News

The Tomato Processing Industry in Kazakhstan (part 2)

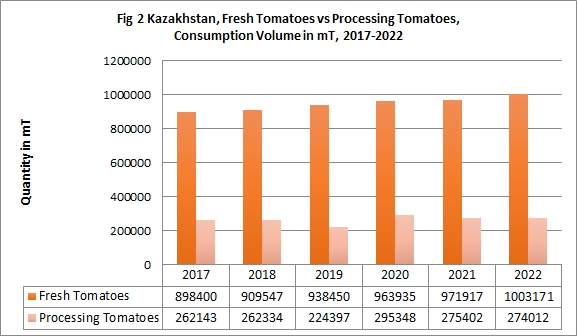

With an average annual production of processing tomatoes of about 95,000 tonnes over the last six years, the Kazakh industry devotes about 11% of its total fresh production (906,000 mT) to processing and covers only around 36% of its annual needs of tomato products, estimated at 265,000 mT.

Trade & Consumption

According to WPTC, the trade balance of processing tomatoes (raw material equivalent) reached 184,836 mT in 2021 from 153,159 mT in 2017. This reflects the country's reliance on imported processed tomatoes from China, Russia, Italy and Iran. The country was 42% self-sufficient as of 2019. However, owing to the negative impact of the Covid-19 epidemic, levels plummeted in 2020. According to the most recent estimates, in 2022, self-sufficiency levels are approaching 35%. Most recently, the development of the tomato processing sector has been one of the key government priorities as, Kazakhstan’s fresh tomato production do not meet the demands of the local market. This objective comprises of enhancing the capacity utilization of food processing firms, lowering dependency on imported food products, developing export capacities, and improving labor efficiency.

**2021 estimates indicate slightly subdued demand due to the Central Asian drought

Source: 2017-2022 figures from Kazakhstan Statistical Agency processed by WPTC

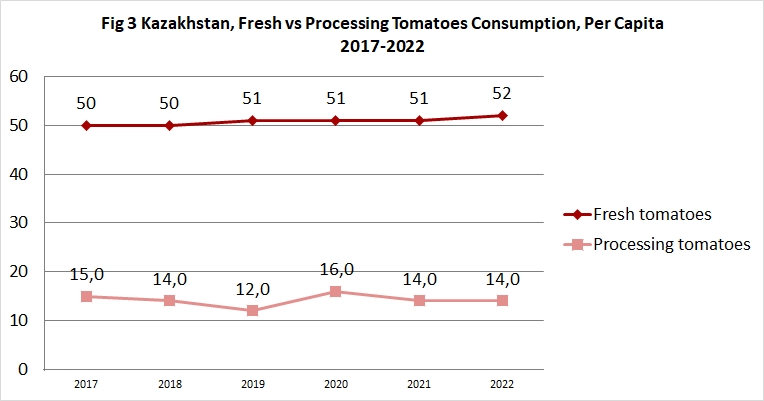

Source: 2017-2022 figures from Kazakhstan Statistical Agency processed by WPTC

Kazakhstan is primarily a consumer of fresh tomatoes as opposed to processed variants. The yearly per capita consumption of processed tomatoes fell by 13% in 2021, from 16kg in 2020. However, in the case of fresh tomatoes, per capita consumption has stayed stable for three years in a row, demonstrating that consumers prefer fresh varieties over processed ones. According to projections, per capita consumption of processed tomatoes would likely remain steady until 2022.

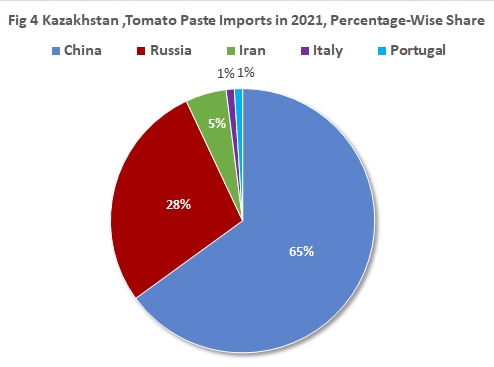

Kazakhstan’s tomato paste import volumes escalate in 2021

As per official statistics, Kazakhstan is a net importer of various processed tomato products including tomato paste, ketchup and canned tomatoes. In 2021, nearly 22,557 mT of tomato paste, 8,554 mT of ketchup and 1,251 mT of canned tomatoes were imported into the country amounting to a total value of USD 32 million. Compared to the previous year, the import of tomato paste witnessed an exponential growth of 49% after a period of suppressed demand in the pandemic hit year. Furthermore, in 2022, the import volumes of tomato paste and canned tomatoes are witnessing a decrease of 17% and 13%, respectively, while ketchup volumes are witnessing a positive 17% growth compared to 2021. This could be because the demand is being met by local production.

Source: WPTC

As per Fig 4, China is by far the key trading partner to Kazakhstan followed by Russia, Iran, Italy and Portugal. In 2021, Kazakhstan imported 21,827 mT of tomato paste from China. In the same year, approximately 555 mT of canned tomatoes and 8,231 mT of tomato ketchup was imported from Italy and Russia, respectively. Small volumes of tomato paste was re-exported to Russia in 2021 (approximately, 2,956 mT). Significant tomato paste export volume growth of 79% is projected in 2022 to Russia.

Tomato Processing Industry

The most common vegetable preserves prepared in Kazakhstan are tomato ketchup and canned tomatoes. Almaty city and the Almaty region produce the majority of canned tomatoes. The existence of a significant number of raw material suppliers in the region is one of the reasons why processing industries are concentrated in the Almaty region. This, in turn, makes timely sourcing of tomato harvests for processing in the appropriate amounts possible.

It is worth noting that most processing enterprises in the region have raw material specifications, and many farmers try to achieve these standards by cultivating tomatoes with their own resources. Many large processors prefer selling their ready products through major chain retailers, and a number of them even have their own units for transportation, storage, and sales as part of the company's infrastructure.

This system, on the one hand, provides for the complete production cycle, from cultivating fruits and vegetables to sales, but it also necessitates significant financial investments and the adoption of extra management and control mechanisms. However, this practice is frequently out of reach for small and medium-sized businesses.

Furthermore, due to the existence of strict raw material standards and requirements, large processors prefer to work with large suppliers or grow their own fruits and vegetables for processing, which means small farms are unable to compete and maintain the required level of quality, volume, and supply schedule. Experts estimate that a substantial number of unresolved concerns and challenges continue among local farmers and processors, many of which include a lack of information about product varieties, volumes, and quality. Furthermore, raw materials provided to processors must be harvested, packaged, and delivered within a specific time frame while according to established criteria. Any differences in volume, quality, size, and so on may result in the produce being rejected by the processor, reducing the farmer's potential to earn.

There is a shortage of trained specialists in the industry, particularly in agronomy, cultivation, irrigation, selection, logistics, and packing. Despite a yearly increase in tomato output in Kazakhstan, demand for tomatoes during the off-season remains unsatisfied.

The need of the hour is to provide scientific support to tomato processing industry thereby boosting the sector's total production efficiency.

The Leading Tomato Processing Companies in Kazakhstan

Tsin Kaz LLP

Founded in 1998, Tsin-Kaz LLP is biggest tomato paste producer in Kazakhstan. Apart from tomato paste, the company produces ketchups, different types of sauce (Satsebeli, Adjika, Cobra, Soy, Red hot chili etc.) and Salads. Currently, the company captures a 50% market share for its finished tomato products. With an annual production capacity of 13,000 mT of tomato paste and 3,000 mT of tomato ketchup Tsin Kaz exports to CIS countries. The company has two processing factories in Kazakhstan and one based in Urumqi, China. At these facilities, the cold-break system is deployed for the production of tomato paste. The finished tomato products are packed into glass jars, metal cans and doypack. The company adheres to the ISO22000 quality norms and Kaizen (Japanese Management System) at their factory and office. Tsin Kaz aims to expand its exports globally.

Aidos Sultankulov, Export Manager at Tsin Kaz LLP notes that the processor uses tomato varieties including HENIZ 1015, YAXIN 82, YAXIN 87 and HENZI 8113 for the production of tomato concentrates. These concentrates are in turn used for manufacturing tomato paste. According to Aidos Sultankulov, the growth in the Kazakh tomato processing industry is hindered by market instability and low cultivation capacity of tomato crops, among others. However, by increasing the annual acreage and promoting automation, the tomato processing industry can further be developed. The processor reported a reduction in its capacity by 60-70% in 2020 following the suspension of production activities due to the Covid-19 pandemic.

MASLO-DEL

MASLO-DEL, is one of the largest companies in Kazakhstan for the production of food products. The company employs more than 2,000 employees, of which the number of sales teams is about 860 people. The plant for the production of finished products in Almaty produces up to 74 thousand tons per year of finished products such as condensed milk, butters, spreads, margarines, fats, tomato paste. The production capacity of tomato paste alone is 34 mT/day.

Eurasian Foods Corporation JSC

Almaty based Eurasian Foods Corporation is one of the leading and most important food enterprises in the Republic of Kazakhstan and Central Asia. The company produces tomato ketchup under its brand name 3 Zhelaniya apart from fat, oil and dairy products. The combined annual production volume of all the products manufactured by the company exceeds 140 000 mT.

Golden Food Company LLP

Golden Food Company LLP has been operating in Almaty since 2000 and currently occupies a leading position in the market for the production of refined sugar and canned fruits and vegetables. It manufactures tomato paste and sauce under its own brand name as well as provides private labeling for third-parties. The company's products are sold in stores, wholesale and retail and large retail chains throughout Kazakhstan and neighboring countries.

The other relevant tomato processors in the region include Tomatyi Rai, Barskaya, Primario, Astana Bottlers, DMD Production LLP and Solenich, among others.

{kind=link}