News

Italy: record export levels in 2016

Italy: record export levels in 2016

A balance of EUR 1.54 billion

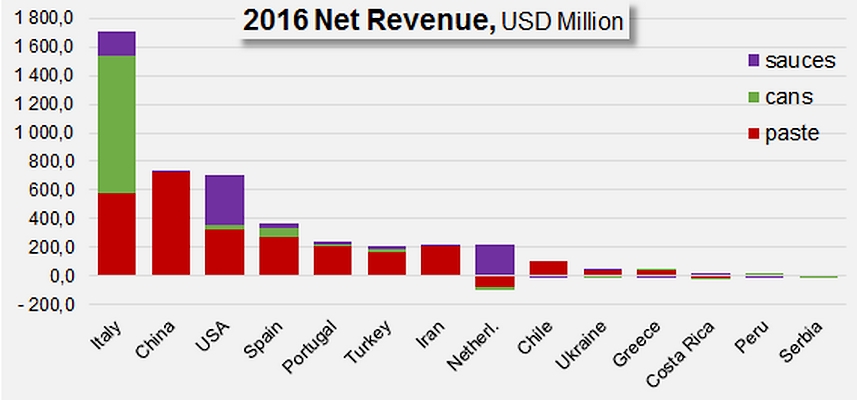

In 2016, the positive trade balance resulting from the trade in tomato products once again positioned Italy at the top of the world ranking of leading countries in this sector. Well ahead of its two main competitors (China with USD 740 million and the United States with USD 706 million), Italy exported USD 1.706 billion of tomato products. Spain and Portugal's foreign sales, ranked fourth and fifth of the Top 14 countries for tomato product exports, are respectively estimated at USD 372 million and USD 237 million (val. January-December 2016).

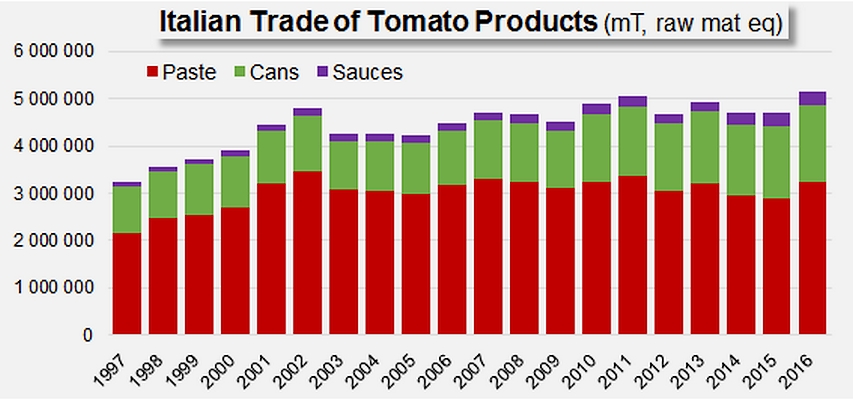

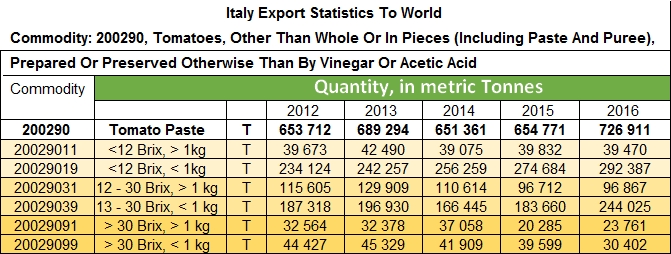

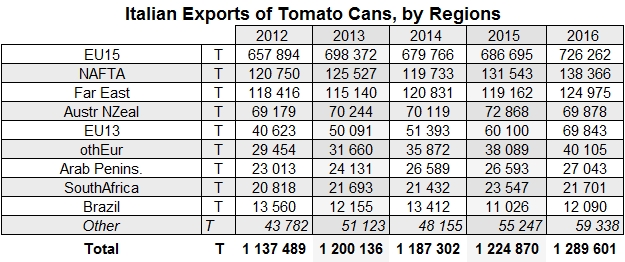

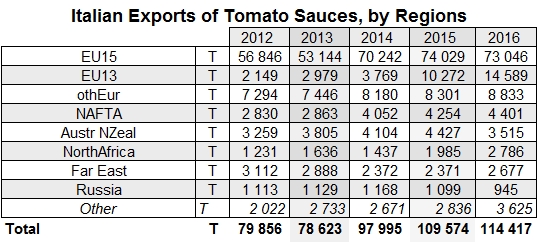

This excellent result of EUR 1.54 billion indicates a slight progression when reported in euros (+0.8%) compared to the result of 2015, but a more notable increase (approximately 3%) compared to the average of the three previous years (2013-2015), despite the tense commercial context that has penalized the value of products. The increase in quantities is indeed more considerable, and seems to indicate that the efforts made by the national representative bodies of the industry (ANICAV, IO Pomodoro Nord Italia, etc.) are starting to bear fruit. This recovery in foreign trade, which is also driven by the competitiveness of the European currency, could constitute a basis for relaunching Italian dynamics, which have run out of steam in recent years to a certain extent (see our special report in the June 2016 issue and the infographics at the end of the article). Last year, the Italian industry's foreign sales reached the record level of 727 000 metric tonnes (mT) of paste (finished products), which is 72 000 mT more than in 2015 (+11%) and 62 000 mT (9%) more than the average for the period running 2013-2015. Performances have also improved for the canned tomato category (1.29 million mT) with an increase of close on 65,000 mT compared to 2015 (+5%) and 85 000 mT compared to the period running 2013-2015 (+7%). Sauce exports (114 000 mT) have confirmed and extended the development initiated last year, with a progression of approximately 5 000 mT compared to 2015 (+4%), but more importantly a sharp increase of 20 000 mT (+20%) compared to the average of the three previous years.

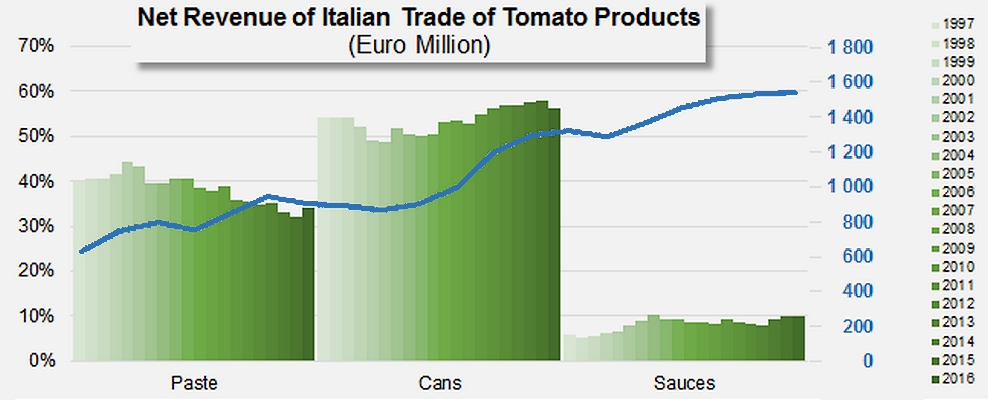

The 2016 Italian trade balance for tomato products recorded a positive balance of USD 1.7 billion (EUR 1.5 billion), 34% of which are the result of paste exports, 56% of canned tomato exports and 10% of sauces exports. For the record, in 2016, 98% of the revenue of the Chinese industry was generated by paste exports. As for the revenue of the US industry, half of it was generated by foreign sales of sauces and 46% by sales of pastes.

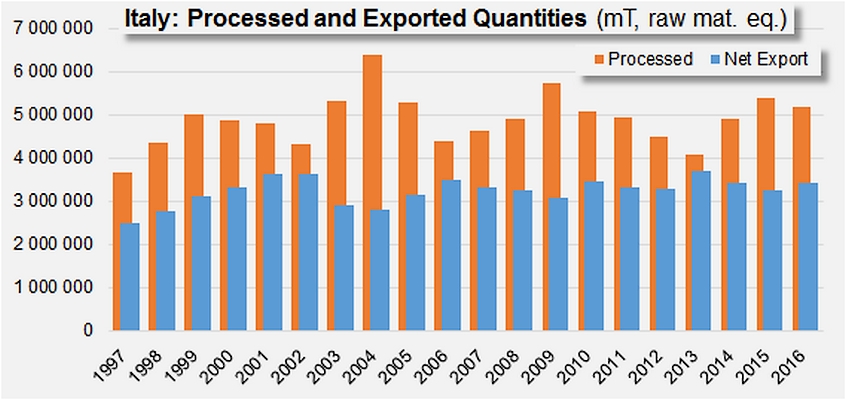

In total, Italian exports of tomato products absorbed in 2016 a record volume of 5.15 million tonnes (farm weight equivalent), almost 10% more than in 2015 (4.7 million mT, farm weight equivalent) and 8% more than over the period running 2013-2015. Taking account of imports, which are significant in the paste category and more specifically in the segment of products with a Brix higher than 30°, the year ended with the trade balance result recording a positive balance estimated at 3.42 million tonnes (farm weight equivalent). In other words, last year, the Italian industry dedicated two thirds of the volumes processed to foreign market outlets, the remainder being intended for domestic consumption.

| "Foreign markets are an important area of growth for our industry, which indicates that even in times of crisis, consumers choose quality," stated ANICAV President Antonio Ferraioli. "In an industry that is as focused on exports as ours, foreign sales still can balance out the stagnation of national consumption." |

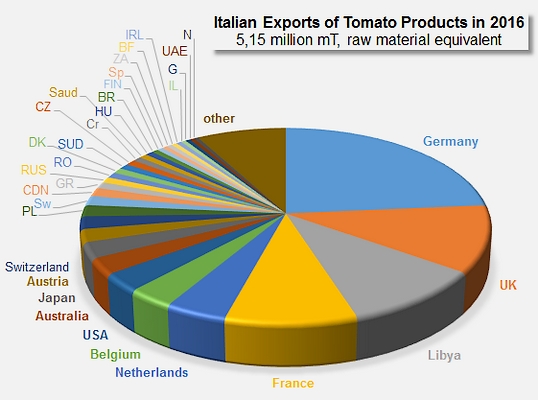

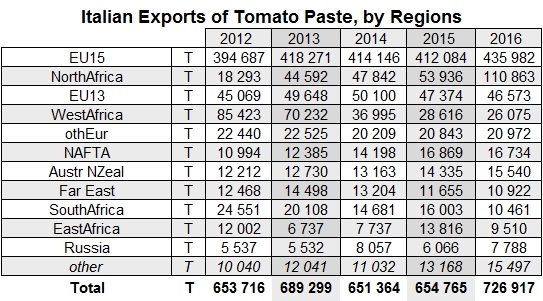

Germany (24% of total quantities exported (farm weight equivalent)) and the United Kingdom (11%) absorbed the equivalent of 1.7 million tonnes of raw tomatoes, for EUR 337 million and EUR 230 million respectively. Libya (10%) and France (9%) also feature among the main outlets for Italian products. These first four markets absorbed last year more than 54% of Italian exports. With the Netherlands, Belgium, the United States, Australia (see our article in the March issue of Tomato News), Japan, Austria and Switzerland, the proportion amounts to almost three quarters of the products exported by the Italian industry.

As the ANICAV pointed out in its comments on the results of 2016, peeled tomatoes – whole or in pieces – remain the most popular category sold abroad. This sector generates more than half of the net income produced by the tomato products trade and the quantities exported in 2016 amounted to 1.29 million mT (+5.3%), which is a considerable increase compared to the previous marketing years, though unfortunately, it did not see a corresponding increase in the value of products (EUR 869 million, -2.4% compared to the 890 million of 2015).

Most of the outlet regions participated in this increase of the trade flow, except for the Australian market (-5%, probably due to the anti-dumping measures instituted by Australian authorities) and the South African market (-11%, probably due to the big collapse of the South African rand).

The major progression recorded by the paste sector mainly stems from a strong growth in exports of 12-30°Brix products, in sharp contrast to the development of the growing trend in foreign sales of "low concentration" products observed in recent years. The quantities involved grew from 280 000 mT exported in 2015 to more than 340 000 mT exported in 2016 (+23%, whereas average variations over the past 20 years have generally been within a range of -7% to +13%).

A certain number of regions or countries noticeably increased the intensity of their trade flow in paste from Italy last year. The UE15 is one of these – and more specifically the United Kingdom – whereas countries of West Africa – particularly Nigeria and Guinea – have considerably reduced their purchases of Italian paste. The most notable variation is the one recorded for exports to Libya, which grew from 48 000 mT in 2015 to more than 105 000 mT last year.

The sharp increase that has been observed in recent years for "low concentration" products, at the expense of other categories of lesser values, opened the way in 2016 to a sudden increase in the 12-30°Brix category.

The development of sauce exports, which is limited (+4%) compared to the 2015 result, has however been decisive compared to the average of the three previous years: the 19 000 mT increase recorded last year was largely the result of the growth in Polish and Czech purchases of Italian sauces, and, to a lesser extent, to purchases from France, the Netherlands and Israel.

Less raw material, more value

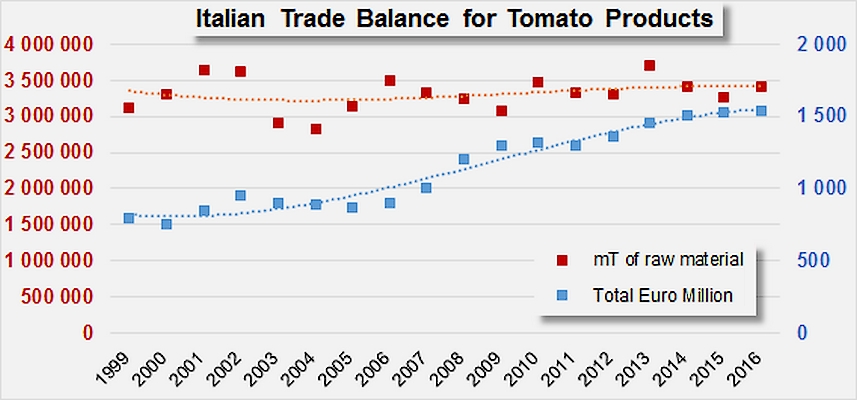

Over the years, the annual turnover generated by Italian exports of tomato pastes has progressively increased, despite the toughening of economic and commercial contexts around the world, and despite the fairly limited growth in the quantities of raw materials involved in these trade flows. Over the past 18 years, the trade balance has recorded an average annual positive result of 3.3 million mT (farm weight equivalent), with a lower end level of 2.8 million mT in 2004 and a higher end level of 3.7 million mT in 2013. At the same time, despite the difficulties linked to competition and to the consequences of the economic crisis, the value of each of these tonnes of products has grown, from an indicative level of EUR 230 /mT in 2000 to approximately EUR 450 /mT in 2016 (for all product categories, conditionings and contractual considerations). In the final count, between 1997 and 2016, the volumes of raw tomatoes involved in net export movements have progressed at a fairly slow annual rate, close to 1.1%, whereas the "value" of each of the tonnes shipped has increased at an average rate of 3.3%.

The volumes of raw materials mobilized by exports have evolved only slightly, whereas their value has progressed at a relatively consistent rate.

These dynamics are the result of an increase in the price of the finished products exported, but also and more importantly of a strategic commercial reorientation effort, which has consisted in promoting foreign sales of more elaborate products or at the very least of higher value products, which is the case of canned tomatoes on the one hand and of "low concentration" products on the other.

The importance of these categories and product segments on the Italian products export markets has increased regularly in recent years, both in terms of quantity and in economic terms. Since 2002-2003, new trends have appeared in export patterns, which have mainly impacted the pastes and canned tomato sectors.

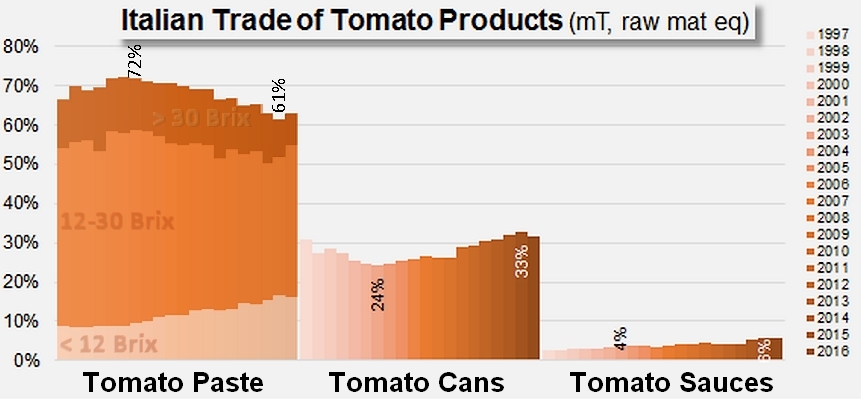

- Almost independently of the annual variations linked to markets uncertainties, paste exports have taken on an increasing importance within the Italian trade balance for tomato products, growing from 24% of the total exported in 2002 to 33% in 2015 (expressed in farm weight equivalent).

- Mechanically, the importance of pastes has sharply declined in proportion to the total (from 72% in 2002 to 61% of the total in 2015), along with a redistribution observed within the paste category:

- very progressively, foreign sales of "low concentration" products (less than 12°Brix) have accounted for an increasingly large proportion of total paste exports, at the expense of the 12-30°Brix segment and the more than 30°Brix segment.

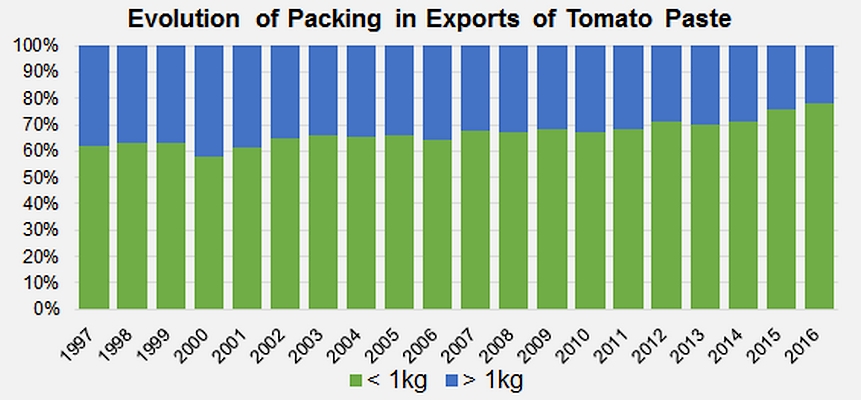

- Along with these basic trends, the Italian industry has developed the form of its exports by increasingly promoting catering-sized conditionings and products intended for retail sale, particularly in the paste category (60% of foreign sales in 1997, close on 80% in 2015).

The joint effects of these industrial and commercial patterns have driven the development of the value of exported products, by enhancing the profitability of each tonne of tomatoes processed and exported, with continual increase in production volume. In the final count, this growth pattern has helped the Italian industry to go from a positive trade balance of 3.64 million tonnes (farm weight equivalent) that generated EUR 846 million in 2001 to a trade balance of 3.42 million tonnes that generated EUR 1.54 million in 2016.

(See also our article on US "border adjustment tax" project).

Some complementary data

The 2016 result contrasts sharply with the results of the past three or four years, and could be the starting points of a recovery in the dynamics of Italian exports.

The progression of the turnover generated by exports is mainly based on the dynamics of the canned tomato category. Contrary to the trend observed since the beginning of the 2000s, the 2016 result for canned tomatoes indicates a major recovery of revenue from paste exports along with a slight decrease for canned products. Sauces account for approximately 10% of the overall results, a regular but limited increase.

The quantities exported (expressed in farm weight equivalent) have varied according to market conditions, but have progressed relatively little since 2002-2003. They absorbed 66% of the processed volumes in 2016.

Over the past 20 years, Italian industry exports have increasingly used catering or retail packagings, whereas the proportion of industrial conditionings has tended to decrease. The impact of this shift on the turnover generated by foreign sales of tomato pastes has been considerable.

The results tables for each category over the past five years are available in the appendices presented at the end of the web version of this article.

Appendices/Annexes

{kind=link}