News

Europe’s Position in the Global Tomato Paste Trade

The quantities of tomato paste traded globally over the last ten years have grown at an average annual rate of 1.6%. Chinese and American products appear to be the main beneficiaries of the upturn, while European products are holding their own, while shifting more toward the domestic market.

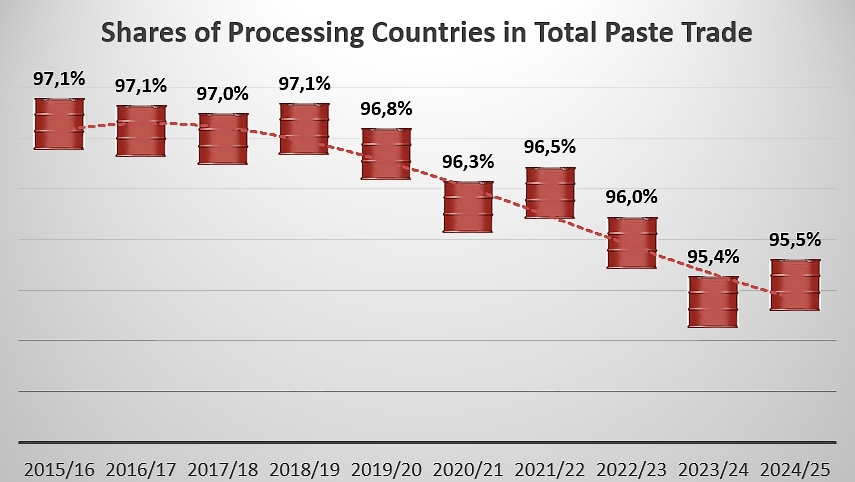

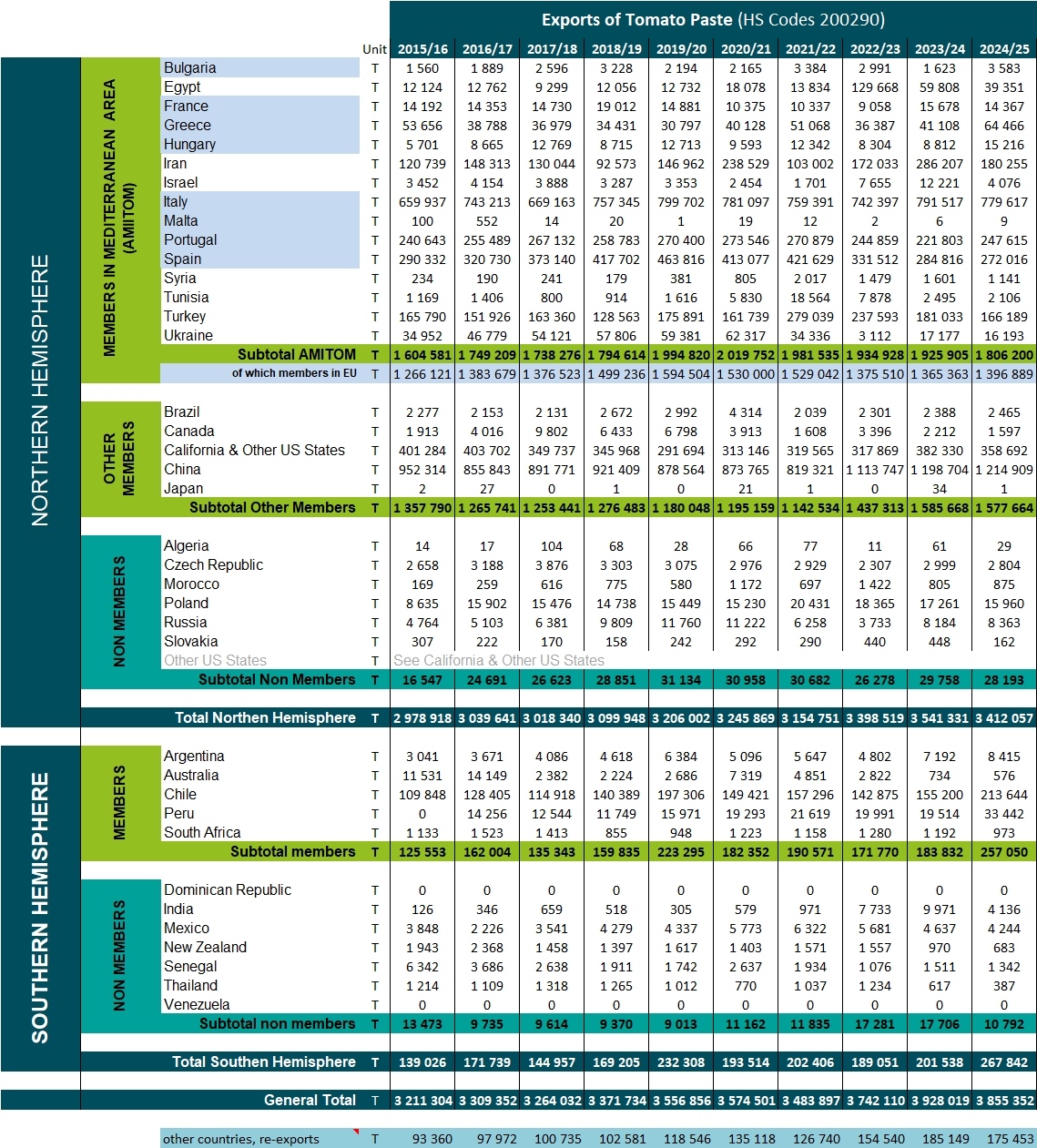

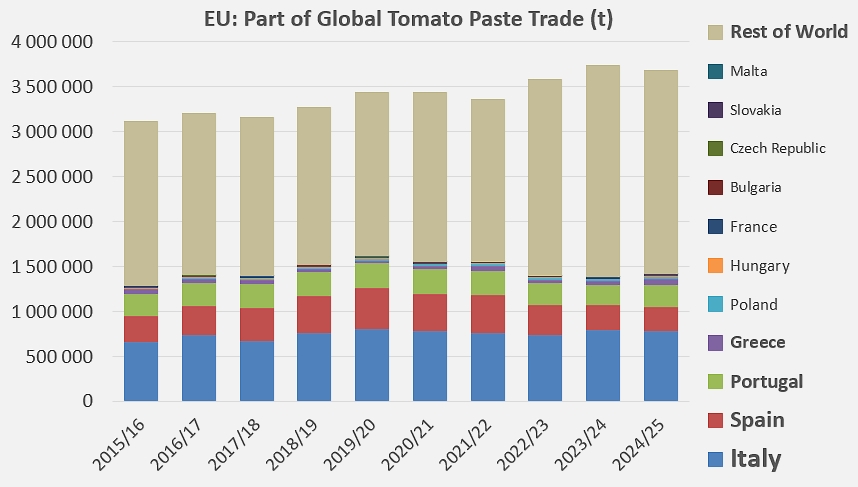

The forty tomato processing countries regularly monitored by the World Processing Tomato Council (WPTC) account for 96 to 97% of the annual tomato paste trade (HS codes 200290). Over the last three marketing years, the total quantities they mobilized amounted to nearly 3.674 million tonnes (t) of finished products, a significant increase (16%) compared to the 3.166 million t averaged over the period 2015/2016-2017/2018. Despite this sharp increase, the contribution of processing countries to global trade has been eroding in recent years, from more than 97% of total exported quantities at the beginning of the last decade to just over 95.5% over the last three years.

In 2024/2025, the total quantities exported by all reporting countries (sourced from Trade Data Monitor) represented 3.86 million tonnes of finished products; of this total, only 3.68 million tonnes (95.5%) originated in one of the forty producing and processing countries listed by the WPTC: the remaining quantities can be attributed to other countries or considered re-exports from non-processing countries.

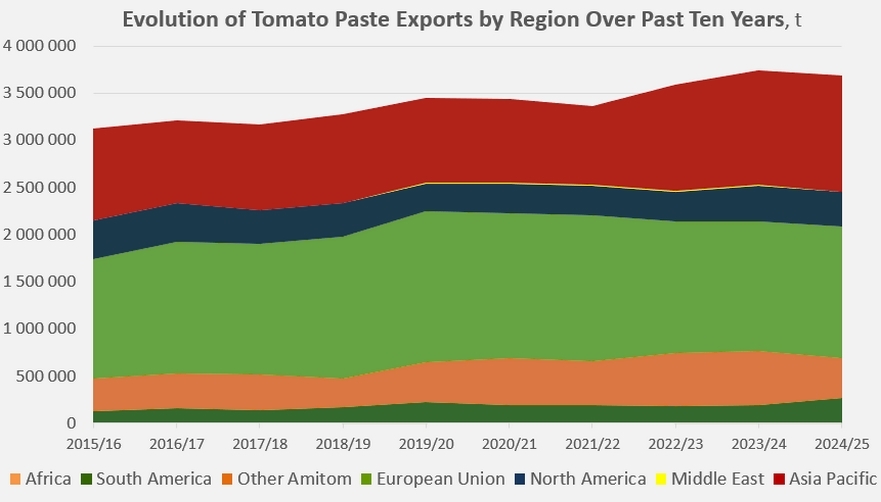

With this in mind, Tomato News has drawn a parallel between the national and regional production/processing figures collected by the WPTC (see additional information at the end of the article) and the quantities exported by these same countries and regions; the differences between the graphs clearly illustrate the domestic and/or export vocations of the major production and trade areas identified by the WPTC.

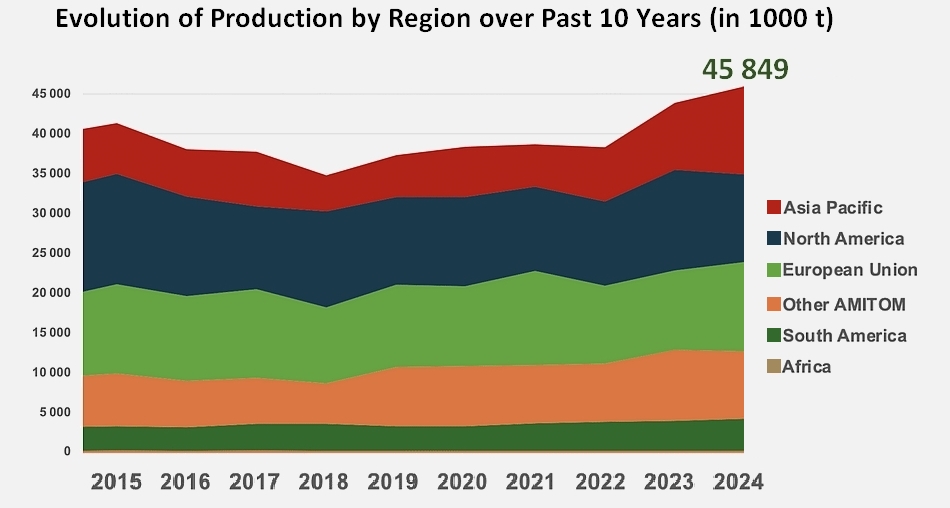

Thus, the processing activity of China, the main player in the Asia-Pacific region, appears clearly geared towards foreign markets, while the primary destination of North American products appears, on the contrary, to be domestic. Between the two, the European sector in the broadest sense of the term (eleven countries) maintains strong production activity focused both on EU and/or geographically nearby markets and on foreign markets.

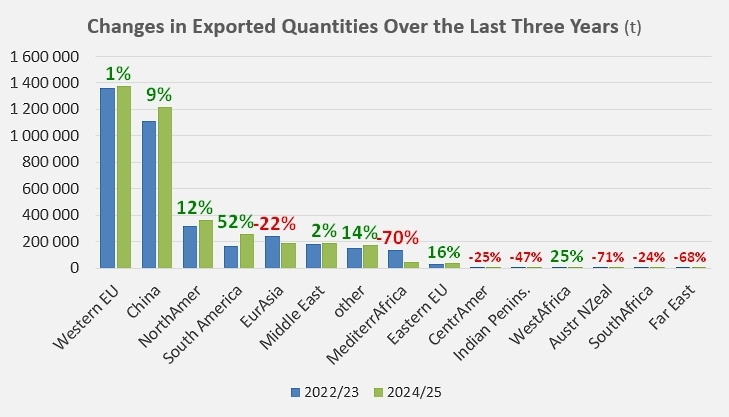

Evolution over three years

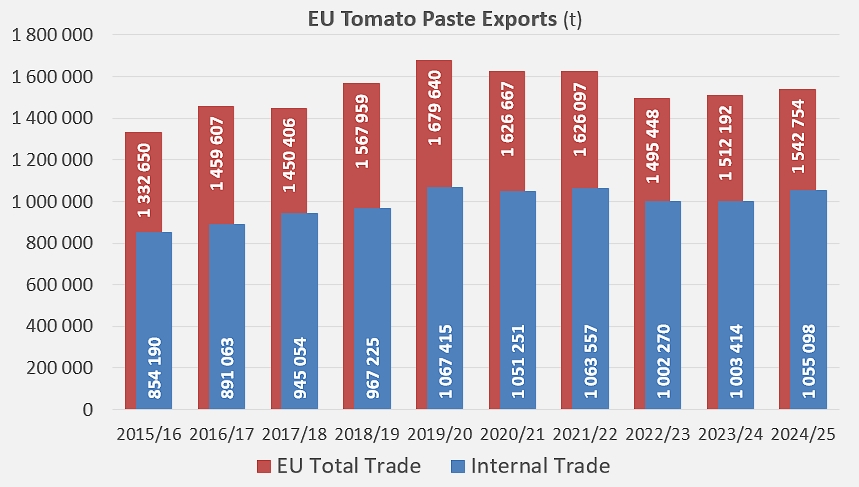

In a global market marked by a significant increase in demand, the three marketing years following the end of the Covid health crisis have not brought about any fundamental changes in the hierarchy of tomato paste exports. With 1.38 million tonnes exported in 2024/2025, the Western EU (Italy, Spain, Portugal, etc.) retained its position as the world’s leading exporting region of tomato paste and slightly improved its performance (+1%). Over the same period, from 2022/2023 to 2024/2025, China remained the main challenger in the sector and saw its external results increase significantly (+9%), reaching 1.215 million tonnes last year. Although much smaller in volume, North American (California, Canada) and South American (Chile, etc.) products also increased their exported quantities, reaching 360,000 t and 258,000 t respectively, increasing by 12% and 52% over three years.

Conversely, the period saw a number of declines in annual export rates, particularly from Turkey (-30%) and Egypt (-70%).

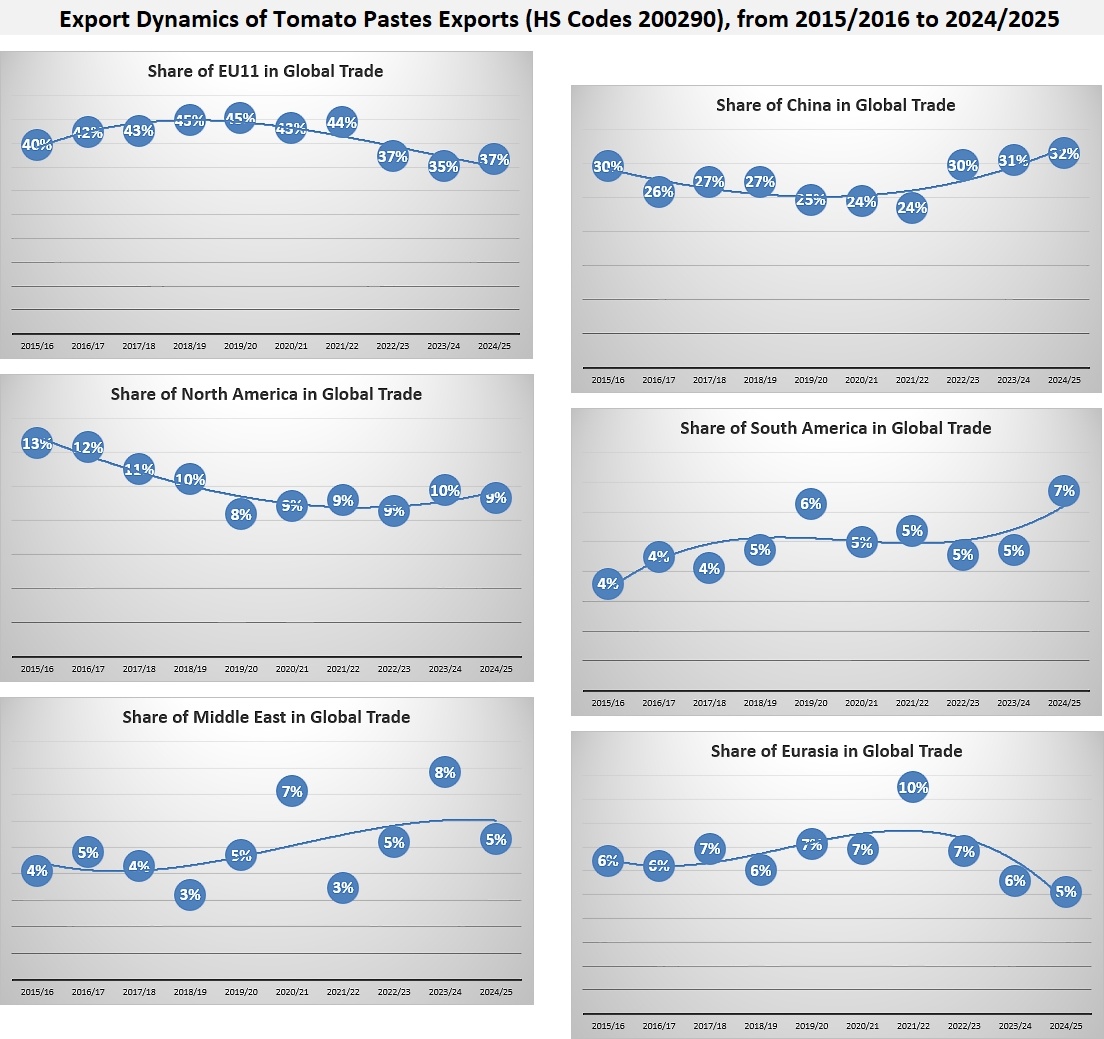

The share of different processing areas

These different dynamics are reflected in changes in the distribution of global market shares among the major sectors in the sector; the European industry’s exposure to climatic hazards, but also and above all to the economic, political, and social difficulties of recent years, have visibly contributed to a relative weakening of the region’s trade positions, whose influence has declined from 45% of the global market at the best of the decade, in 2019/2020, just before the outbreak of the pandemic, to less than 37% in the last marketing year. At the same time, the context of increasing volumes traded globally has clearly benefited the Chinese industry, whose share of the global tomato paste market has increased, despite embargo measures implemented in a number of countries, from 25% at the lowest of the decade to nearly 32% in the 2024/2025 marketing year.

The third largest global player in terms of quantities, the United States has struggled in recent years to consolidate a share of approximately 9% of the global market, which reached 13% at the beginning of the decade. The competing sectors of South America (Chile, Peru) and the Middle East (Iran) display much less regular dynamics than those of the three leading basins; despite greater exposure to fluctuations in the global economic and trade context, the decade’s results are rather positive for these regions, which represented 3.6% and 4.1% of the global market respectively in 2015/2016. In 2024/2025, South American exports will have supplied nearly 7% of global supplies, while exports from Middle Eastern sectors will amount to more than 5% of the global total.

Finally, in addition to Ukrainian products, which are still facing the consequences of the conflict with Russia, the performance of the Eurasia region remains essentially driven by Turkish activity; after a sharp increase during the Covid health crisis, it has recorded a sharp decline on a global scale, which has positioned the region at around 5% of the global total during the last marketing year.

Focus on the EU

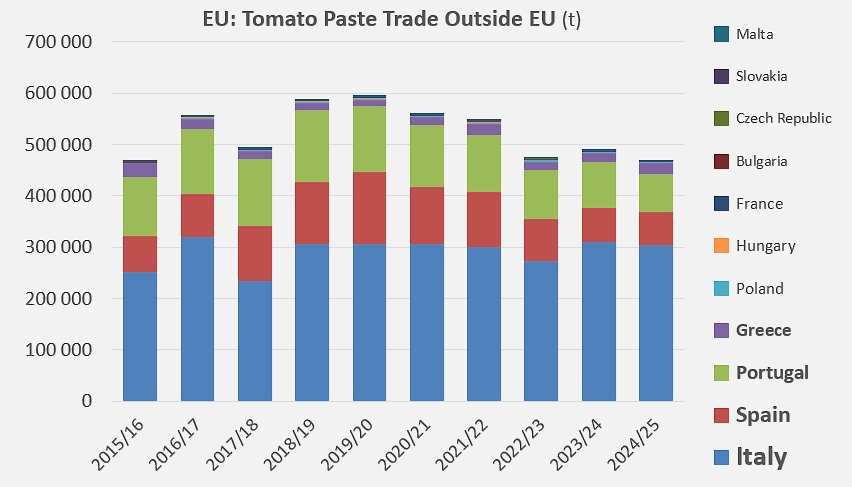

The eleven EU processing countries accounted for more than 36% of global trade over the past three years (see additional information at the end of the article); the total quantities mobilized, very close to 1.4 million tonnes of finished products, came mainly from Italy (771,000 tonnes on average over the past three years) and, to a lesser extent, from Spain (296,000 tonnes) and Portugal (238,000 tonnes).

However, only a portion of these quantities of tomato paste, estimated at 31% of European external sales, is intended for export outside the EU, representing approximately 477,000 tonnes of finished products on average over the past three years. In this context, it is important to note that, according to official trade data, this share destined for the global market, primarily accounted for by the three main European processing countries, has declined significantly over the last five or six fiscal years: the average quantities mobilized between 2022 and 2025 for markets outside the European Community have returned to a level roughly equivalent to those recorded in 2015/2016 or 2017/2018.

In fact, European production and processing activity is primarily oriented towards the domestic market, the world’s largest in terms of quantity and value.

In a global market that has been growing again since the health crisis, but which has been faced in recent years with a dynamic of overproduction and increasing constraints of all kinds, increasingly intense competition is prompting a number of European industries to rely on their domestic markets; what appeared at best to be an uncertain trend before the outbreak of the pandemic in March 2020 now reflects a reorientation of commercial activity towards known historical markets, less costly in terms of transport, closer in terms of regulations and more accessible in terms of customs duties.

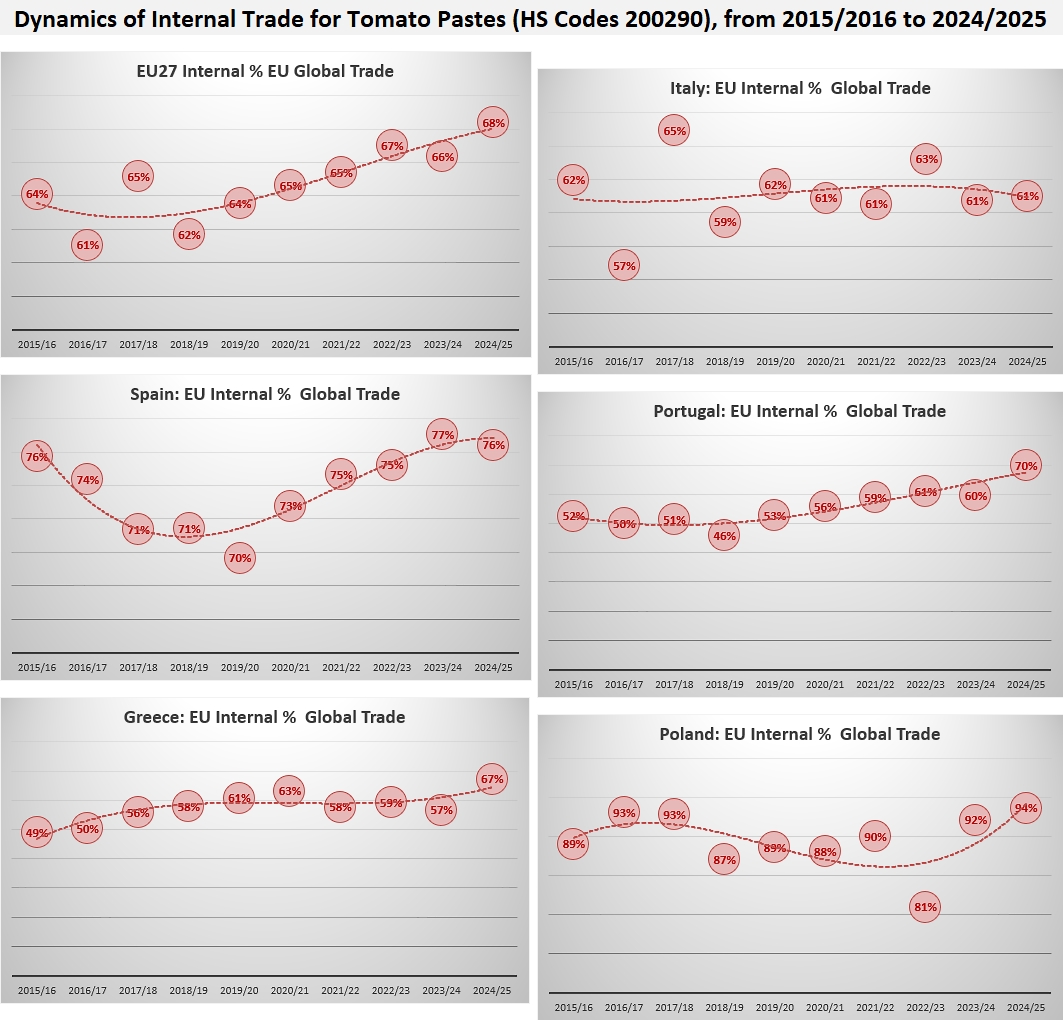

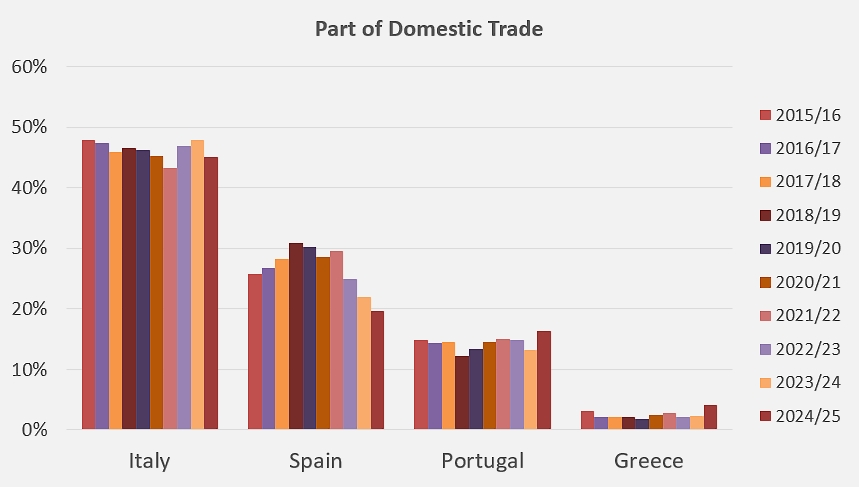

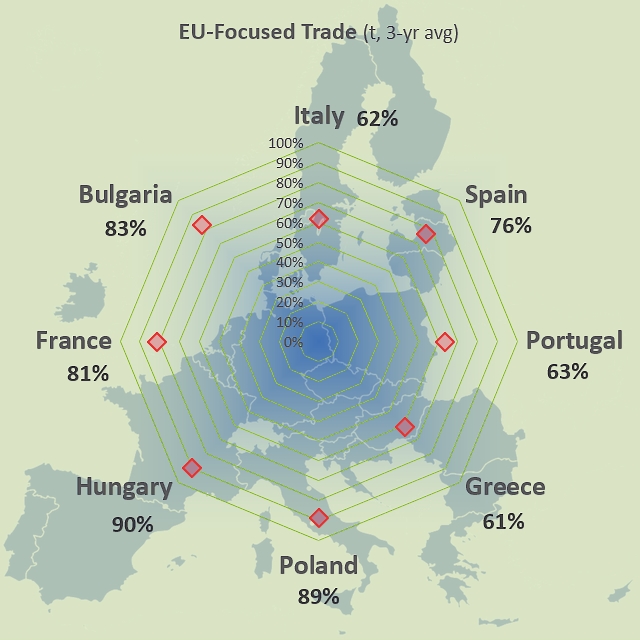

For all EU27 countries, the fraction of activity reserved for the domestic market has increased significantly over the last seven or eight marketing years: in 2018/2019, the European domestic market accounted for around 62% of exported quantities; in 2024/2025, this figure rose to 68%. But within this regional trend, national dynamics reveal stark contrasts between the different industries: while Italy has devoted a roughly stable or slightly increasing proportion of its products to the European domestic market in recent years, effectively offsetting the more EU-oriented orientations of neighboring sectors, Spanish, Portuguese, and Greek industries have seen their external activities clearly refocus on European customers. In the case of Spanish products, more than 76% of the quantities were delivered within the EU in 2024/225, compared to 70% in 2019/2020; the Portuguese processing industry exported almost 70% of its tomato paste to EU markets, compared with only 46% in 2018/2019; for Greek products, the figure rose to 67%, compared with 49% in 2015/2016. For other significant sectors, the figures range from 80 to 90% of activity.

These dynamics and performances, described for the period ending with the close of the 2024/2025 marketing year, will likely be profoundly reshaped by market conditions redefined by the results of the season just ending: the drastic reduction in quantities processed in China in 2025, the very exceptional season achieved this year in California, the emergence of Iran into a broader commercial sphere, and the consolidation of Chilean positions on the international market are all elements likely to alter the trade balances of the global tomato paste market: we will keep Tomato News readers informed of their developments.

Some complementary data

Table of global tomato paste exports, prepared in parallel with the WPTC processing table.

Evolution of the regional components of global production/processing of processing tomatoes.

Contribution of European sectors to total global exports of tomato paste.

Contribution of the main European sectors to supplying the European tomato paste market.

Proportion of quantities processed by each EU country destined for the European domestic market.

Sources: TDM, WPTC

{kind=link}