News

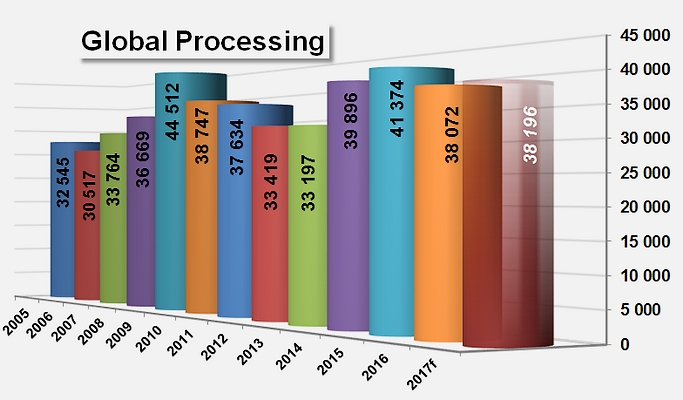

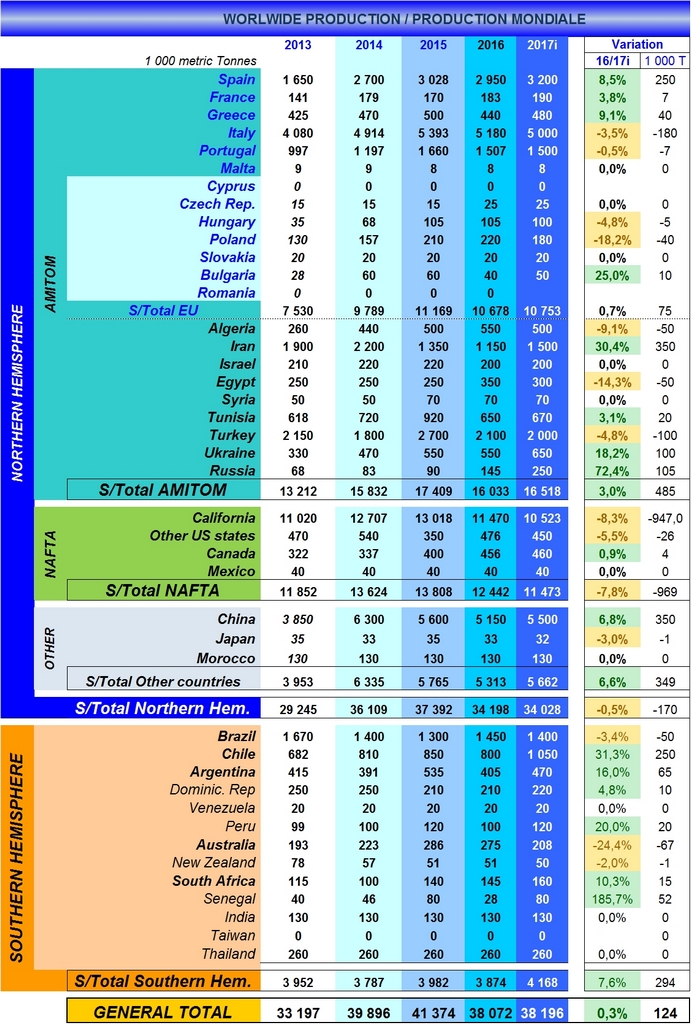

Not many changes since March, with estimates for the season at 38 million tonnes

There will be neither more nor less tomatoes processed in 2017 than in 2016. In recent weeks, processing prospects have been made more accurate and latest volume indications gathered by the WPTC on 11 April do not show any great change from previously published information. Total processed quantities should remain close on 38.2 million tonnes this year. Variations compared to previous crop updates (February and March 2017) and compared to the final results of 2016 (38.07 million mT) are tiny and really negligible compared to the negative or positive impacts that serious weather issues could have on the running of the harvest season.

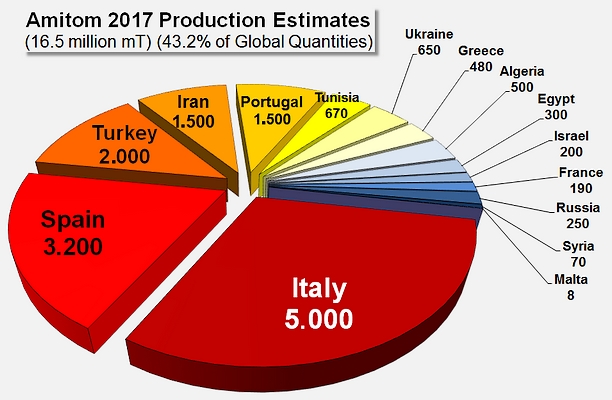

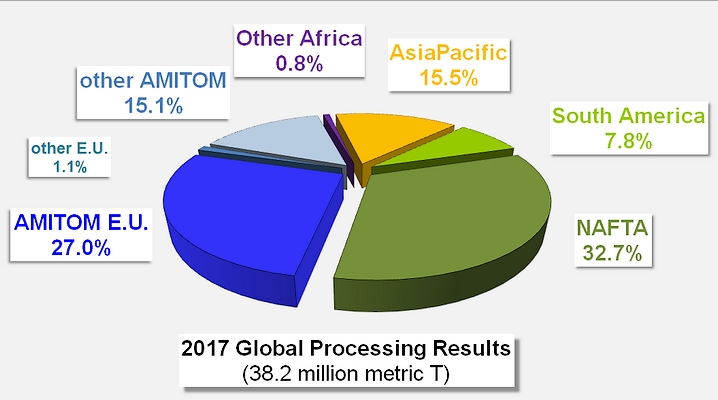

As things stand, operations in AMITOM countries should increase slightly this year (+485 000, +3%), with an overall target of 16.52 million mT, against 16.03 million mT last year. The decrease programmed in California is resulting in a slowdown (-970 000 mT, -8%) for NAFTA countries as a whole, as they are considering processing only 11.47 million mT in total in 2017. The Chinese industry has increased its objectives in the hope of benefiting from the relative weakness of US operations, and is planning to process 5.5 million mT, which is 350 000 mT (+7%) more than in 2016. In the southern hemisphere, finally, the acceleration undergone by the Chilean industry should lead to an increase in processed volumes of close on 300 000 mT (+7.5%), reaching 4.16 million mT this year.

The most up-to-date data collected by the AMITOM is presented below.

As of 29 March, Portuguese forecasts remained at 1.5 million tonnes. Like in Spain, the average price is EUR 70-71 /mT field gate, slightly down (-1 or -2 euro) compared to last year. Transplanting started in week 12 (19-25 March) but was interrupted by rain, then resumed rapidly and was carried out at full speed the following week.

In Spain, at the same date, forecasts remained at 3.2 million tonnes. Planted surfaces are expected to cover 37 200 hectares, for an average price of EUR 70-71 /mT field gate. Transplanting started around 19 March in Andalusia and was expected to start properly in Extremadura during week 14 (early April).

As of 29 March, the French industry reported stable planted surfaces and processed volumes in 2017, with 2 500 hectares planted for an expected crop of 190 000 tonnes, but with an increase in the proportional importance of organic production. A few smaller surfaces were planted during week 12, but transplanting was expected to start properly at the end of week 13 in the southeast and later in April in the southwest. Prices are slightly down compared to last year (-1 or -2 euro per metric tonne).

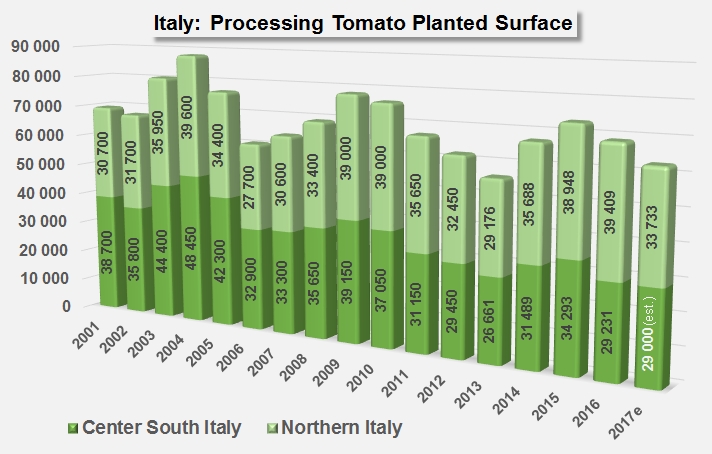

In northern Italy, as of 11 April 2017, the Pomodoro IO estimated that 33 733 hectares had been planted this year with processing tomatoes in the north of the country, for an expected crop of about 2.4 to 2.5 million mT. High temperatures contributed to the smooth running of transplanting operations during week 12, with the only remaining concern being the low rainfall recorded over the winter and the level of groundwater resources.

Just after Easter, very low temperatures (coming in from Russia and the Baltic countries) and some frost affected a number of crops in the region of Parma and Ferrare (80-100 ha). The affected fields were due to be replanted. (See also our article on page 5992.)

Just after Easter, very low temperatures (coming in from Russia and the Baltic countries) and some frost affected a number of crops in the region of Parma and Ferrare (80-100 ha). The affected fields were due to be replanted. (See also our article on page 5992.)

In the South Central region, planted surfaces were announced at similar levels to 2016, for an expected crop of 2.4 to 2.5 million mT. As of 11 April, price negotiations had still not been concluded, and growers were still rejecting the price drop requested by processors.

As of 29 March, the Greek industry announced no change to its forecasts, which remain at 480 000 tonnes. Transplanting had started in the south but was expected to reach cruising speed in the following weeks (end of March and early April). The average price remained stable at approximately EUR 73-74 /mT field gate, with upward or downward adjustments compared to last year

According to information obtained on 29 March, Ukraine's seeding operations started in plant nurseries on 11 March and transplanting was expected to start at the end of April. Production forecasts remained at 650 000 tonnes.

Tunisian forecasts as of 11 April remained unchanged from those of February. It is expected that 14 000 hectares will be planted this year, with an expected average yield of 65 mT/ha. Of the total production of 910 000 tonnes, 650 000 tonnes are intended for paste production (target production of 100 000 tonnes of 28/30 paste) and 20 000 tonnes for canning. Field gate price will be TND 147 /mT (about EUR 59.7 /mT). Planting started at the end of February in the Centre and Cap Bon regions, and by the end of March, 7 800 ha had already been planted (4 650 ha at the same date in 2016). The harvest should start in the first week of July 2017.

As of 29 March, the Turkish industry reported very slow negotiations as growers are not inclined to plant tomatoes this year.

Other WPTC countries

According to the information collected on 31 mars 2017, seeding started in China on 10 March. Transplanting was expected to start from mid-April in South Xinjiang and from end of April in North Xinjiang and Inner Mongolia. The total planted area is 938 000 mu (62 500 hectares) with an estimated fresh tomato volume of 5.5 million tonnes. At this date, the price was not yet fixed but the range will be between RMB 380 and 420 /mT (about USD 59 /mT).

In Australia, the difficult start to the season (heavy rain and low temperatures) has resulted in crop yields being lower than expected across the entire production region. As a result, the expected forecast for the season has been reduced to approximately 208 000 tonnes, down from the initially predicted 253 000 tonnes.

As of 31 March 2017, contract intentions in Canada appeared to be the same, or slightly up from last year (about 460 000 tonnes). Transplants were starting to be planted in the greenhouse, with favorable weather.

Regarding the price, the 5-year tomato pricing agreement signed by tomato processors in 2016 contains a formula that requires the CTGA price to be fixed, so no price can be reported until such time as the CTGA has announced their pricing. (See our articles in the September and October 2016 issues of Tomato News.)

So far this year in California, the story has been about the abundant amount of rain and snowfall. All areas in the state have seen their water situation greatly improve from previous years. As of 31 March 2017, with regards to planting, the southern part of the state was pretty close to being on schedule, with a few exceptions. In the northern part of the state, after being delayed by rains in March, plantings were expected to begin again by the first days of April. This area is about 10 days behind schedule. Negotiations for the 2017 price continued at this time. The estimate remained unchanged from the 11.6 million short tons (10.5 million metric tonnes) USDA/NASS figure released in January.

On 11 April, California’s industry confirmed that while planting was pretty much on schedule in the south of the valley region, it was delayed in the north by a couple of weeks due to rains, with the risk of losing seedlings in the greenhouses if rains continued.

As of 11 April, Chilean plants were in the last stage of their season, with 80% already harvested at the end of week 14 (2-8 April), with normal weather and yields, according with the latest estimation. Processors report they have high color raw materials this season, with good quality and color for the tomato paste. The season was expected to last longer than usual, until the end of April.

On 31 March, weather conditions in Argentina were reported to have been good since the start of the harvest, which was due to last until the end of April (about 80% already done). The forecast was maintained at 470 000 tonnes from 6 200 hectares planted.

Non Members

On 31 March, Polish processors announced that the production forecast has been reduced to 180 000 tonnes as no-brand companies have decreased their quantities because the margins for bulk tomato paste are too small. Seeding started in the greenhouses to plant a total of 3 400 hectares. Base price will be PLN 400 /mT (EUR 94 /mT). A total of 167 000 tonnes should be processed into paste, 10 000 tonnes frozen and 2 000 tonnes into juice.

Other US states

The total volume should be in the order of 500 000 short tons (450 000 metric tonnes).

Some complementary data

{kind=link}