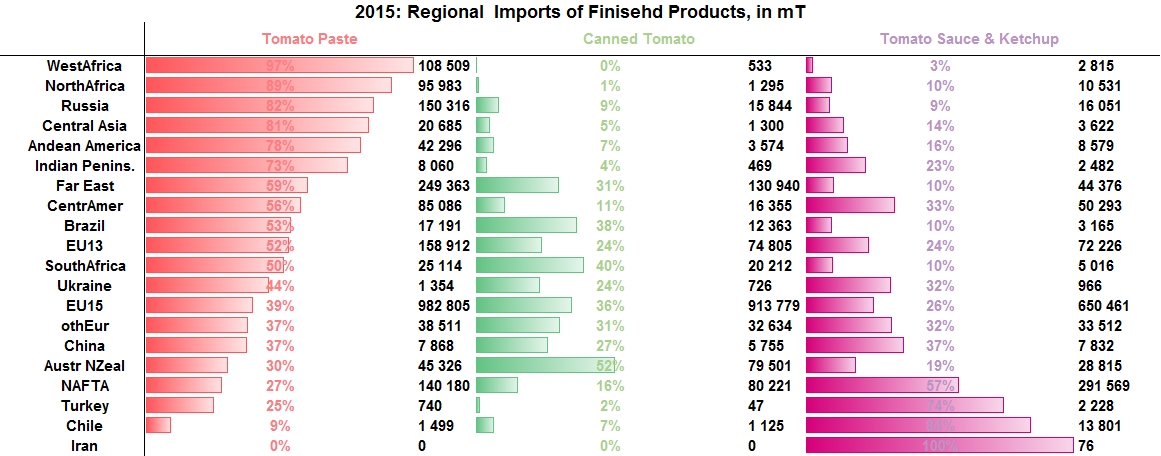

A long way behind the EU, the Far East in 2015 ranked in second place worldwide (with 1.8 million mT in farm weight equivalent), driven by the foreign purchases of countries like Japan, the Philippines and Korea, whose accumulated total accounted for almost 10% of the import volumes traded around the world (expressed in farm weight equivalent). In third place worldwide among tomato product importing regions, NAFTA accounted for volumes that are practically identical (1.78 million mT in total), ahead of Russia, whose purchases were massively focused on the paste category. Similarly, imported volumes to North Africa, West Africa, Central Asia, Andean America and the Indian peninsula almost exclusively involved tomato paste, as these regions only dedicate a tiny proportion of their expenditure to the other categories.

Other regions dedicate a larger proportion of their resources to purchasing products from the other categories, notably Australia-New Zealand and South Africa, whose imports of canned tomatoes claimed a large part of the regional total imported last year.

{kind=link}