News

Roundtable: Towards a Resilient Supply Chain in the Markets (Part 1)

The 2025 Tomato News Conference

Transcript of the roundtable: Towards a Resilient Supply Chain in the markets held during the 2025 Tomato News Conference @ANUGA on 5 October 2025 (part 1)

Click on the image above to watch the recording on Vimeo or read the transcript below.

All the slides are available HERE

Antonio Casana: We start the second part of the session with a roundtable on the market situation and it is my great pleasure to welcome our panelists to the stage.

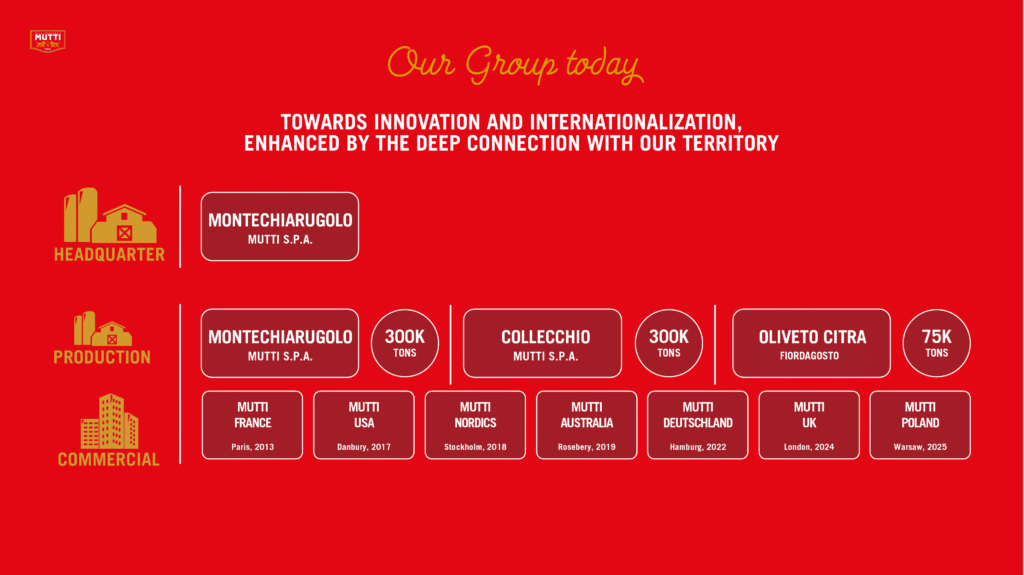

I start with Francesco Mutti, a distinguished guest who has been at the forefront of innovation and quality in the tomato industry. Mutti today is the leading brand for tomato retail product on the Italian and European markets, with a turnover higher than €700 million and the growth rate of double digit per year. In the last ten years, the company has grown significantly on the global scale, with company opening in Germany, France, the US, UK, Australia, Scandinavia, Poland with three factories located in Italy with a total processing capacity of about 800,000 tonnes, with an employment rate of 550 people, Mutti has grown from a well-respected national brand into international benchmark for excellence in tomato products, driven by a strong commitment to sustainability, transparency, product innovation and the valorization of the Italian agricultural heritage. Today we will have the opportunity to learn about these insights and visions. Please join me in welcoming Francesco Mutti.

The second panelist I want to introduce, I am pleased to introduce Manuel Vasquez who is a leading voice in the global tomato processing industry and currently the president of the WPTC and TomatoEurope. Manuel has a degree in mechanical engineering, followed by executive programs in Finance and Business Administration. Manuel’s entire career has been shaped within CONESA, the family company, one of the Europe key players in tomato processing. Starting the fields and production lines back in 1988, he officially joined the company full time in 1995 after roles in quality and production management, he was appointed CEO in 2004. Over the years, playing and build a truly global perspective, working closely with the industry’s largest users and stakeholders. Let’s welcome Manuel Vazquez to the roundtable.

I am glad to introduce Monica Souza, Vice President of Procurement and Sustainability of for Kraft Heinz across Europe and developing markets. Monica leads the sourcing strategy for one of the company’s most iconic ingredients, the tomato. A core component in the 650 million bottles of Heinz ketchup sold globally each year. With nearly 20 years of experience in the consumer goods sector, she brings the expertise in procurement, sustainability and strategic partnership. Now based in Amsterdam, Monica brings a perspective to procurement and sustainability, emphasizing that real progress in supply chain through a long term partnerships grounded in trust and shared value. Please join me in welcoming Monica.

Then it’s the time for Kitty Kitajima from Kagome. Kitty has worked in Kagome since 2009, first in quality assurance and in quality department and since 2024 she is Manager of Division Purchasing Department. Kagome, as you know, is Japan leading brand in tomato based food product and vegetable beverage. Founded in 1899, Kagome has grown into a vertical integrated company from seeds and agricultural production to final consumer goods, driven by a mission to solve social issues through food. While Kagome holds a dominant position in the Japanese retail market, the company has also significantly expanded its international presence, especially in the B2B and foodservice sector, with operations in the US, Portugal, Australia, and Asia. Kagome is also active in operator and sustainable agriculture and food technology, including AI driven smart farming, collaborating with NEC. Its commitment to environmentally responsibility to consumer health and innovation position make it a forward looking global player in the tomato processing setting. So welcome to Kitty-san.

Then I want to introduce, the last of our panelists. I am pleased to introduce Wolfgang DeMartino. Born in Milan in 1976, DeMartino holds a degree in Economics of International Institution. He began his professional journey in sales and local marketing at the CS Johnson Works. Between 2000 and 2002. Then, he moved to Japan where he studied the language and immersed himself in the unique characteristic of Japanese market. Since 2003, DeMartino has been a key figure in the growth of this company, helping to expand company revenue from 9 to 14 million euros. Under his leadership, the company has evolved from focus solely on brand tomatoes to a brand of Italian local across Japan, including new product category in Japan and Scandinavia and developing for private label project in Asia. At the end of 2023, the company was integrated in one of the Italian tomato leading group Casalasco, with the strategic aim to fortify its supply chain and solidify its market presence in the Far East and Northern Europe, with a keen focus on penetrating the markets of Japan and Scandinavia. So today we bring to our roundtable the experience and truly global perspective on the future of tomato processing industry. So welcome Wolfie.

Starting from Francesco Mutti. I want to start with a question regarding, market evolution and brand strategy. Your company has successfully combined a deep respect for tradition and, also for innovation, a balance that is increasingly difficult to maintain today because of the competitiveness around the world. So Mutti remains focused on a single iconic raw material. While many global competitors of are much more diversified portfolio of products. How do you turn that focus into a competitive advantage? and what are the key factors that allow you to grow in such context? Then coming to consumer preference trend, how do you see the evolution of branded product versus private label and discounting offering in a price sensitive environment? Do you believe that the value of a trusted brand is maintained and willing to grow, or PL are approaching a structural shift to the retail landscape?

Francesco Mutti: Well, it is very a long question. Let me first, thank you and everybody thank you for being here. But let me introduce the conversation with a few slides regarding this. We just have a full idea of who is Mutti.

Basically, it’s a company that works only on brand or its own brand, with a purpose that is bringing to market, as you mentioned, that iconic fruit at its best, meaning really giving back the value of the tomato.

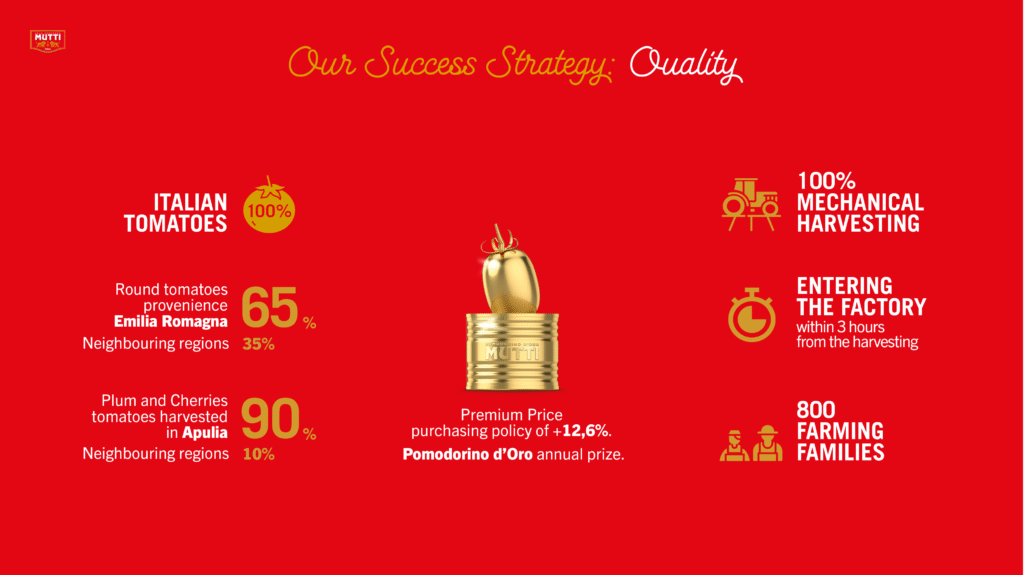

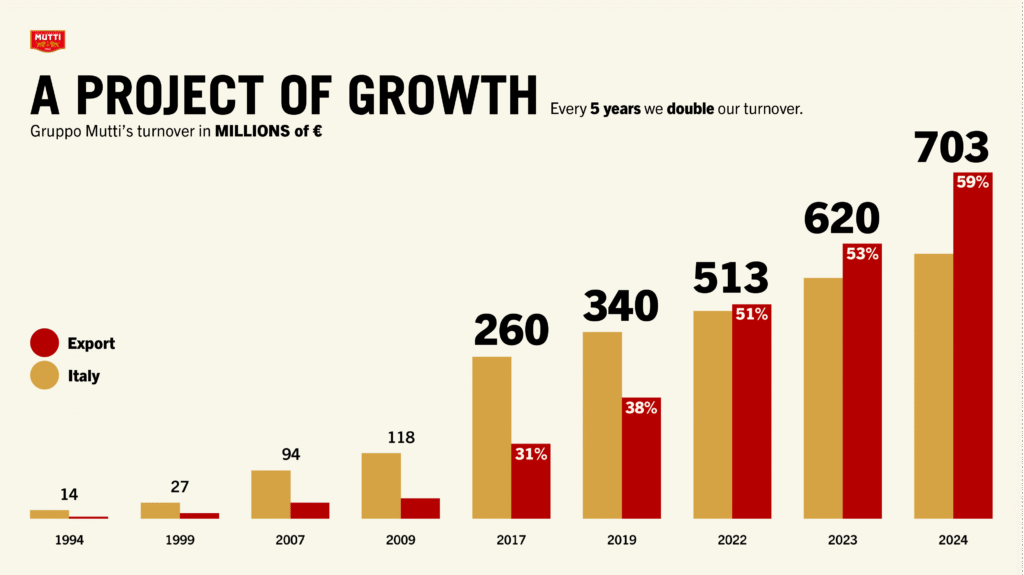

I made this, structure very simple. We started in Montechiarugolo, this small city village in Parma. We have three plants which processed this year something like 700,000 tonnes. Then, as Antonio mentioned, we have different subsidiaries now producing all the tomatoes come 100% from Italy.

We invest on Quality. I think the three pillars on which we build in some way, this development as being innovation, quality and sustainability.

Investing in quality is not just words, but means that we invest a lot. It means that on average versus the market, our cost of the raw material is above 10% per year, being quite large, at least in Italy with 700,000 tonnes, having a premium mass that goes well above a 10% usually have economies of scale, usually try to reduce the costs of the tomatoes. In this case, we invest a lot on farmers demanding a different quality. And there are a lot of incentives to ameliorate constantly the quality of the tomatoes delivered.

And when we are talking about what will be the trend of the consumer, that will depends a lot from the ability of the brand of a company to deliver a different quality. We have to imagine that in any case, a company like Mutti is selling something like half a billion pieces per year, that means that millions and millions of households of people that goes shopping decide every year to buy constantly, a single product that maybe has a different price positioning. So it cannot be just storytelling. You have to be very, I think, consistent. And the basis and the pillars of your company. And the first one definitely is the quality of the raw material and consequently the investment that after the technical investment, the quality, the finished product.

Innovation is another key pillar. We work only on tomatoes, definitely, but we stretch our lines moving from, well, let’s announce a couple of milestones of what has been done.

In 1951, the first tomato paste in tube was born in Mutti, as a product like pulp that was born again in 1971 in Mutti. We invested a lot, at the time the company was, I mentioned, a little different for, the capability of tracing the origin of the raw material starting from a finished product. At that time, there was again, like now in the latest years, a Chinese import in Italy and being able to recognize really the origin is fundamental. But then we can we talk about salsa datterini, the most sold SKU in Italy, or the Instafactory that is a company that goes into the field to produce, or the new categories like the pesto, and I mean in any case that the first ingredient is tomatoes, or the soup, chilled products.

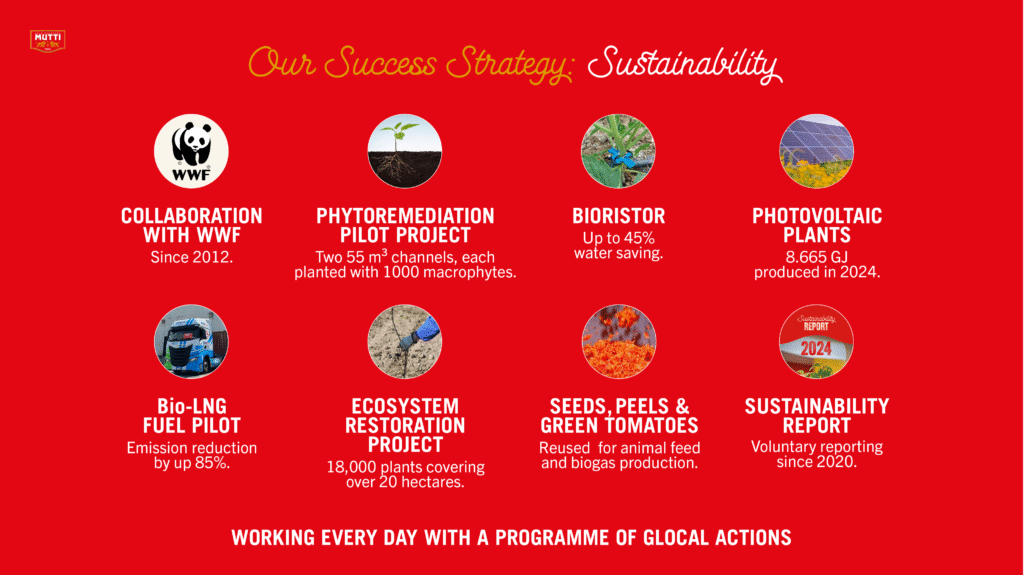

We invest a lot obviously in Sustainability. We started working with WWF since 2012. We have project like, the bioristor that is a project to reduce water consumption. Then the big question is we have too much or too little water. Again, the restoration project, more than 18,000 plants covering more than 20 hectares in the in the pianura padana.

And we could continue innovation and Communication, also big investments with a different approach per single markets.

And that bring us into a complete shift in the recent years from a mostly Italian company with a turnover originated mostly in Italy, in which if you want the culture of tomatoes is deeper, versus an internationalization.

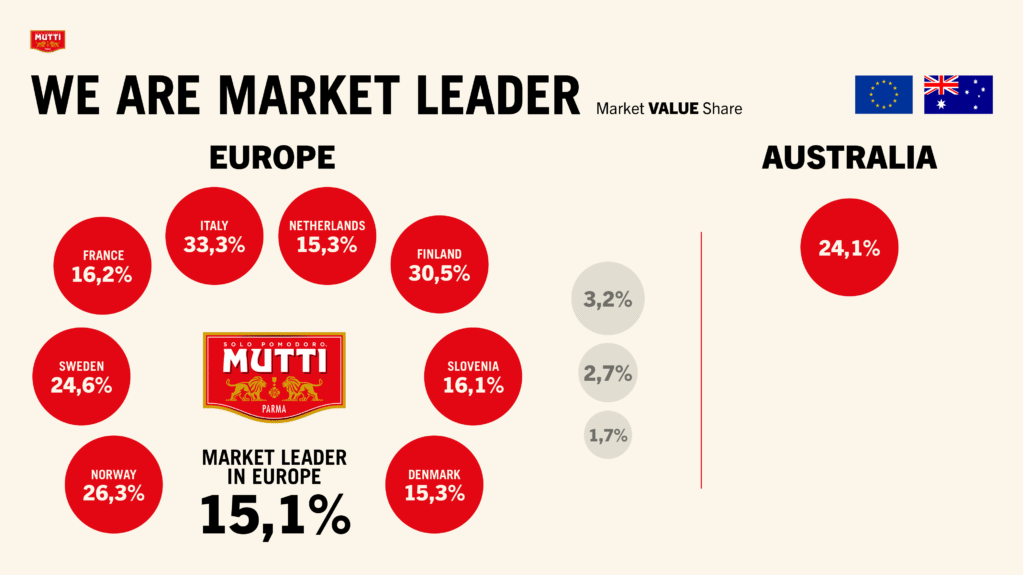

Now, we are brand leader in Europe with a 15% market share. The three grey areas are the market shares of our first three competitors as a brand in Europe.

And why I put it in this way. Because the big question and big challenge nowadays, to me, is really the difference between the brands and the private labels. And that’s stand from the capability of the brand, in that case to compete versus the private label. So the more you are able to deliver a better quality, significant, recognized, better quality, the more you have able to bring innovation, you can compete really with private label. Otherwise, if it’s just a brand and not supported, you do not have really this constant and significant pillars who makes a difference then? It would be a matter of prizes and private label definitely would be more aggressive versus a single brand.

Antonio Casana: Thank you Francesco for your insight. I forget to mention that we had a request for making some recording and interview and film of this section. So France TV will do that. If someone has any problem about this, please raise your hand, otherwise we continue in this way.

So we move to Manuel Vasquez and, I want to ask you, Manuel, in light of increasing climate disruption, logistical bottleneck, evolving trade and tariff policy, and the shift from the global to more localized models. What in your view, are the key principle or strategy that tomato processor should adopt to ensure continuity and resilience in their supply chain? We are also seeing a growing trend towards consolidation and polarization in big groups, the global tomato industry. Do you believe that scale remains the most important competitive advantage today, or is there still room for regional or niche processor to succeed? In your experience, what would be an optional scale for a tomato processing company in markets like US, Europe and China? Finally, and as someone who leads a major global player as you, we will appreciate hearing from, your broader vision on how the tomato processing industry may evolve. And then over the next decade, which trends do you see and trust transformation you foresee shaping our future?

Manuel Vasquez: Okay. So good afternoon, everyone. Thank you for inviting me. And there are three very deep questions. So I will try to answer starting by the key principles or strategies to adopt in order to ensure continuity and resilience. Which is the first of all, diversification of all of product production areas for reducing the impact of weather and diversification of products to attend wider the range of customers and markets will be key.

I would say that our companies could be an example of that. We operate two fresh processing units, in Portugal in two different areas. We operate three, first processing plants in Extremadura across two production areas. Two first processing facilities in Andalusia in southern Spain, and one first processing facility in China.

Then we have, looking at tomato powder, one of our key ingredients. We have three facilities in into continents, looking to retail or food service. We operate two dedicated lines for second processing units and for food service we have two lines, around the several plants.

Another key principle, I think for the future is to have extra capacity. This is becoming critical when weather like this year in Spain is shortening the window for transplanting and then for harvesting. So to have extra capacity allows to process in less time than usual or absorb peak of production caused by weather.

Another key principle would be to be very close to farming. The farmer is the first link, the first part of the value chain. So we need to be very close to them, explaining what the market is demanding and helping them to adopt new technologies. At CONESA we have our own farming operation. We are farming around to 2400 hectares of tomatoes and our operation works as a large scale lab where we are testing out of different varieties, new technologies, a range of different farming practices, and specialty crops with the ultimate goal to transferring the knowledge to the growers so they so that they can become more sustainable and competitive. I think also that the new technology adoption and digitalization is key both in factory and farming. Innovation is crucial for competition currently. With the artificial intelligence emerging as a transformative tool I think technology adoption and digitalization are going to be, are being, very important. And finally, as another key principle or strategy for ensuring the continuity and resilience of the sector, I think the flexibility and adaptability. The workforce resilience is key, but also the culture of adaptability and being able to supply the market very fast. The retentretention of talent is key. You know, what they say is, it’s very difficult to have a talented people to retain them is very crucial for the future.

Moving to the consolidation of scale, which is the small processors or niche companies will start in by scale. In my view, I think scale and size is essential in any business, not only in tomato but mainly in the tomato industry. It gives the companies a lot of visibility and then helps to generate opportunities. It also strengthens negotiation power with suppliers and customers and crucially in an industry with a tight margin it helps dilute fixed cost. So I think that the economies of scale, global customer alignment and capital intensity define competitiveness in our in our sector.

Talking about, consolidation. Well, in the last ten years, we have seen a lot of consolidations and the of closing factories in the mainly in USA and in Europe, basically in Spain and Italy. And I think that we will continue seeing the consolidations and closures. Of course, that said, there is always room for regional, regional or niche companies who specialize in premium products or very specific or regionalized markets. I will say that the specialization, flexibility and proximity to customers can present, a competitive advantage for medium small size industries.

And you asked about which is the optimal scale for a factory, and this is very, very difficult to answer as it depends a lot on different factors, like the length of the crop in each region, the type of products that the company is producing, the market it is operating in … But even if we just look at, for instance, tomato paste, and if we look at the U.S. for instance, the companies range from 500,000 to 1.2 million metric tonnes, with the exception of morning by far the biggest scale with 5 million tonnes, so that would say that if we look at these figures, probably the optimal minimum optimal size in this stage would be like 500,000 metric tonnes per crop.

If we look into into China and we just look into two main players that are COFCO and Chalkis, the average size per factory is around 170,000 metric tonnes per crop. So that suggests that this could be the size or minimum size in China.

And I will say that this for a single place producing in Europe that could be probably the minimum size. That size allows you to invest in technology or to dilute the fixed cost. But, of course, as I said before, there are smaller factories, but typically not oriented to paste, but to other retail or foodservice products and also products like low brix, diced, wholepeel tomatoes or other specialities.

You asked about the future or the new trends. So I think I believe that we have already touched on most of the factors that will shape the future, but I will say that we will in my opinion, we will continue seeing consolidations, especially in paste production. The paste market will remain highly volatile and competitive, with probably only the most efficient countries and companies surviving. Adaptability to climate challenging will be crucial, but also diversification and specialization across products, formats, markets and customers also will be very important. Probably geopolitical instability will continue to disrupt and reshape trade flows, so we need to keep an eye on this. Sustainability as a competitive currency. So probably carbon, water and phytochemical footprints will become increasingly necessary for retailers and brands. And we will see or we are seeing a technological acceleration again, both in farming and processing, and those that adapt quickly to the new trends will be more competitive. Finally, I think that we will see an evolving consumer demand, with probably a focus on health and functionality, convenience and customization, premium and locally authentic products.

Antonio Casana: Thank you, Manuel, for your vision to sharing your key principles. And then now, yes, to Monica. Regarding, your, company, your global vantage point, what do you see the most urgent systemic shift that the industry must collectively address, whether regulatory, geopolitical or consumer driven, and specifically how your company, Heinz, is approaching consumer transparency in an era when aging, ethics and sustainability are becoming top of top of mind for shoppers around the world.

Monica Souza: Thank you. So before I answer, I would just give you a quick introduction. I hope that all of you have a product from Kraft Heinz on your shelves or in your fridge. But basically we are the fifth largest food and drink company in the world. We exist with the purpose of create and elevate food that makes us all feel good. And it feels good from a quality perspective, from a product perspective, but also when we know that we are doing what is right for the planet and also for the people that are living in it.

We produce and sell globally over 650 million bottles of tomato ketchup worldwide. So you can imagine that to be able to produce all of that, we do need a lot of tomatoes. Therefore, I’m very happy to be with all of you in this room, because obviously we are the biggest, processed tomato buyer in the world today.

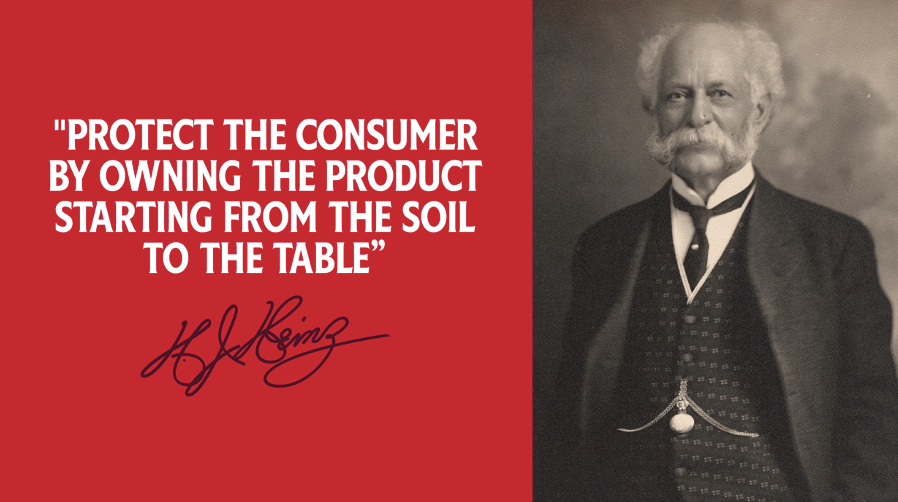

And that, comes with a strong belief that actually is something that our founder said, many years back, and it’s our belief up until today that is our duty to protect the consumer by owning the product, starting from the soil to the table.

And that’s why we are here to talk about this today. Because for us is not only about what we are putting on the shelf and what Francesco is saying, that is really important to make sure that we have the right quality and that we are creating this differentiation for the consumers. But it’s also starts with a responsibility to protect the soil and all the elements of the farming system that are going to guarantee that we have the product at the end of the day.

And that is only possible with true partnerships. And the partnership, for example, that we have with CONESA and with Manuel who is sitting next to me, is one example, but we have other partners of Kraft Heinz in this room.

Definitely, the way that we see it is, we start with our Heinz Seeds business. We deliver the seeds to our growers, to our partners. They nurture the seeds, they process these tomatoes, and they deliver this back to us in the form of paste that we are going to use to produce our tomato ketchup, our beans, our soups, our pasta sauces and so many other delicious products. But coming back to your question, Antonio, I think that the biggest thing for us, I could quote actually the title of the previous panel. I think that there are at least four pressing themes that we are very concerned about. The first one is obviously about climate change and sustainability and what we are doing in that field as I mentioned, I think that is really about what I was talking about in terms of partnership. So how can we make sure that we are optimizing the utilization of the resources that we utilize, be it the soil, the water, and also, the energy utilization and the water utilization when it comes to processing the tomatoes in the factories. We have recently done an investment, with Manuel in Mora in Portugal, where we have been able to optimize drastically the utilization of all water, so we are utilizing 80% less water in our processing facility. And with an outcome of that, we are also able to reduce the utilization and the emissions of CO2 by 20% in that facility. So we are very proud of this co-investment that we have done with CONESA.

To give you an example, the two other things that we are seeing as well is obviously the consumer trends, and we were talking about private label and how this is changing and shaping the future, especially here in Europe. And it’s a trend that we see that is going to start flying all over the globe.

For us is really important to continue to focus on the quality again, starting from the field, but to create differentiation, and to be able to offer products for the different types of consumers that we want to achieve. One recent example that we have done is the Heinz Zero, which we have recently relaunched. That actually utilizes 35% more tomatoes, but has zero added sugar and zero added salt. And with this innovation, we are being able to achieve more in consumers with incrementality., that is something that we always need to be concerned about how we can continue to grow and make sure that we are targeting and achieving the new generations.

And then the last piece that is also a pressing matter for us is obviously the global trends and, the whole trade situation that we are facing. I think that at despite we are a global company and we obviously have a global network, and Manuel was talking about the scale, this is something that definitely plays in our advantage. Fortunately, when it comes to Europe, we are very much centralized in Europe. We have eight factories here, more than 4000 employees. Actually our R&D center, and they see a few R&D colleagues here as well, is located in Nijmegen in the Netherlands, where we are actually developing these products such as this Heinz Zero that I just mentioned.

And obviously, 80% of our ingredients and packaging is actually sourced from within you. So we are constantly looking for opportunities to localize, but also to futureproof our supply chain and the resilience of our ingredients and our packaging. I think that it’s our objective as a company is obviously we have been here for the past 150 years, and we want to be able to be here for the next 150 years as well. So, obviously that we need to be constantly looking at all those different trends and challenges, but through strong partnerships, such as the one that we have with, Manuel, CONESA and a few others here in this room.

Antonio Casana: Thank you Monica for your vision and sharing your strategy. Now I come to our distinguished guest from Kagome, Kitty Katijima. Kagome is a brand leader in Japan for tomato products, but in recent years, the company has expanded its footprint globally. While your domestic focus is primarily on branded consumer goods, so your international strategy seems more centrally on B2B and foodservice, could you share Kagome global strategy for becoming one of the top five players in the world? What are the key priority and challenges in achieving that goal?

Kitty Katijima: Firstly, thank you very much for the opportunity to speak in this round table. It’s actually my first round table, so I’m kind of nervous but I know Manuel-san and Casana-san so I’m pretty comfortable now. Anyway, before answering the question, I’d like to quickly go through the presentation I prepared. It’s actually prepared for this meeting, so it’s not like company introduction, really great PowerPoint, like Mutti or Heinz, but I just want to quickly go through this.

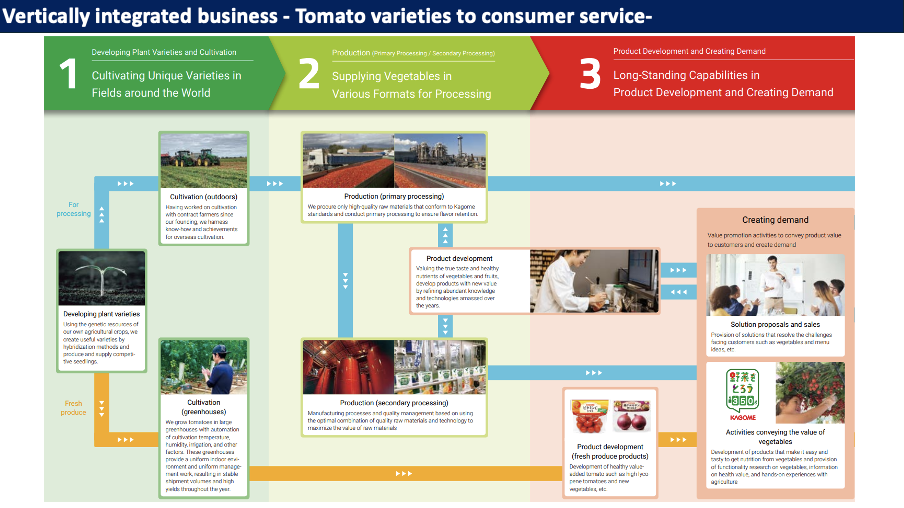

So you are aware, Kagome has got, basically integrated business from Seed United Genetics, primary processing like HIT or Kagome Australia, and we acquired Ingomar last year, and we got secondary process in the United States and, of course, in Japan as well.

And recently we started the service to encouraging vegetable or tomato intake in Japan.

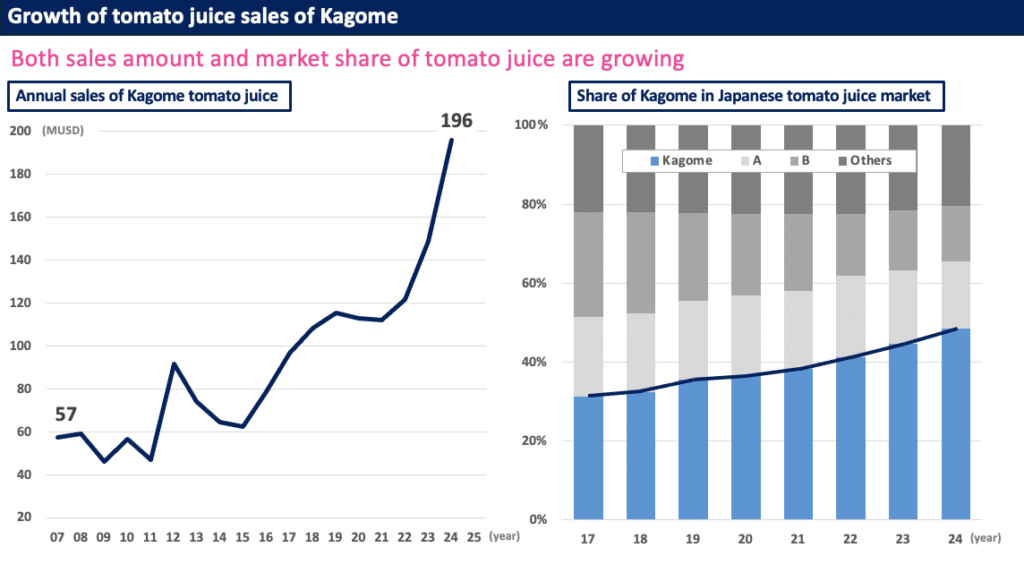

This is actually the latest sales in Japan for Kagome tomato juice. As you can see around 20 years ago, the volume is quite small, but in the recent five years, you can see dramatically the sales is going up and it is actually converted to United States dollars. So and you know that Japanese yen is pretty, pretty weak compared to USD, but still the sales going really up, in recent five years. And the graph on the right hand side is a share of tomato juice of Kagome in Japan, and this share is also growing as well.

To keep that kind of situation Kagome of course doing some strategy to keep the sales. The first one is we do fresh squeeze. It’s actually limited time and but it’s domestic tomato. Or we do produce some high lycopene tomato juice. It’s actually from Conesa and we do some health claim on the product packaging to encourage people to support the health as well. And we actually have a health claim on traditional tomato juice as well. And we do some sweet tomato juice for the people who tend to hate tomato, real tomato taste. We think that the tomato is too sour or too green or, you know, whatever. So we have a lot of product line up to have tomato juice sales more and more.

And as I mentioned recently, we give some service to everybody to encouraging vegetable intake. And this is a different action to increase Kagome fans, especially future fans. We provide some nursery plant to kids freely to support them grow tomato at their home or at their school as well. And then they feel that vegetable growing is close to their life. So they have some interest in to tomato growing on tomato product or food.

And this is a theme park, very next to one of the Kagome plant in Nagano Prefecture in Japan, and we do support some biodiversity in that area to grow some original plant around there, and we do support some educational activities in theme park as well.

This is very new, for it’s actually released two, three days ago. We established corporate venture capital in the United States, and we announced new development of 100% biodegradable, plant based water retaining polymer. It’s actually not designed for tomato growing but that’s tested in Ingomar fields. So that’s a point of actually, our global strategy.

So I’m going to finish this, presentation here. To answer the question, we got, midterm management plan, of course and it’s actually smart for Kagome. And we set goal to pursuing both organic and inorganic growth like this. So this is the example for inorganic growth. And, like I mentioned, the acquisition of Ingomar is a prime case for us for our global strategy to improve the supply side, to benefit market side. It means that, we can tailor made the ingredient to match the product, products concept, compared to using the commodity ingredient. To catch up with the global marketing side, we are accelerating business in the regions when where population growth is expected, like in the United States or in India. And at the same time, we are starting the opportunity to find new production areas or new market all the time as well.

Antonio Casana: Thank you Kitty-san for your presentation and for introducing for the and for the vision of your company.

I want to ask Wolfgang DeMartino about his experience, in North America, in North Europe and Asian countries. What do you think are the most challenging factors in supply chain to maintain competitiveness today? And what role do you see for consolidation and strategic alliance in the future for tomato processing sector?

Wolfgang DeMartino : So as everybody else, first of all, thank you for your invitation. Thank you for inviting me with such esteemed companies in person I know more or less. And, so my experience is, basically, we are buying and selling and involved also in logistics and logistics is becoming. So when I graduated in university, I have done a degree in the, in the logistics and at that time, it was 1999, there were the multimodal operators. There were the new things in the market. And nowadays the market is completely changed and the supply chain has been sometimes managed by these, and sometimes it has been anyway affected. So advantages and disadvantages like everything. The supply chain to my personal opinion, to my experience has been, hit by the consolidations of carriers around the world, especially for among shipping companies. When I started this business 23 years ago, they were I think something like 20 shipping companies, all independent so it was easy for direct business or even for orders, so picking the best conditions. But now there are only basically three alliances controlling the market and deciding what to do in terms of services, ports to be supplied and availability of empty containers. And this has affected a lot and this is affecting a lot actually, the availability of goods around the world, especially during geopolitical situations, which Manolo cited.

These can this is being controlled. So this situation is being controlled by operators in several ways. One of those has been using for orders, even if shipping companies to try are trying directly to make business with the companies, even small companies like mine. But it’s not easy to direct business direct relationship with them because I think to my experience, it would be necessary a kind of specific office dealing with the shipping companies directly. And this would mean, knowledges and costs for companies, even if good advantages would be brought to the supply chain. On the other hand, this grants some of the flexibility to the business.

Then talking about the products themselves, what I could see is that so companies have seen the hurdles not only from the supply chain point of view, but also from the economic and financial situations around the world, starting from the Covid, but several things later on, and that there have been some endogenous and exogenous problems for companies themselves, mostly for packers and for brand leaders, less for trading companies of course. The exogenous hurdles are the structures because the markets are changing very fast. So several years ago, I was thinking about the markets, so looking ahead, I was trying to look ahead, let’s see, one year or even more. And now I cannot see that more than two months because thanks to the social, social data in social, systems.

So trends in markets and consuming trends and consuming tastes are changing very fast. And companies I think they have these are tools to be flexible enough to face these and to read these fast, because I think that we don’t have enough information studies from the markets to read the markets ahead. And this is the other problem. Anyway, the structures should be more flexible to face the problems. And this is the endogenous. The endogenous are the partnerships or the consolidations. The partnerships are like Monica cited with the CONESA. And I think that that Mutti will have the same. And I know that Kagome has the same. And these can be something helping the companies, brands, private label, whether what you want, to face the reality, which is a very fast changing reality and, and cost facing reality because we are all aiming to be friendly to the environment, friendly to the prices or lower prices and so on. And t looking at the climate change and also to the food waste because that is another big issue for us. But it’s a matter of balance, because if we go for the climate, for the environment, then the price will be affected. And some buyers don’t want to, don’t want to listen to that.

Yesterday or to two days ago when I was leaving from Bologna airport, I’ve seen in a shop, a phrase apparently said by George Armani, and the phrase is over there. It says, so the concept is that Giorgio Armani think is to leave the lives, to leave a mark thinking of people and of the reality in terms of respect. So strength to the efforts and attention to the people and to the reality and the people for us are not only the consumers, which are so kings for us, of course, but also the buyers, because the buyers sometimes need to be driven because they have too many things to do, and we can be helpful to them.

Further to my experience, so small part in Japan and small part in Scandinavian countries, I can see that I learned a lot for the supply chain and for the product trends from both areas. In Japan, I learnt the mindset and the approach to do business. So in terms of building projects, as long so with a long view, as long as possible long view projects. So with the facing the problems countermeasures and then going ahead with this. So looking at the stability in terms of supply and also delivery.

From the Scandinavian countries, I learned efficiency and capacity of team building to find new to, to build new projects. And I am trying to I’m trying to apply these things all over the other areas I’m working with, because I think there is a lot to learn from these two areas in a long view, in a long view, which are not easy because there is no simple recipe to find solutions.

I think it’s the marketing mix that has changed in terms of topics of the marketing mix. Because I was studying in the university globalization and after the globalization, there was localization and then glocalization and now other things. So everything changes in two months. So I think the companies sitting in this round table are really heritage I think because they’re facing markets which are really complicated and if you manage to deliver your ideals, your profile, it’s the main, I completely agree with what you said until now.

Antonio Casana: Thank you Wolfie for your thoughts and I think we had the opportunity to learn from you, from your perspective.

Now, I come to the second question and I ask you to be brief, in order to have some time, also for the Q&A section.

The Q&A section is published in Part 2 of the transcript

{kind=link}