News

Pakistan’s Industrial Tomato Sector

Following up on our conversation with Khurram Irshad, Head of Sales of Simta Foods Private Limited, a company involved in the cultivation and processing of tomatoes and other tropical fruits in Pakistan, we investigated the Pakistanis Industrial tomato sector.

The Pakistani tomato industry is currently characterized by a significant disparity between primary production and industrial processing capacity. While the nation maintains a substantial agricultural footprint, structural inefficiencies have historically limited its role in the global processing market. However, recent initiatives by local processors and increased engagement with international bodies suggest a shift toward industrial modernization.

Pakistan’s tomato industry is characterized by high volatility, with production concentrated in specific clusters as follows:

- Balochistan: Leads in volume, accounting for ~40% of national output.

- Sindh: Holds the highest land allocation (38%) and contributes ~25% of production.

- Punjab & Khyber Pakhtunkhwa: Punjab yields higher outputs on smaller acreage, making it a strategic hub for processing facilities.

Pakistan produces between 760,000 and 800,000 metric tons of fresh tomatoes (for the fresh and processing markets) annually across approximately 70,000 hectares. However, seasonal gaps often force the country to import fresh tomatoes, primarily from Afghanistan (approx. $42.6 million in 2024) and Iran (approx. $9.6 million in 2024), especially during the winter months.

Despite its agricultural footprint, Pakistan’s processing sector is still emerging. Local demand for processed tomato products is growing at a CAGR of over 8%, driven by rapid urbanization and the fast-food (HORECA) sector.

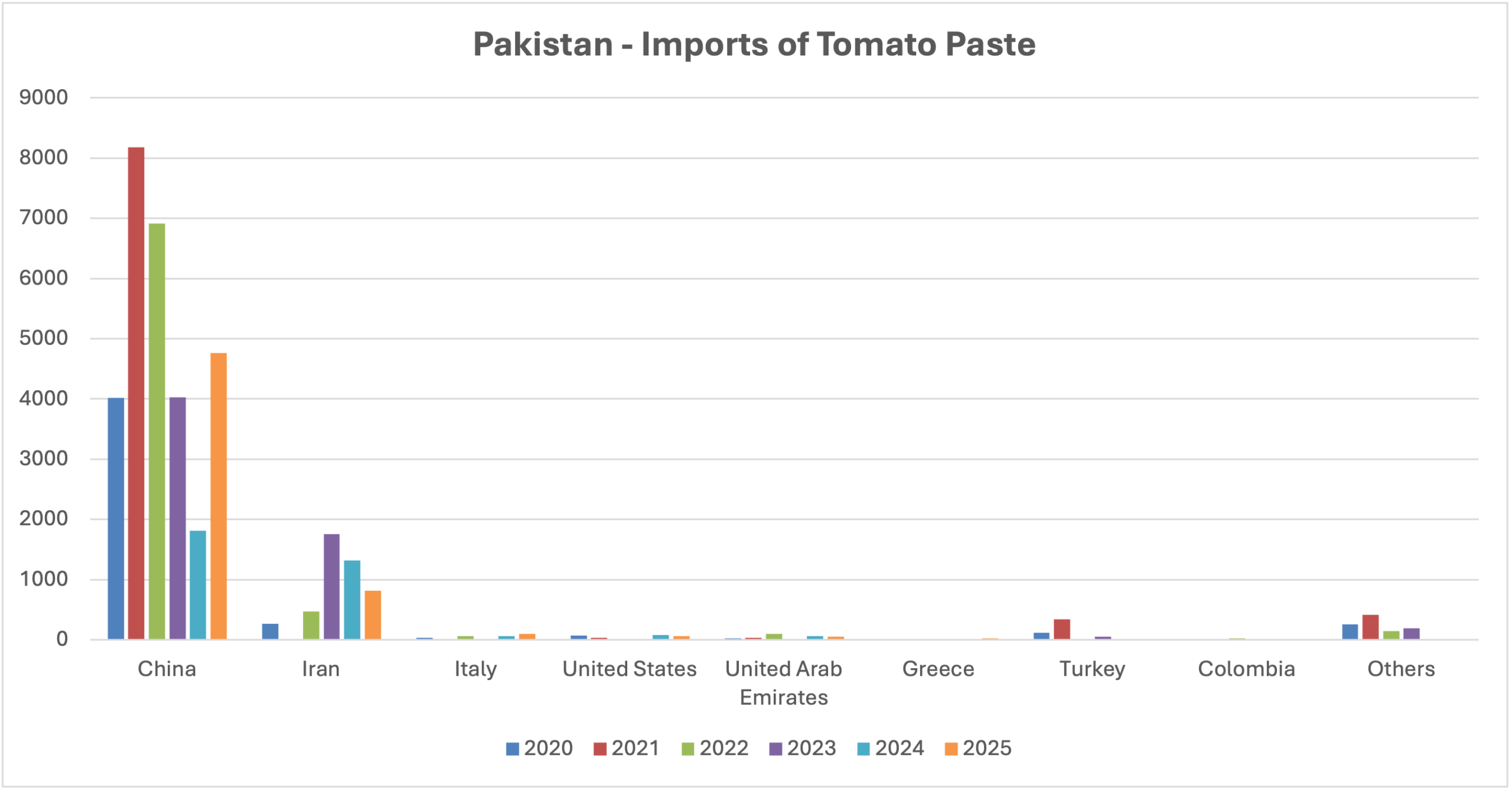

Pakistan has historically imported nearly $10 million worth of tomato paste annually to meet the demands of its ketchup and sauce industries. China is the overwhelmingly dominant supplier of industrial tomato paste to Pakistan.

Pakistan’s tomato import landscape is currently defined by a strategic shift: the country is moving away from a heavy reliance on expensive imported tomato paste toward localizing the entire value chain. While fresh tomato imports remain high to cover seasonal gaps, the industrial focus is on “import substitution.”

The sector also faces a critical challenge in post-harvest management. Industry data indicates that 30% to 35% of the total crop is lost due to supply chain inefficiencies, inadequate cold storage, and logistical bottlenecks.

Currently, the domestic processing industry utilizes only a fraction of available raw material, accounting for roughly 50,000 tonnes. This underutilization forces a heavy reliance on imports; approximately 80% to 85% of the tomato paste used in Pakistan’s growing condiment sector is currently sourced from China.

There are currently a few tomato processing companies in the country:

- National Foods Limited: Launched a $10M import-substitution project now transitioned into Verdora Ventures to scale corporate tomato farming.

- Shangrila Foods: Known for Vacuum Cooking Technology (VCT) which preserves lycopene and color without artificial additives.

- Shezan International: Known for being one of the oldest processors with multi-province facilities in Punjab, Sindh, and KPK.

- Mitchell’s Fruit Farms: One of the oldest integrated facilities; owns 450 acres of farms in Renala Khurd for direct sourcing.

- Ahmed Foods: A legacy brand with a strong presence in both local and export markets (Middle East/UK).

- Simta Foods Private Limited: New industrial-scale processing (15 tonnes/hour) focused on 36-38 Brix tomato paste.

- Matco Foods: Primarily a rice exporter that has diversified into the “Falak” and Friends” brand for ketchups and sauces.

- ITT Foods (Brand: Dipitt): Focuses on “real tomato” artisanal batches and export-quality gourmet sauces.

- Volka Food International: Large-scale manufacturer based in Multan, focusing on high-volume production.

As a new entrant, Simta Foods exemplifies the shift toward high-spec industrialization. With a 7-acre facility in Vehari, Punjab, and corporate hubs in Lahore and Multan, the company is bridging the farm-to-factory gap.

- The facility utilizes a 15 TPH (Tonnes Per Hour) processing plant equipped with state-of-the-art Ing. A. Rossi machinery, aiming for a daily output of 35 to 40 tonnes of concentrate.

- Beyond tomatoes, the facility processes tropical fruits, producing high-brix concentrates for:

- Mango (Desi & Chaunsa): Up to 28-30 Brix concentrate.

- Peach, Guava, and Strawberry: Ranging from 8 to 32 Brix.

- Simta has integrated 450 acres of corporate agricultural land. Through collaboration with Syngenta, they are testing specialized hybrid seeds, looking for higher brix seeds to maximize factory yield per ton of fresh fruit, aiming for a naturally thicker paste that reduces concentration costs.

The industry also faces other challenges such as:

- Seasonal Price Spikes: Prices often skyrocket in November due to the “crop gap” between the Sindh and Punjab harvests, leading processors to rely on stored paste or imports.

- Climate Change: Unusual rainfall patterns in Balochistan and heatwaves in Sindh have recently reduced cultivated areas by up to 40% in some regions, according to 2024-25 estimates.

- Corporate Farming: There is a move toward corporate farming models (like Verdora Ventures) to ensure a consistent supply of “processing-grade” tomatoes rather than relying on the open “mandi” (wholesale market).

The viability of tomato processing in Pakistan is heavily dictated by geography and climate. Transport costs remain a primary variable; however, processors have identified that sourcing from the southern regions can effectively extend the processing window from 60 to up to 130 days. However, transports costs will increase (based on 4 to 8 hours transit time), therefore price of raw material needs to be low enough in these Southern regions to offset the expenditure for processors.

The transition from the open “mandi” (wholesale market) to corporate farming models like those of Simta Foods and Verdora Ventures (National Foods) is essential for consistency. By addressing the 30-40% post-harvest loss through direct-to-factory sourcing, these players are stabilizing the value chain.

Looking forward, Simta Foods plans to introduce an additional higher-capacity line in the coming season. This expansion is part of a broader national trend: transforming Pakistan from a volatile fresh-market economy into a competitive player in the international tomato concentrate trade.

About SIMTA Foods

Simta Foods is actively working on a zero-waste processing model. They are currently developing upcycling initiatives for by-products generated during processing, including tomato seed oil, lycopene extract, mango kernel oil, and mango kernel butter. This is the first phase of their sustainability program, and they plan to continue R&D to identify further opportunities for upcycling by-products from tropical fruit processing.

To further improve our environmental footprint, they are also in the process of installing a solar energy system at the facility to reduce reliance on conventional energy sources and move toward a more carbon-neutral operation.

In terms of compliance and quality assurance, Simta Foods will also be obtaining internationally recognized certifications including FSSC 22000, SEDEX (SMETA), and Halal certification.

Statistics (Source: TDM)

Import data shows a strategic reduction in Pakistan’s reliance on Chinese tomato paste, which peaked in 2021 before declining as local “import substitution” took hold. While global price surges and supply chain shifts pressured margins, Iran emerged as a key secondary partner to bridge seasonal domestic gaps. Despite a slight projected uptick in 2025 to meet rising demand, the overall trend reflects a successful move toward sourcing high-brix concentrates from within the domestic value chain.

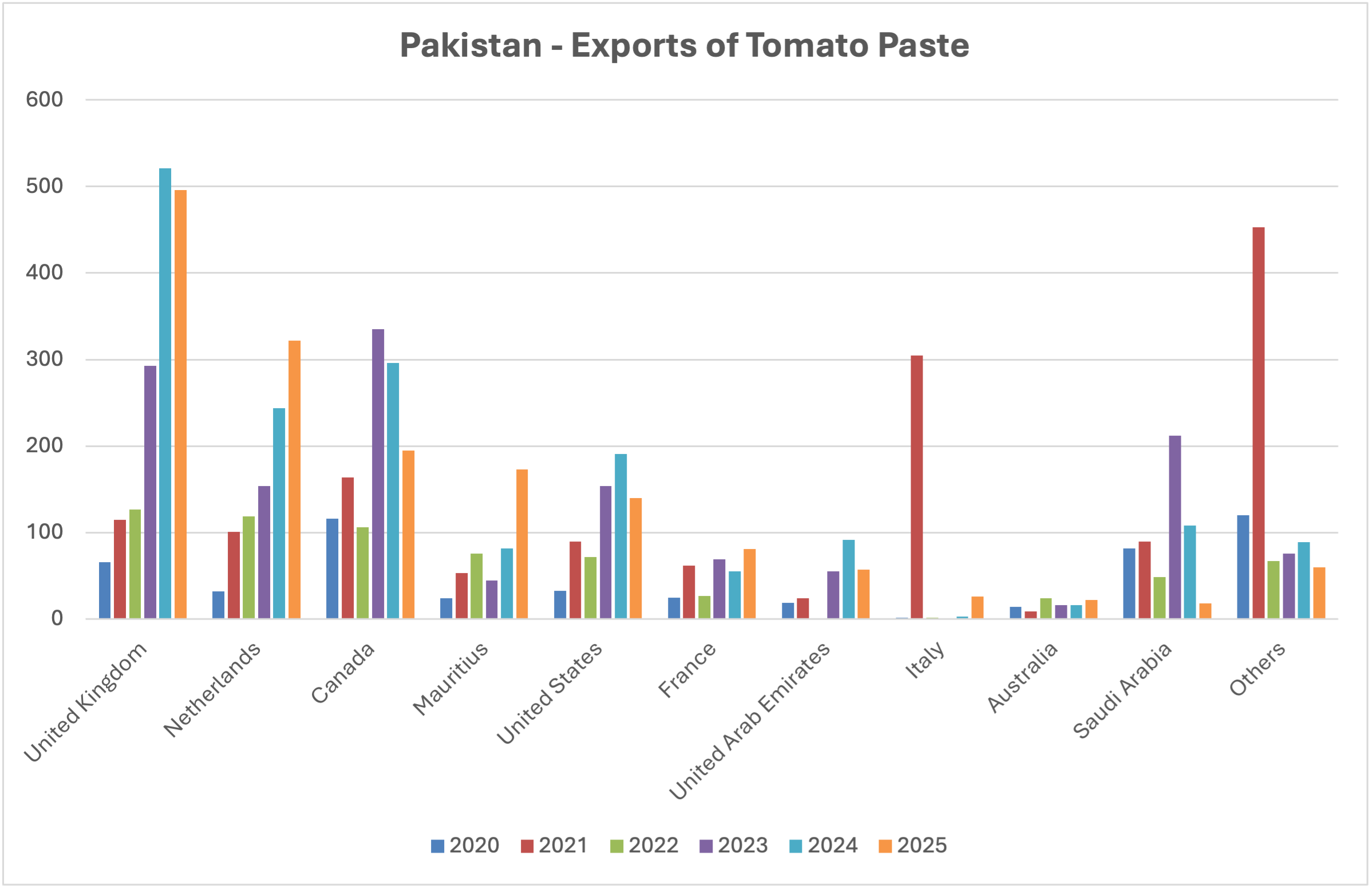

Pakistan is rapidly transitioning into a competitive exporter, with a steady climb in tomato paste shipments to the United Kingdom and the Netherlands through 2025. This growth indicates that local facilities are now meeting strict international quality standards. While historical spikes to Italy signaled temporary global shortages, the consistent expansion into markets like Mauritius and the United States marks Pakistan’s permanent entry into the global industrial concentrate trade.

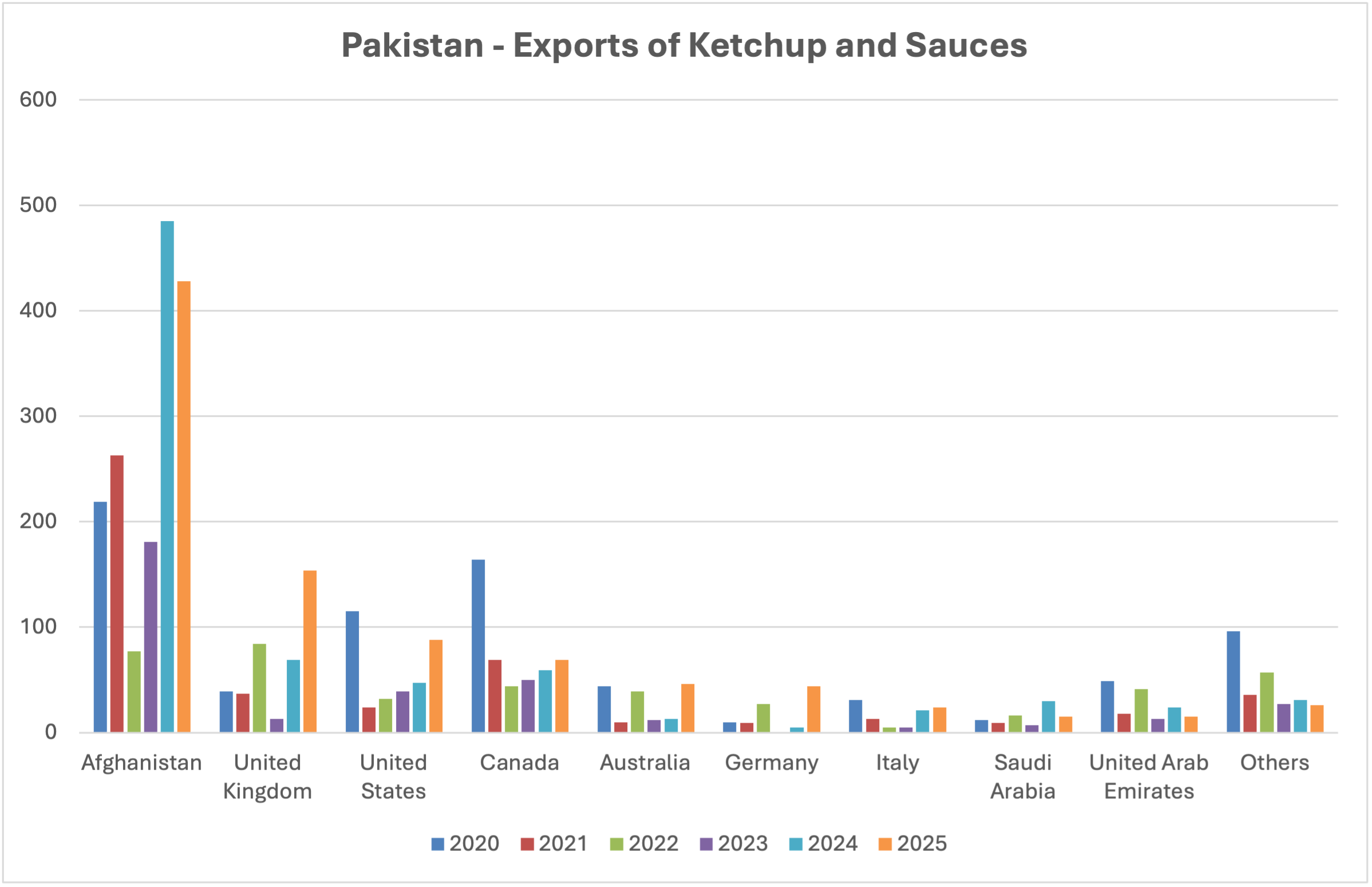

The export of finished ketchups and sauces highlights the strength of Pakistan’s manufacturing sector, with Afghanistan serving as the primary, albeit volatile, destination. Beyond regional trade, there is a clear upward trajectory in exports to the US, Canada, and Australia. Rising volumes in Germany and Saudi Arabia further confirm that Pakistani value-added products are successfully competing in diverse global retail and HORECA environments.

Sources: our conversation, Pakistan Bureau of Statistics (PBS), Agricultural Marketing Information Service (AMIS), Pakistan Tomato Industry Outlook 2022–2026, ReportLinker Research, Pakistan Business Council (PBC) “State of Agriculture 2024” report and TradeMap (ITC), SMEDA Industrial Feasibility Reports, National Foods, Shangrila, Shezan annual report, Mitchells, Volka Foods, TDM

{kind=link}