News

California: breaking through the glass ceiling of profitability

California: breaking through the glass ceiling of profitability

While price negotiations for the raw materials of the 2017 tomato season in California were still ongoing, the Agricultural Issues Center (AIC) of the University of California published an extremely detailed set of data regarding the composition of operational costs and profitability for processing tomato crops using sub-surface drip-irrigation in the Sacramento Valley (the upper region of Central Valley) and the northern area of the Delta – in effect, from Stockton in the south to Redding in the north.

While price negotiations for the raw materials of the 2017 tomato season in California were still ongoing, the Agricultural Issues Center (AIC) of the University of California published an extremely detailed set of data regarding the composition of operational costs and profitability for processing tomato crops using sub-surface drip-irrigation in the Sacramento Valley (the upper region of Central Valley) and the northern area of the Delta – in effect, from Stockton in the south to Redding in the north.

The authors of this exceptional study, of which a previous version had already been put together in the 2014, insist on the fact that their work makes use of a model and cannot be considered representative of all the situations encountered: so the results obtained are "indicative" and do not describe an absolute reality, nor do they necessarily express the opinion of the authors. For this study, the researchers –including some internationally acknowledged experts in the field like Gene Miyao and Brenda Aegerter – imagined a virtual farm: "The hypothetical field and row-crop farm consists of 3 500 non-contiguous acres of rented land at 12% of gross tomato revenue for this budget. Tomatoes are transplanted on 1 000 acres, all sub-surface drip irrigated as two-thirds of the local tomato acreage is estimated to be sub-surface drip irrigated. Twenty-five hundred acres are planted to other rotational crops including alfalfa hay, field corn, safflower, sunflower and/or wheat, etc. The grower also owns various farm investments including a shop and an equipment yard. In this report, practices completed on less than 100% of the acres are denoted as a percentage of the total tomato crop acreage.”

Production issues addressed in the study include current costs for production, material inputs, plus cash and non-cash overheads. Analyses show profits over a range of prices and yields, plus monthly cash costs, costs and returns per acre, business and investment overhead costs, hourly equipment costs, and whole farm annual equipment costs.

Production issues addressed in the study include current costs for production, material inputs, plus cash and non-cash overheads. Analyses show profits over a range of prices and yields, plus monthly cash costs, costs and returns per acre, business and investment overhead costs, hourly equipment costs, and whole farm annual equipment costs.

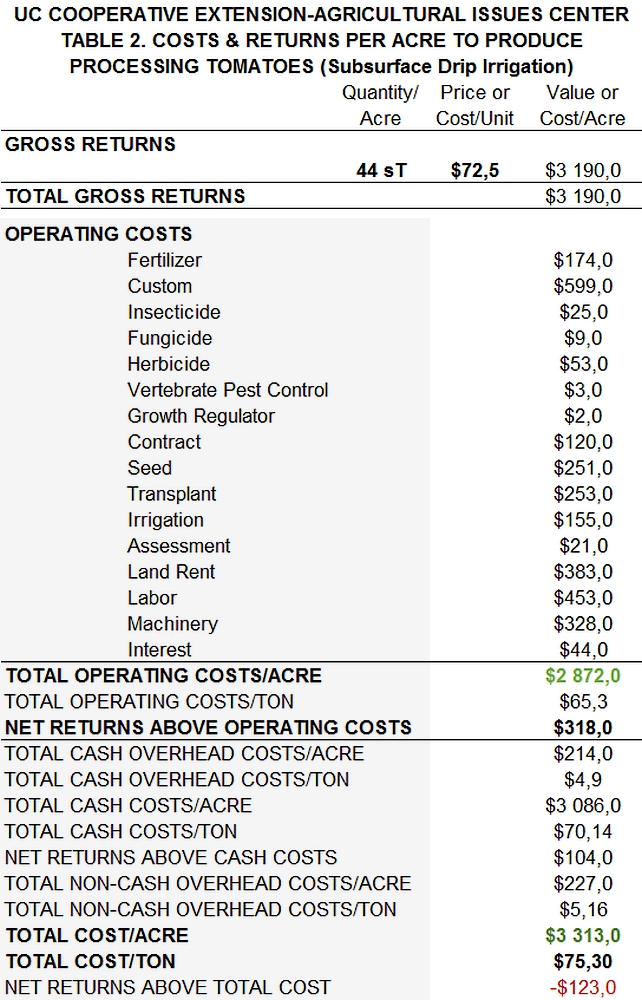

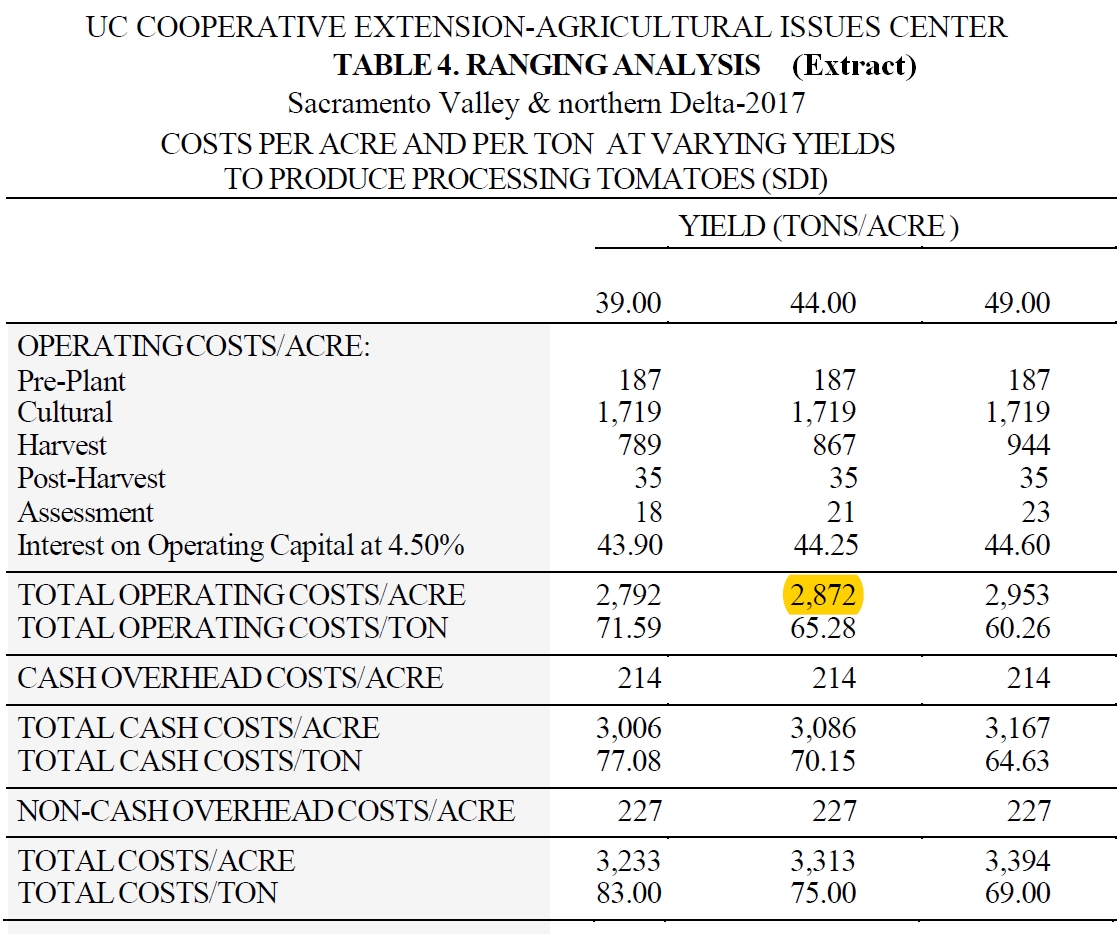

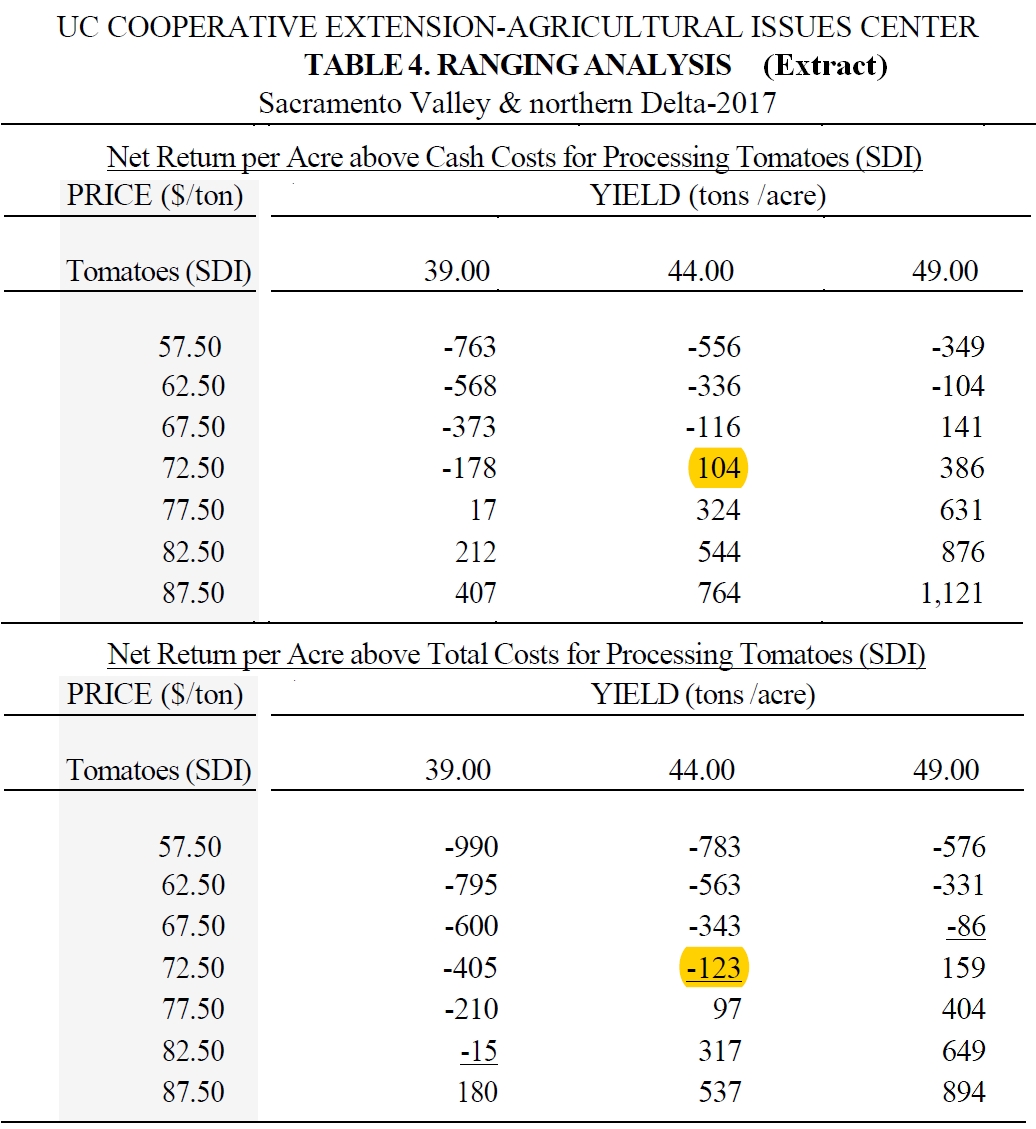

Average yields from processing tomato crops for the counties concerned (Colusa, Sacramento, Solano, Sutter, Yolo, San Joaquin, etc.) range from 39.25 short tonnes per acre (sT/acre) (88 mT/ha) to 46.3 sT/acre (104 mT/ha). For the study, the authors took account of a yield of 44 sT/acre (about 98.6 metric tonnes per hectare), which is lower than the forecast average productivity for 2017, and valued the quantities at the price negotiated last year with processors (USD 72.5 /sT, or about EUR 75 /mT*).

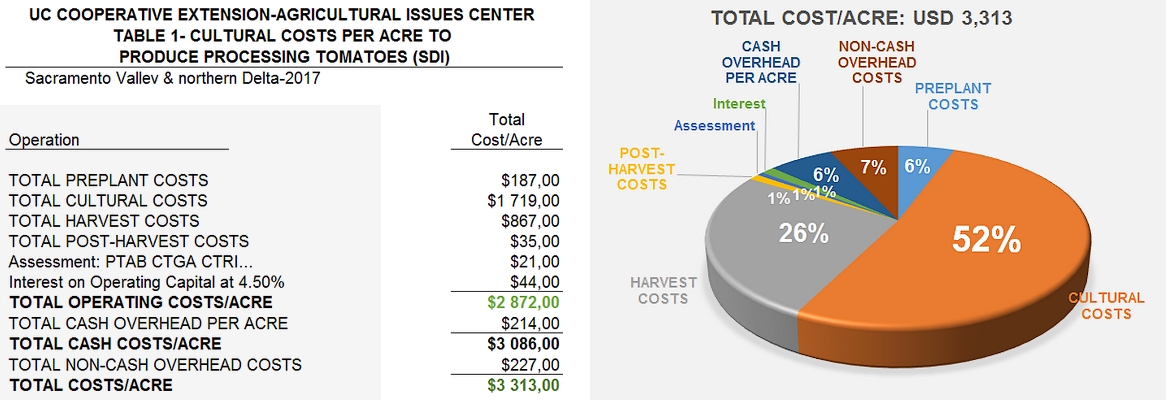

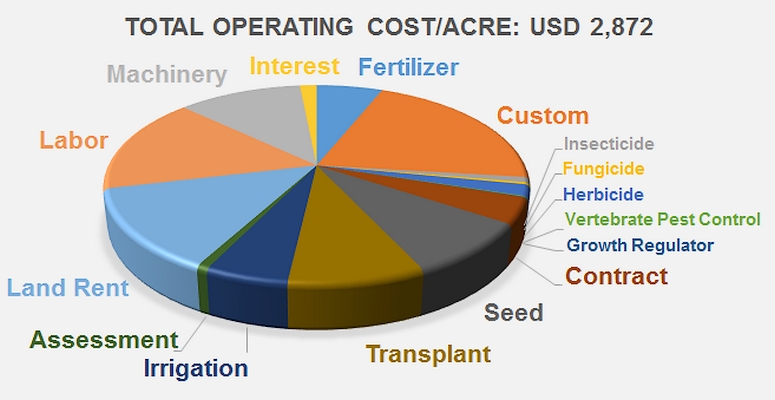

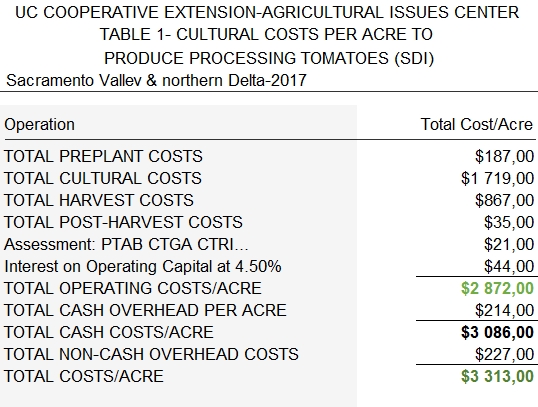

In these conditions, operating costs alone amount to USD 2 872, which is already 90% of the mean value of the harvest, estimated at USD 3 190. More than half of these costs are linked to crop management operations and one quarter to harvest costs, while the costs of field preparation and post-harvest care only represent a relatively minimal proportion of total costs (7%).

Taking account of overheads that are not proportional to the size of the crop, the total direct and indirect costs of production in 2017 are valued by the authors of this study at USD 3 313 /acre (equivalent to EUR 7 700 /ha). This figure is considerably higher than the forecast mean cost (USD 3 190 /acre), but according to the authors themselves, the model cannot give account of all situations. It does however demonstrate the extreme conditions that impact production operations, as well as the very high level of exposure of farmers' revenue to all kinds of hazards (weather, plant health problems, financial obstacles, agronomic and commercial issues, etc.).

For an investment of USD 3 086 /acre, the USD 3 190 revenue would only leave slightly more than USD 100 /acre for the grower, which is a profitability that barely clears 3%, explains Gene Miyao. Margins are indeed very tight, particularly taking account of the fact that this business – growing processing tomatoes – is highly exposed to various hazards, most notably with the late varieties that can suffer heavy losses due to end-of-summer rains, which increases expenditure.

Setting aside any interpretation or comment regarding the obvious and delicate proximity of this study's results with the price offers put forward in January and in March by Californian processors, the analysis of these agricultural experts objectively identifies three points of leverage that could allow growers to "break through the glass ceiling" of low profitability: improve yields in order to spread out the costs and reduce their impact per unit of surface or volume; reduce costs while ensuring that productivity and quality do not suffer; use negotiation to obtain a better valuation of products.

In any case, it is important to note that the researchers based the study on a set of precautionary figures. Among other parameters, the yields – which are particularly influential in the profitability of the business – are expected to reach, according to the USDA, 49.4 sT/acre (more than 110 mT/ha) this year. If such an agricultural yield is achieved, it would bring the point of balance for operating costs, in other words the price from which growing processing tomatoes would start being profitable in 2017, to approximately USD 69 /sT.

For more information and details:

https://coststudies.ucdavis.edu/archived/commodity/tomatoes/

https://coststudies.ucdavis.edu/current/commodity/tomatoes/

Some complementary data

(*: 1 USD=0.94455 euros, val. March 2017)

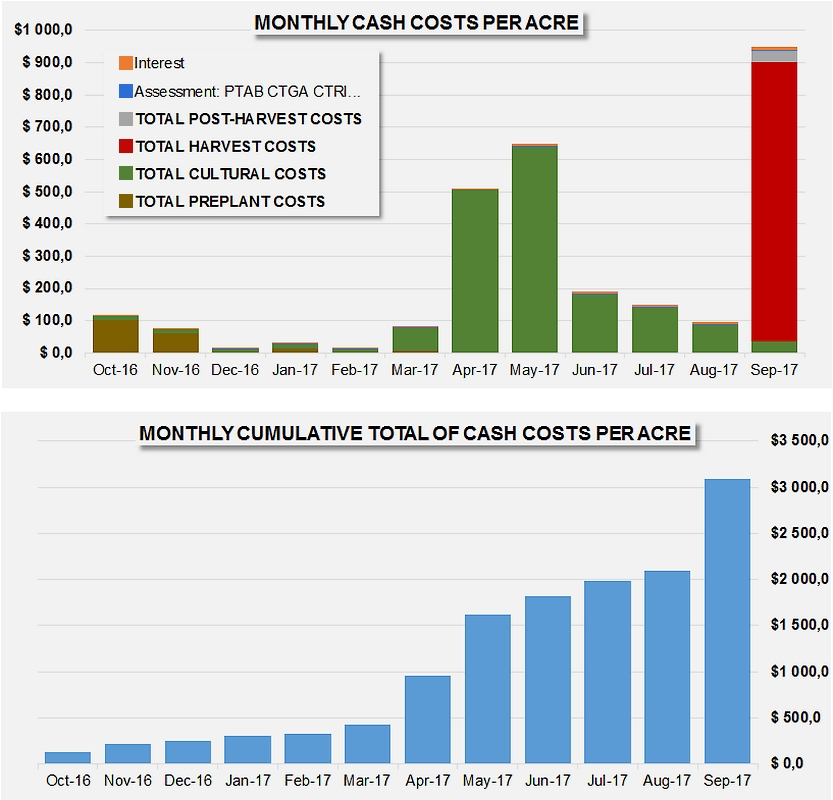

Model of the monthly chronological evolution of the components of production costs for processing tomatoes in 2017 in California

Appendices/Annexes

UC_Davis_Cost-Study_2017

{kind=link}