News

Euromonitor Global Market Report on Processed Tomatoes

Tomato News has acquired a Global Market Report on Processed Tomatoes from Euromonitor International. While the full, comprehensive findings will be presented during the WPTC Congress this June in Monterey and included in the 2026 Tomato News Yearbook, we will be providing our readers with a series of concise analytical insights in the coming weeks.

To begin this series, we are pleased to share the report’s Executive Summary.

- Consumers prioritise affordability, versatility and health, redefining winning processed tomato formats

Versatile tomato bases outperform as consumers prioritise affordability:

Tomato pastes and purées show stronger resilience than finished products, benefiting from affordability, versatility and frequent usage. Consumers increasingly rely on these formats to stretch meals amid cost pressures and sustained home‑cooking habits.

Private label structurally constrains branded pricing:

Private label penetration continues to intensify, especially in mature markets, capping branded price increases. Improved quality perceptions and premium private label tiers force brands to defend value through differentiation rather than scale or promotion.

Health positioning is now a baseline requirement, not a premium lever:

Clean‑label, reduced sugar and additive‑light formulations are no longer niche. Regulatory pressure and anti‑ultra‑processed sentiment are making health positioning a baseline requirement, compressing premiums while reshaping product portfolios globally.

Convenience demand persists, but winning formats vary sharply by market:

Convenience remains a key driver, yet growth differs sharply by format. Frozen, chilled and shelf‑stable tomato products perform unevenly depending on price sensitivity, retail infrastructure and local consumption habits.

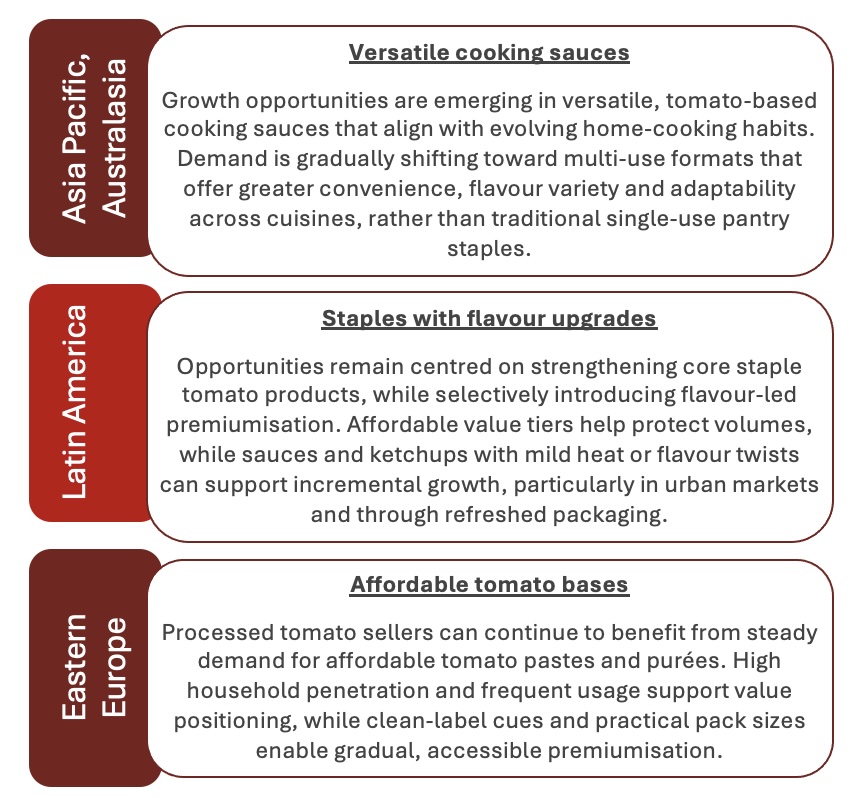

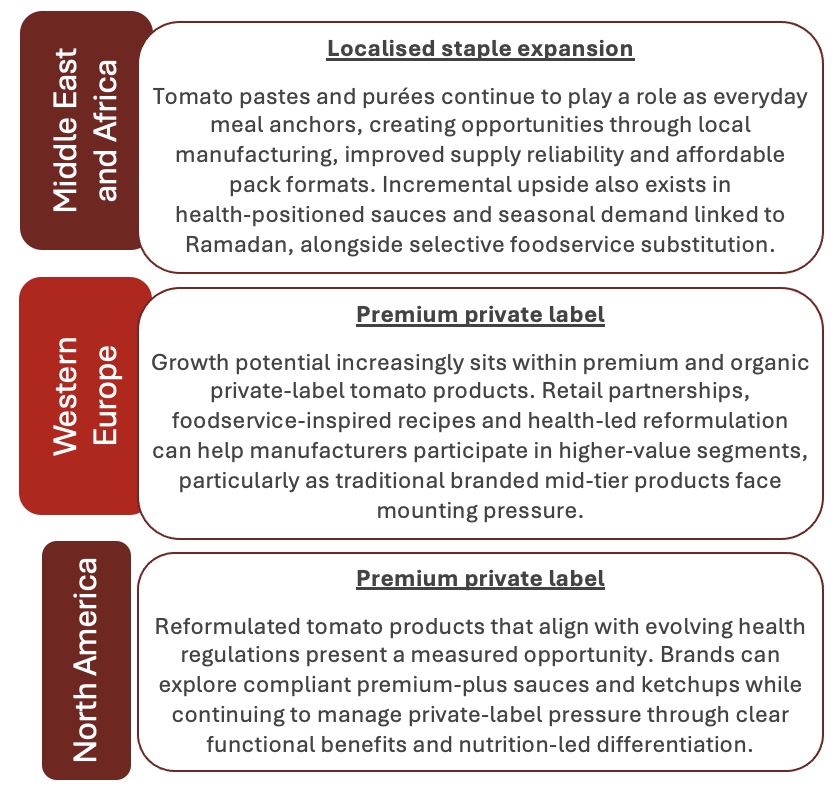

2. Key opportunity region wise

3. Tighter tomato supply drives pricing power across processed categories globally

Global processed tomato volumes are tightening in 2025 as heatwaves in Spain and Italy curb industrial yields and China rationalises acreage after weak 2024 pricing, constraining paste and purée availability which is the core input across ready meals, soups, pizza, pasta sauces, liquid recipe sauces and ketchup. Lower raw supply is limiting promotional intensity and private-label expansion, particularly in shelf-stable tomatoes. Meanwhile, the ~17% US tariff on Mexican tomatoes is reshaping sourcing economics and elevating ingredient costs. Value growth persists, driven by supply tightness, premiumisation (organic, clean-label, low-sodium), and cost pass-through from energy, packaging and logistics inflation.

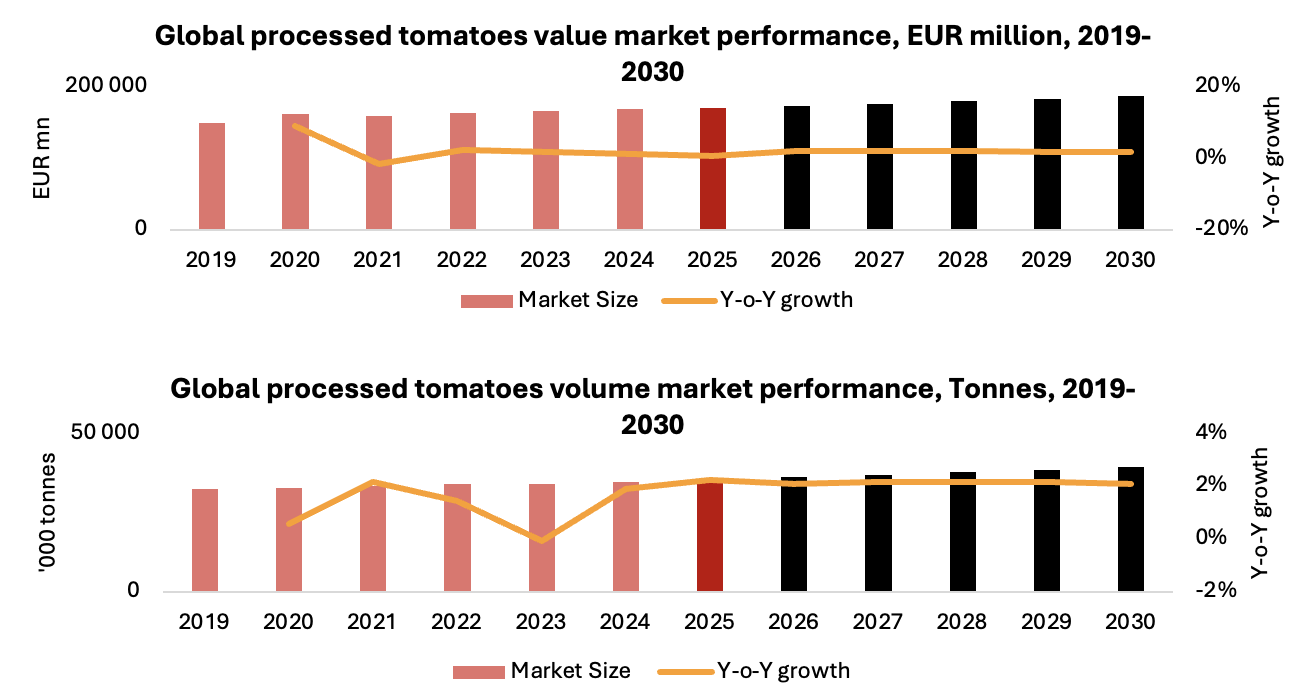

4. Processed tomato value outpaces volume amid cost and premiumisation pressures

5. Global Trends

Supply shocks and trade barriers compress margins

Climate disruptions in major growing regions such as the US and Italy are tightening tomato supply and increasing price volatility, while escalating trade barriers are reducing cross-border food flows. Exports as a share of global GDP are declining, and tariffs are spilling into food categories. Processed tomato producers face unstable input costs alongside consumers unwilling to absorb sharp price increases. Premiumisation opportunities are narrowing as cost-of-living pressures persist, concentrating value growth among higher-income consumers. Fewer goods moving globally is reshaping sourcing structures, retail channel dynamics and competitive positioning across markets.

Clean label shifts from premium to expectation

Consumers are prioritising health even amid financial strain, intensifying scrutiny of ultra-processed foods. Processed tomato categories are experiencing reformulation momentum toward clean-label, organic, non-GMO and minimally processed products. Demand is rising for natural ingredient lists, reduced additives and functional benefits such as fibre or protein fortification. At the same time, regulatory pressure around ultra-processing is building globally. This environment is shifting portfolio mixes toward premium, transparency-led offerings, while mainstream commoditised SKUs face slower value growth. Health positioning is becoming a structural expectation rather than a niche differentiator across sauces, pastes and meal bases.

Global tastes remain strong but local sourcing rises

Economic globalisation is slowing as trade barriers and geopolitical blocs reduce cross-border food flows, yet cultural globalisation remains strong. Consumers continue seeking internationally inspired flavours, using processed tomato products as core bases for global cuisines at home. A weaker global economy may further reinforce “travel through food” behaviour. However, as trade fragmentation reshapes sourcing structures, manufacturers face higher input volatility, tariffs and regulatory divergence. This may encourage regionalised supply chains and nearshoring strategies, reinforcing local production hubs even as consumer demand for globally inspired tomato-based dishes remains resilient across markets.

Scope of the study

Countries & Regions

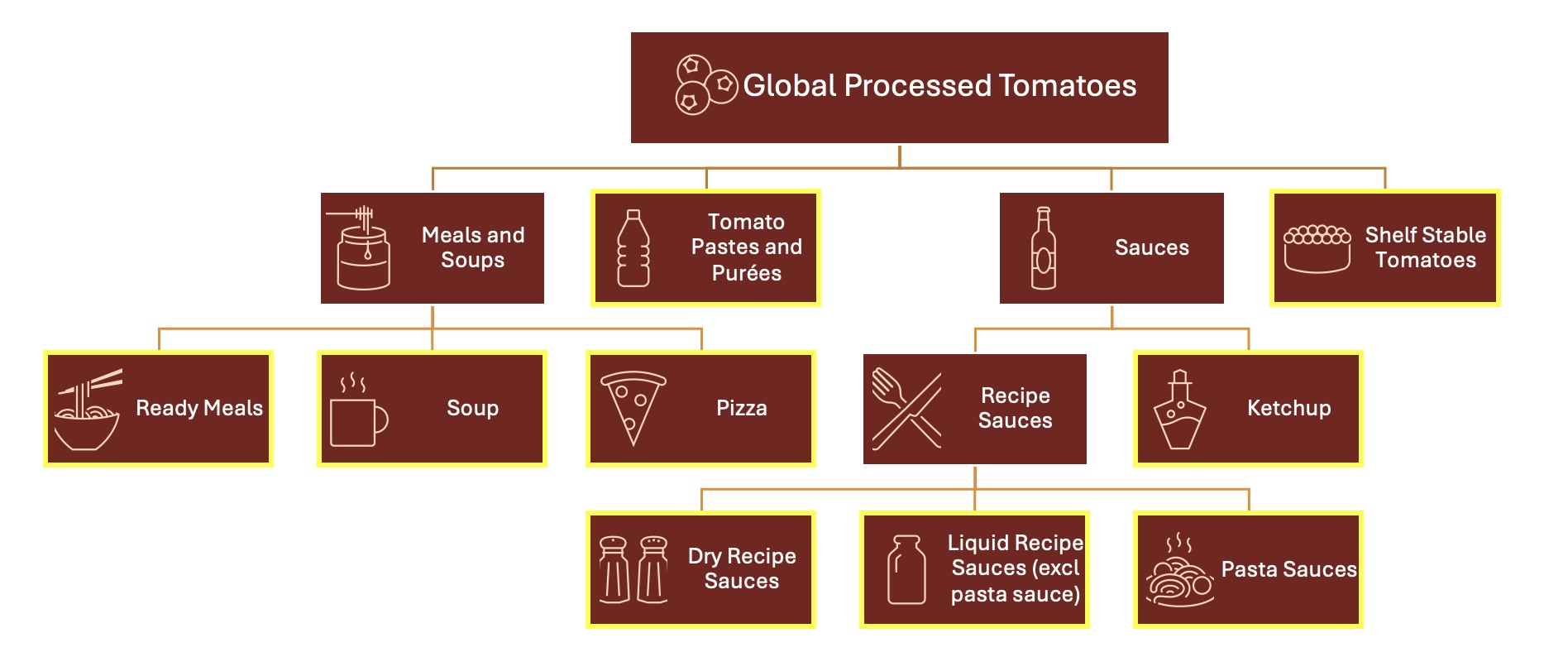

Product categories

Watch this space for more articles to come …

Source: Euromonitor International

{kind=link}