News

Chile: exports rise sharply in 2025

In a global sector largely dominated by Northern Hemisphere countries, Chile is not the only processing country in the Southern Hemisphere, but it is by far the largest, operating out of season. The volumes processed have represented more than 40% of Southern Hemisphere activity over the last five years, and the latest WPTC forecasts credit Chile with processing intentions of approximately 1.3 million tons for the 2026 season.

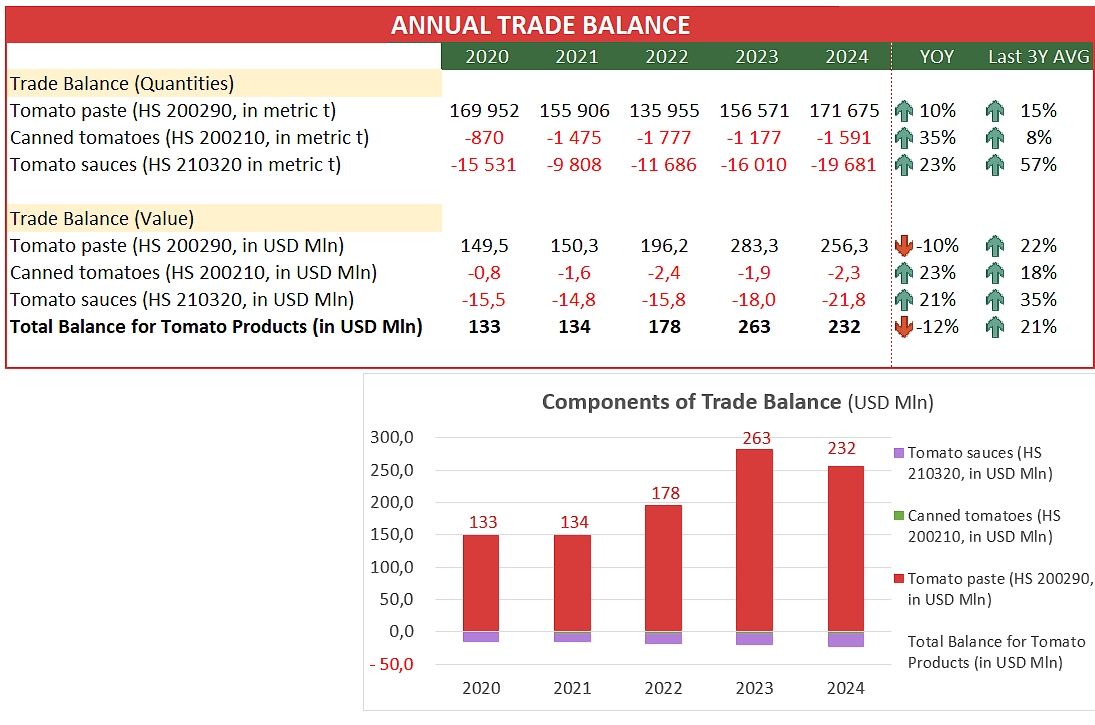

The Chilean trade surplus in tomato derivatives is built exclusively on exports of tomato concentrate (HS code 200290): in 2024, the total surplus amounted to USD 232 million, down USD 31 million (-12%) compared to 2023, but still 21% higher than the 2021-2023 average. Exports of tomato concentrate generated a surplus of approximately USD 256 million in 2024, significantly higher than the average of the three preceding years, but showing a decrease of USD 17 million (-10%) compared to 2023. This decline occurred even though the quantities exported in 2024 were 15,000 tonnes (+10%) higher than in 2023 and 22,000 tonnes higher than the average for the period 2021-2023.

Chile is not an exporter of canned tomatoes (HS codes 200210) and imports only small quantities. The annual trade deficit in this sector has been around 1,400 tonnes and USD 1.8 million over the last five years; these two indicators demonstrate a steady widening of the canned goods trade deficit.

The widening trade deficit in sauces and ketchup (HS code 210320) is even more pronounced, with imports in 2024 approaching 20,000 tons, significantly higher than in 2023 (16,000 tons) and the three preceding years (12,500 tons on average). The change in value is almost as dramatic, with a deficit of nearly USD 22 million last year, compared to “only” USD 18 million in 2023 and just USD 16 million over the 2021-2023 period.

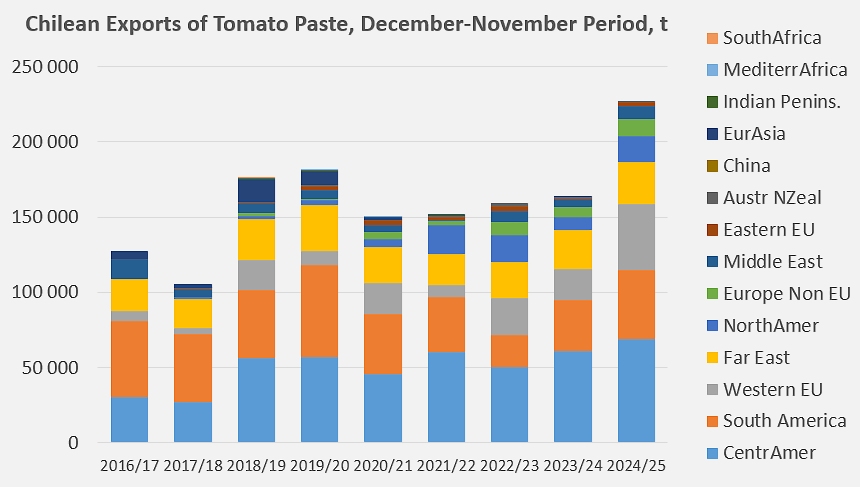

Over the twelve-month period ending in November 2025, Chile’s trade balance for tomato paste shows strong growth. A dozen or so long-standing customer countries, spread across five regions, accounted for over 77% of Chile’s export sales of concentrates in 2024, and, with the exception of Colombia (+1%), all showed very significant increases.

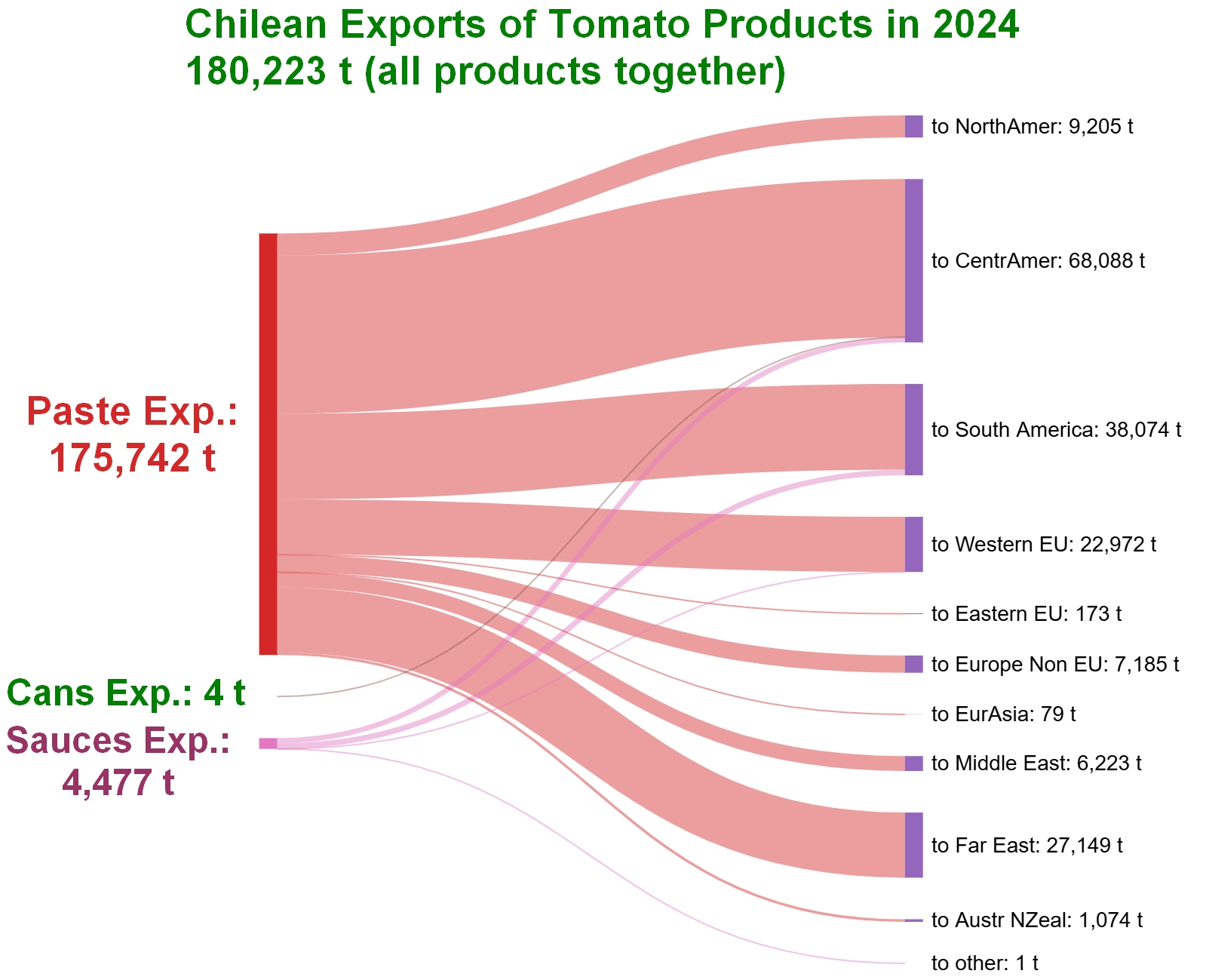

The majority of the Chilean sector’s markets are located in Central and Latin America. Between December 2024 and November 2025, these two regions received half of Chile’s exports (just over 115,000 tons of concentrates). Deliveries increased by 12% to Costa Rica, 26% to Mexico, 16% to Venezuela, and 32% to Guatemala, for a total of 58,000 tons out of the 69,000 tons received in the region.

In Argentina, purchases of Chilean concentrates jumped by 61%, while the quantities delivered to Brazil and Uruguay increased by 16% and 10%, respectively; these three countries received 41,000 tons out of the 46,000 tons delivered to this region.

Nearly 24,000 tons of Chilean concentrates were exported to Japan, 13% more than in 2023; with nearly 15,000 tons in In 2024, US purchases increased by more than 90% compared to the average volumes of the previous five years. Finally, it is important to note the significant increases in deliveries to Italy (from 8,300 tons in 2023 to 15,900 tons last year), Germany (from 9,100 tons to 16,500 tons), the Netherlands, Portugal, and other countries.

In its recent crop status report, the WPTC mentions that “Chilean exports reached a good volume in 2025 (January-December) with 221,000 tons compared with 174,000 tons in 2024.”

Some complementary data:

Evolution of processed quantities in Chile

Composition of Chilean exports of tomato derivatives in 2024

Sources: TDM, WPTC

{kind=link}