News

2026 Congress Day 2: Guido Afdemkamp

NAVIGATING FOOD PACKAGING RECYCLING MANDATES:

CHALLENGES AND POTENTIAL SOLUTIONS FOR EUROPE

From the presentation of Guido Aufdemkamp, Executive Director, Aseptic Bag Manufacturers Association (ABMA)

Who is the ABMA and What is at Stake?

Who is the ABMA? Basically, we represent the producers of industrial aseptic bags. The global representation across our membership is quite significant; we are a global group with members all across the world on the manufacturing side, operating as a subgroup of the European packaging association, FPE.

Just to remind ourselves what industrial aseptic bags actually are: they are high-performance bags—usually 55-gallon (220-liter) or 300-gallon (1,000-liter) sizes—used either inside steel drums or intermediate bulk containers (IBCs). Their main advantage is providing a stellar shelf life of up to 24 months for ambient storage. In our industry, this is the vital mechanism used to keep stocks and transport product around the world without a cool chain, allowing us to mitigate seasonal harvest variability. As we all know, the tomato business is a truly global business.

The Reality of the Global Tomato Supply Chain

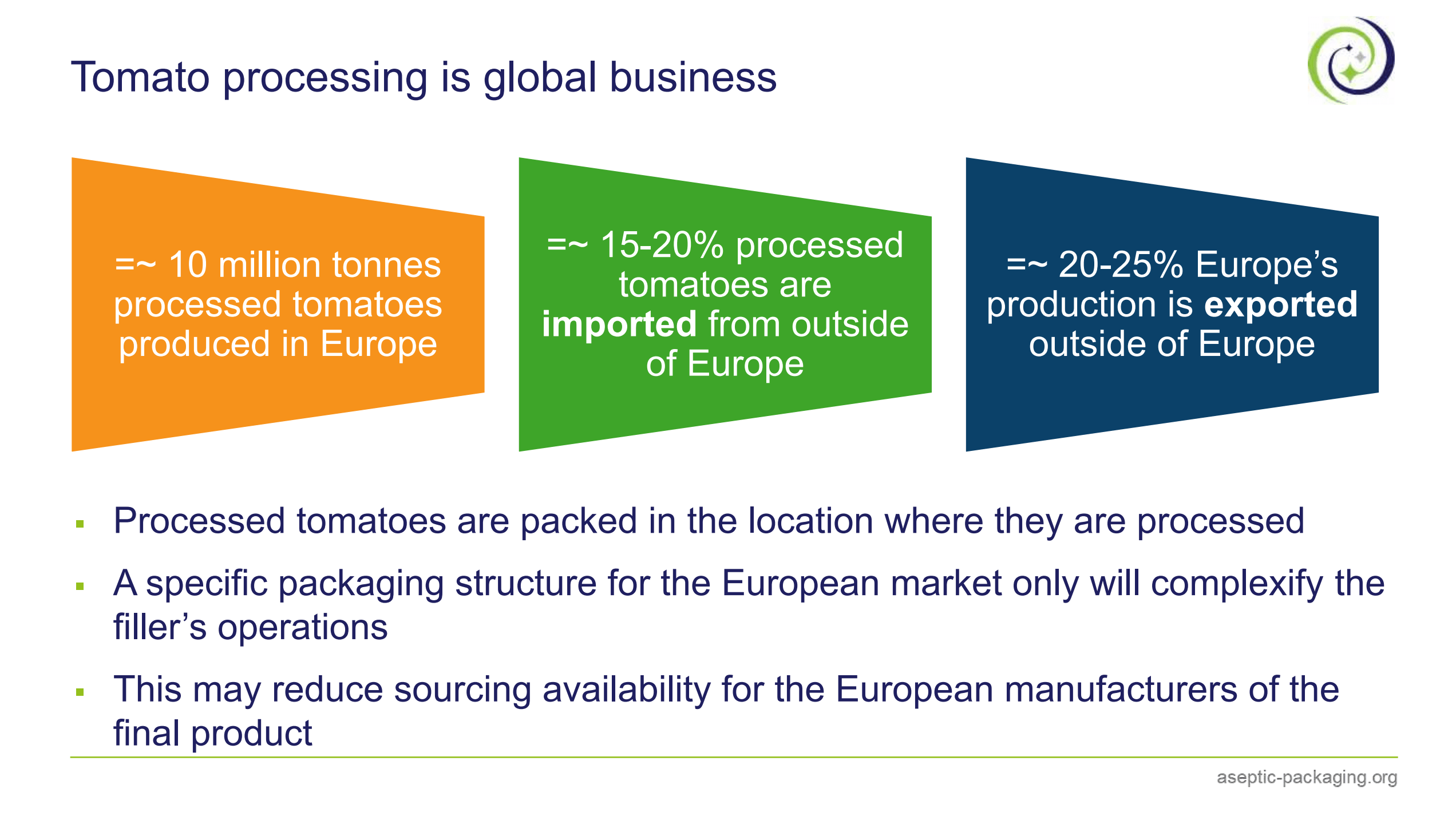

To put it into perspective just for Europe: we use about 10 million tonnes of processed tomatoes. Roughly 15% to 20% of that demand is imported from outside the EU, and more than 20% of what we produce is exported. Because tomatoes must be packed exactly where they are processed, a major issue arises if we change things up.

If the European Union forces a unique packaging structure onto the market, it will obviously make the life of the filler much more complicated. Operating various, fragmented packaging schemes will drastically reduce raw material sorting and sourcing availability for the end-users who manufacture the final products. It is a critical part of the global value chain.

The Arrival of the PPWR

Let’s get to some basics first. I don’t know if we should be happy to say from the European side that we are the first in the world with a major packaging legislation coming up, but we are definitely not the last ones doing this. For those of you involved in advocacy, lobbying, or public affairs, I can tell you that this specific file was the most lobbied file ever in European history.

It starts with a simple realization: everybody is affected by packaging. Every raw material coming into your factories, and everything you send out to your customers, involves packaging. That realization came on slowly in some industries, but then it hit like a tsunami.

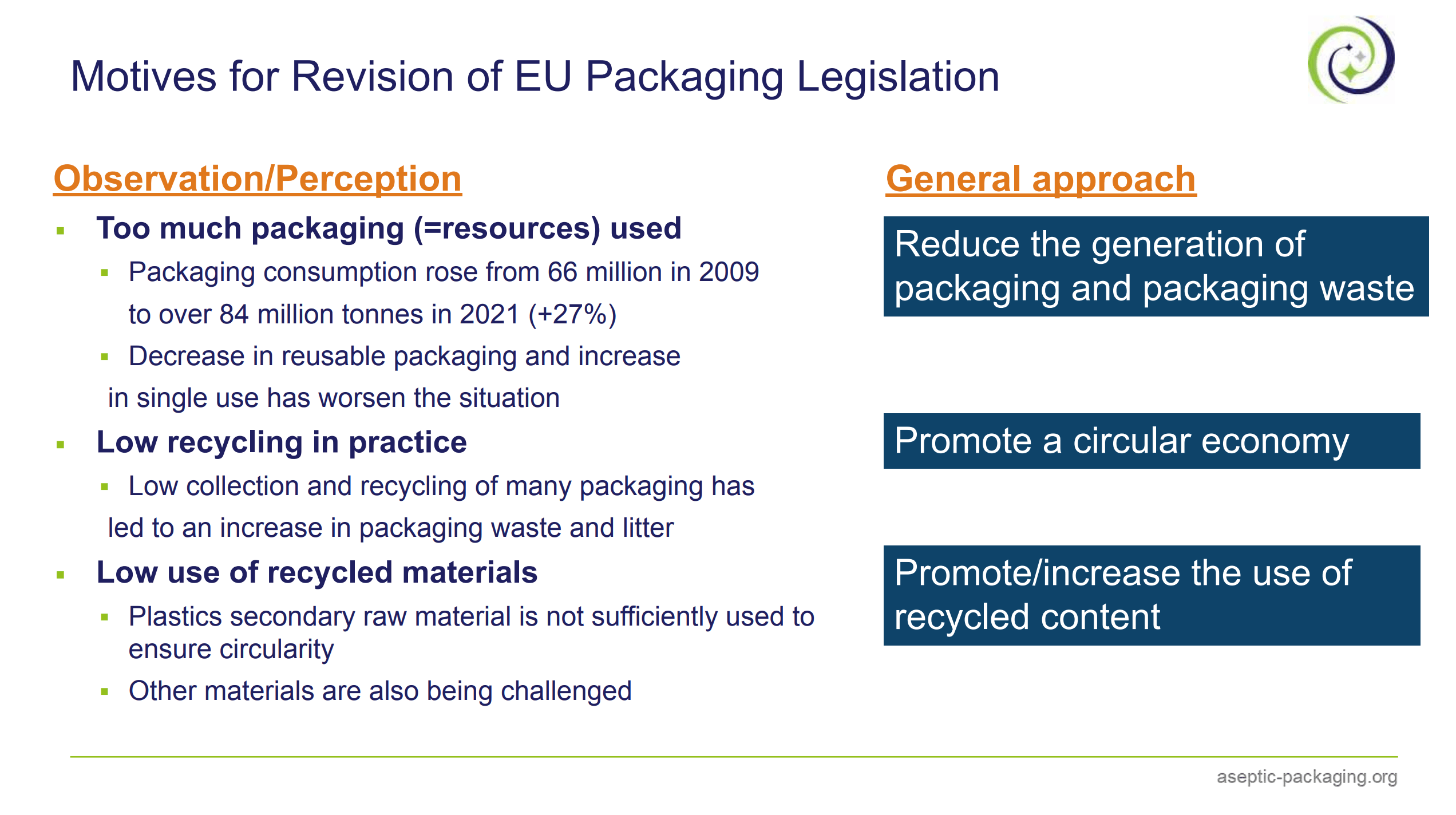

Why? Because the legislators look at it and say there is simply too much waste. Whenever you talk with family and friends, you can always agree on two things: everybody is a schooling expert because they went to school, and everybody is a packaging expert because they use packaging. We cannot always agree on religion or sports, but we can always agree that packaging is bad, it’s too much, and we are obsessed with it.

Politicians love this because the public supports the cause. The goal of this new law is to reduce packaging waste, promote a circular economy because there isn’t enough recycling in practice, and force an increase in the use of recycled content.

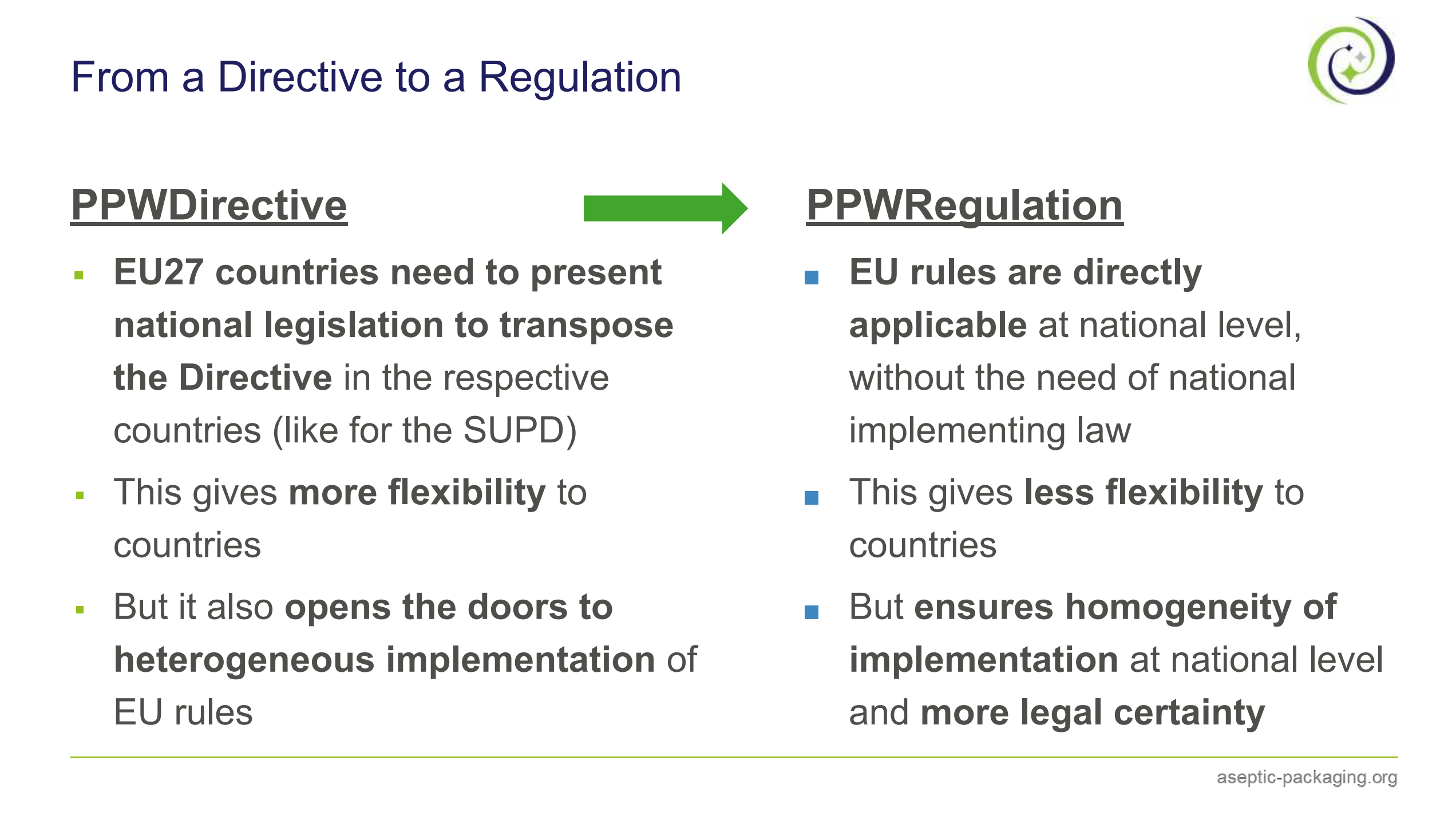

Compared to the U.S., we are a bit lucky in Europe because we only have 27 member states to deal with, not 50. And this new legislation is a Regulation, not a Directive. The major difference is that a regulation does not need to be transposed into 27 different national laws; it is automatically applicable to all member states.

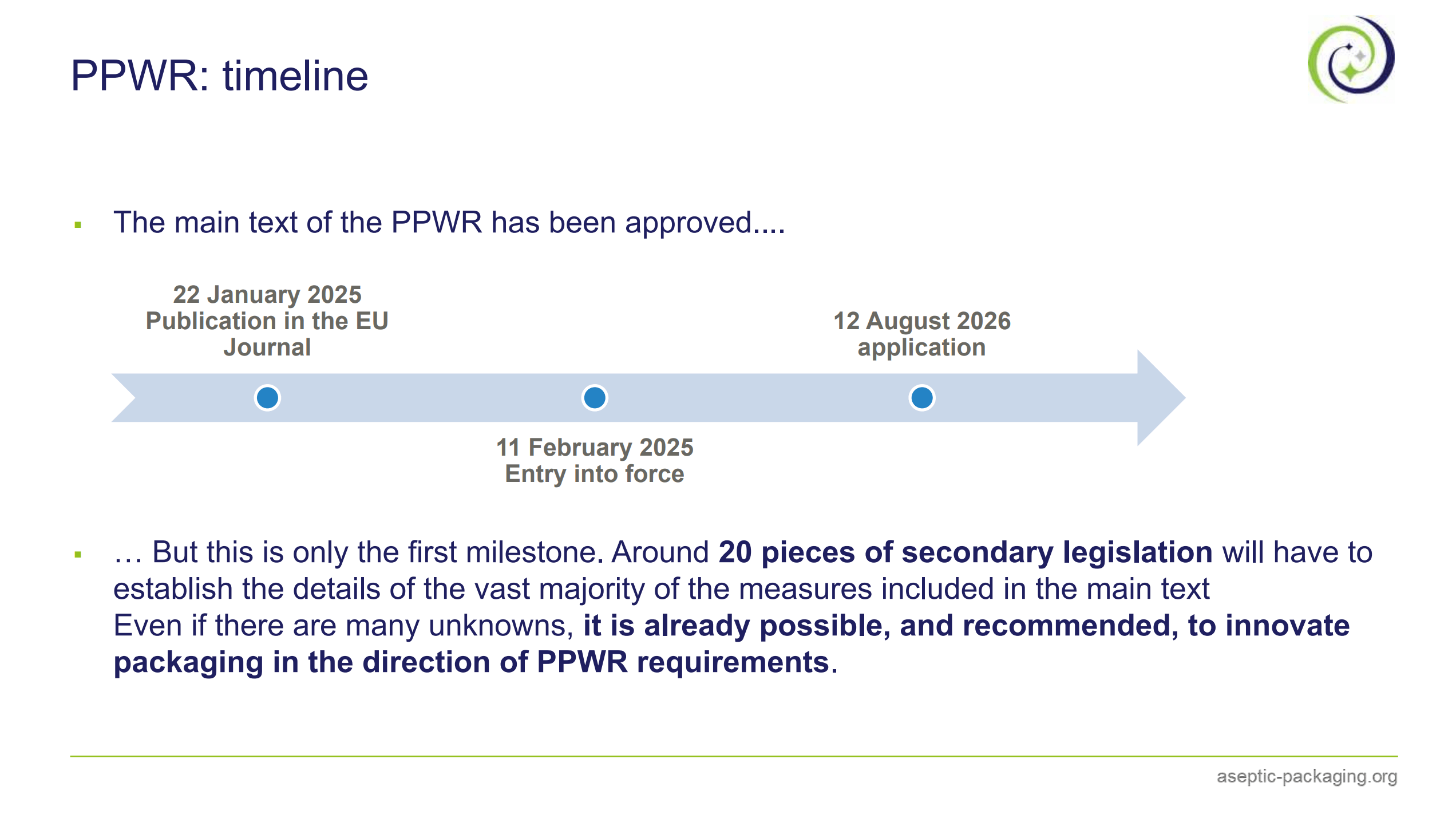

The main text enters into final application on August 12, 2026. However, not everything happens on day one. We still need about 20 secondary legislations—acts written by the Commission—to define the exact technical details. Even so, 90% to 95% of the direction is already very clear.

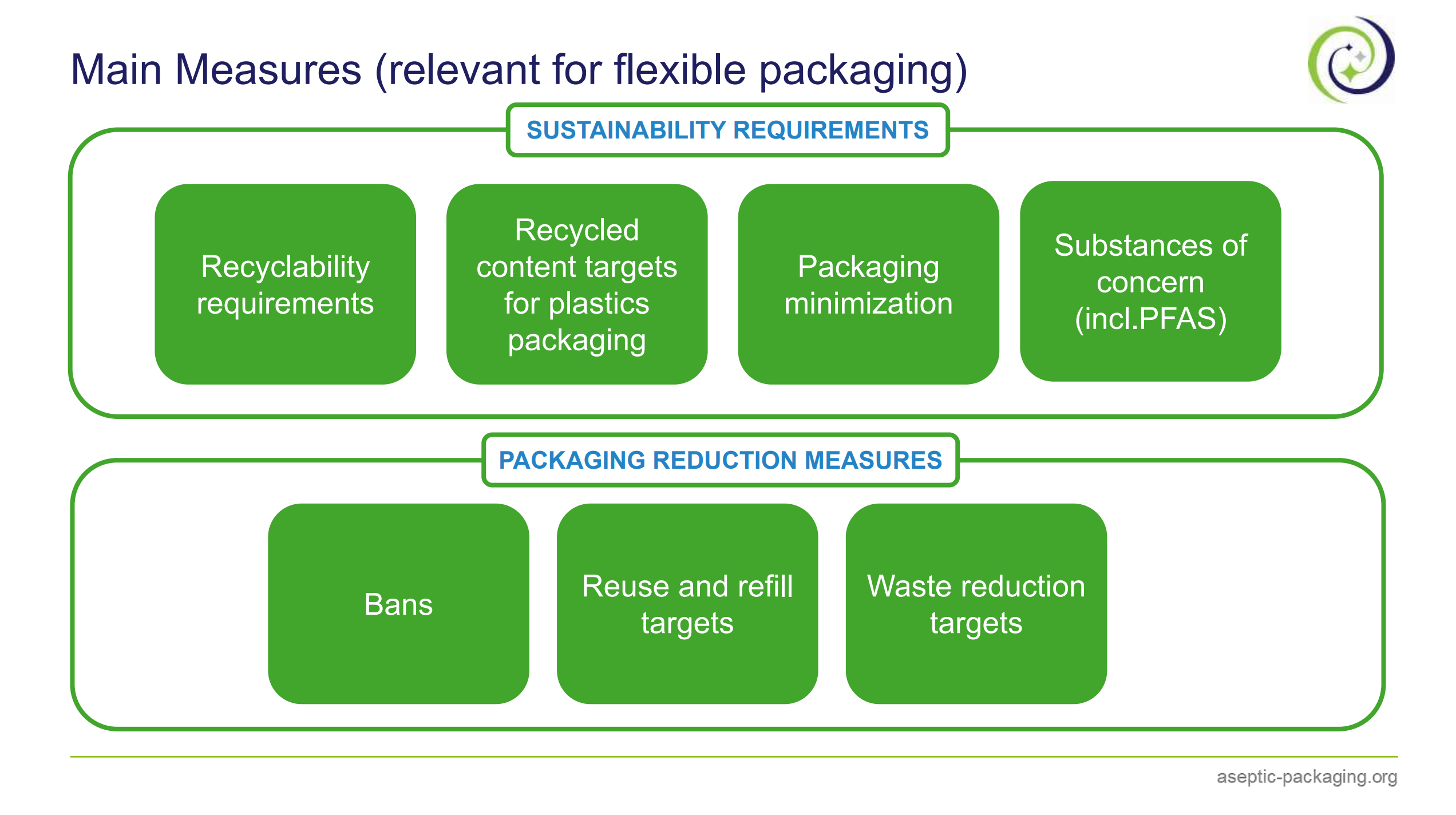

Sustainability Requirements & The Threat to Market Access

The core measures relevant to flexible packaging and aseptic bags boil down to sustainability requirements: recyclability, minimization of packaging weight, and the minimization of substances of concern, including a total ban on PFAS. There are also general reduction measures, like bans on plastic condiment sachets for in-store consumption—yes, your classic ketchup sachets are heavily targeted. There will also be a mandatory 10% reuse target for things like water, soft drinks, and beer, which will have a major impact on retailers.

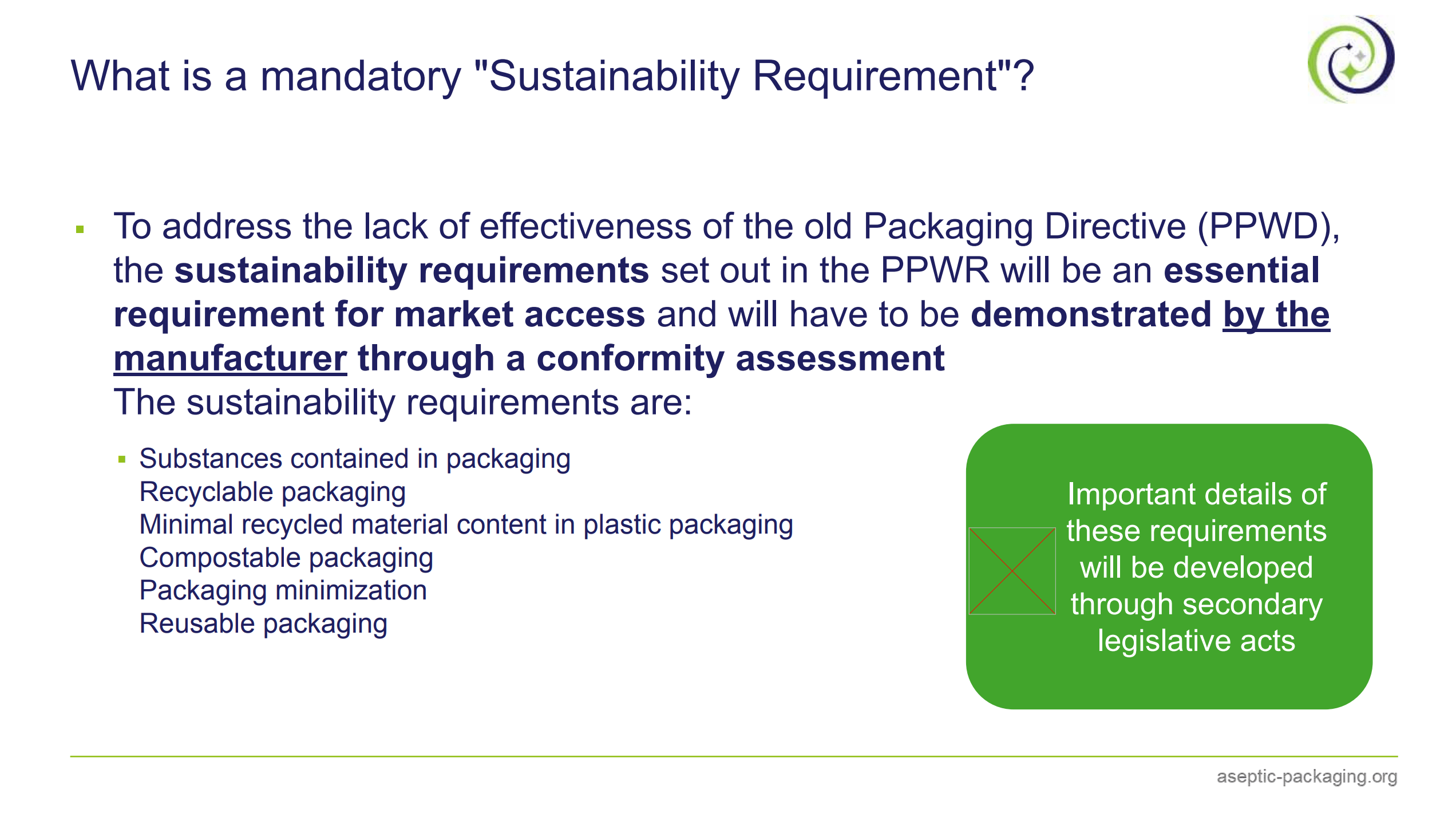

In the past, sustainability requirements were a bit vague, and you could always make an excuse or a workaround for marketing reasons. In the future, these requirements are strictly mandatory and are a direct condition for market access. Let’s realize this clearly: not meeting sustainability requirements equals no market access. And this isn’t just for European manufacturers; it applies to absolutely anyone placing packaged products onto EU territory, meaning all global importers are equally concerned.

Legal Responsibility: Who is the “Manufacturer”?

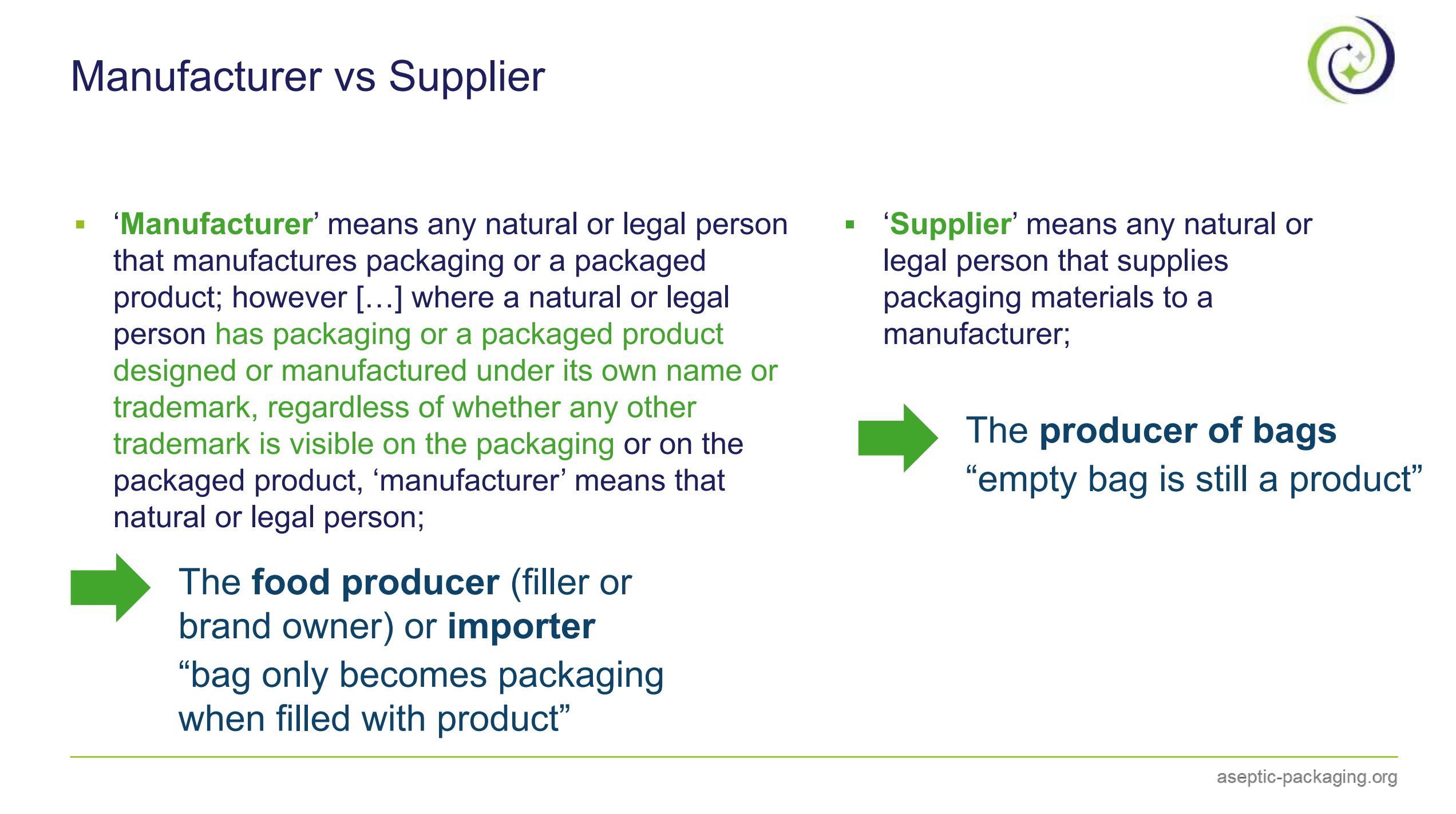

Let’s take a step back and look at a very important definition: the difference between a manufacturer and a supplier. Two years ago, I had to tell all my ABMA members: you are not the manufacturers of packaging. Tetra Pak, for example, is not a packaging manufacturer; they are suppliers of packaging materials.

A material only legally becomes ‘packaging’ when something gets put inside it and it is sealed or closed. Therefore, the food producer—the filler or the importer—is legally the manufacturer of the packaging because they run the brands. The only exception is private labels, where the retailer defines the design and composition; in that specific case, the retailer becomes the manufacturer.

Why does this matter so much? Because most of the legal obligation and responsibility lies entirely with the packaging manufacturer. All these sustainability rules must be fulfilled by the filler or the retailer.

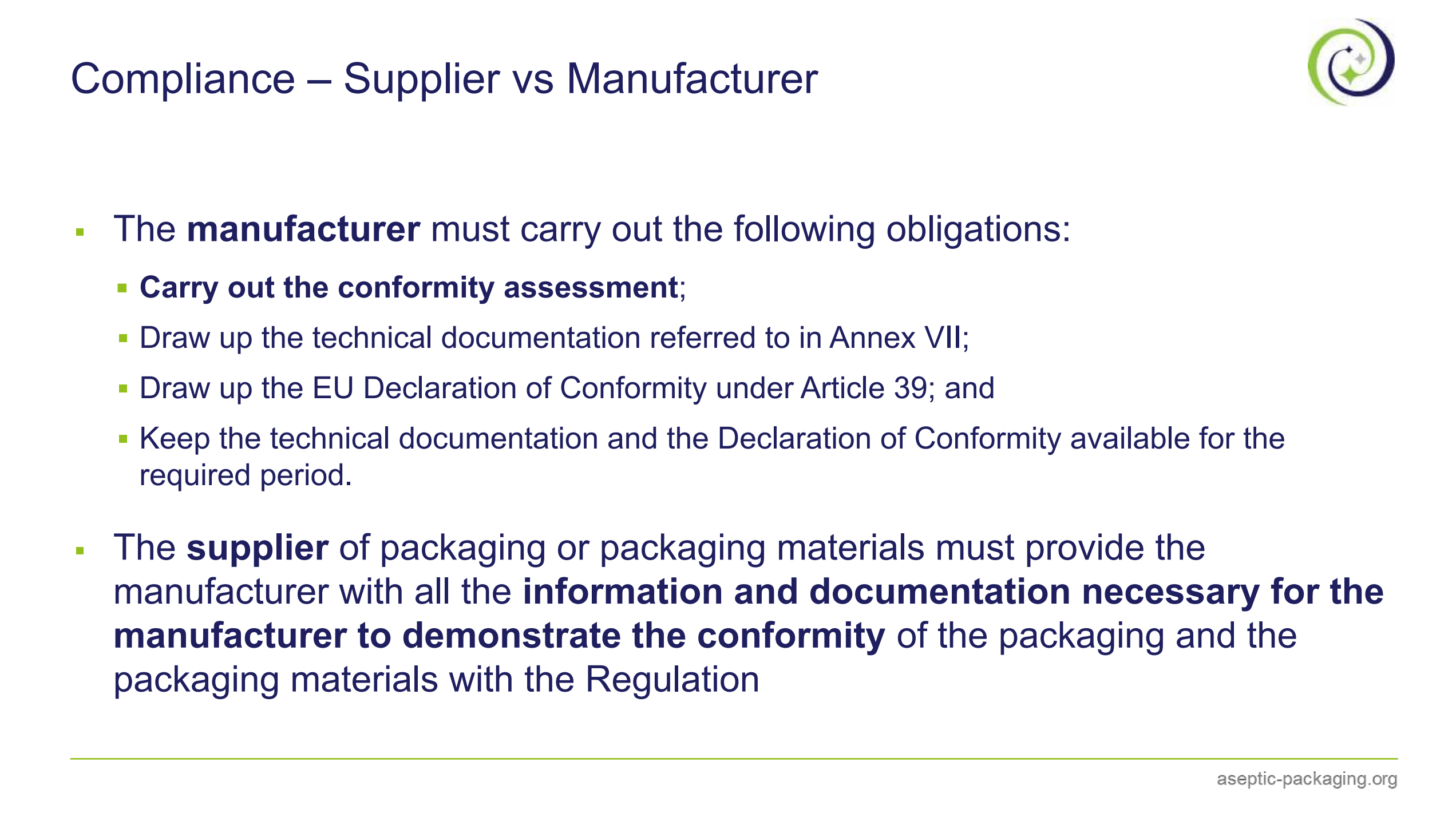

Think of a yogurt cup: the plastic cup and the foil lid are usually supplied by two different companies. Neither the cup supplier nor the lid supplier can be held accountable for the total packaging compliance. But the dairy filler puts them together, making the final packaging. That’s why the filler has the lead responsibility to carry out component assessments, draw up technical documentations, and sign the official Declaration of Conformity under Article 39 to keep on file for the authorities. The material supplier isn’t off the hook, of course; they are legally obliged to support the filler with all the necessary technical data and documentation so their customer can comply.

The 2030 Deadline and the Recyclability Grades

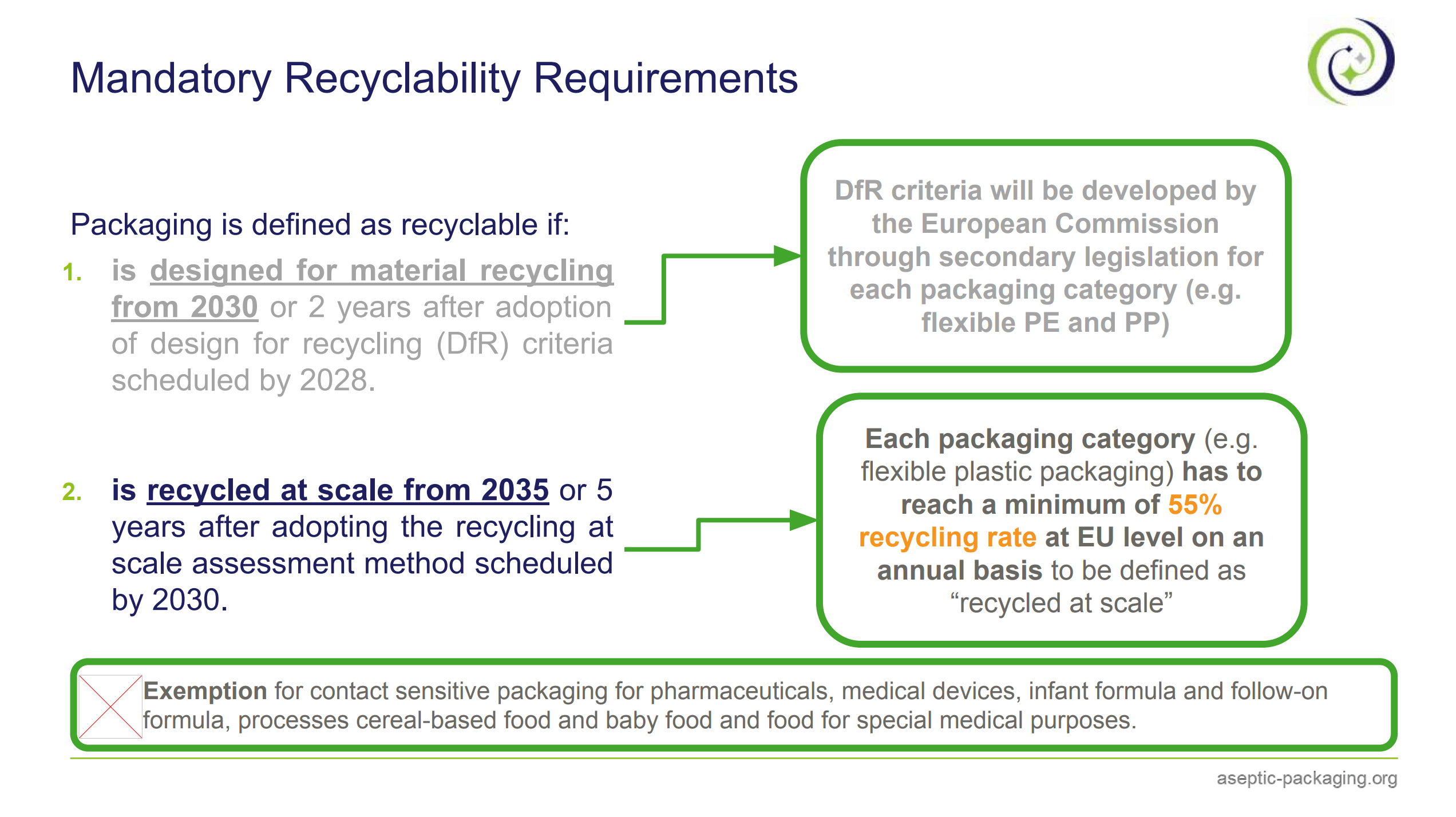

Under the new law, no packaging can go on the market if it isn’t recyclable. It must be designed for material recycling according to guidelines currently being developed in secondary legislation for categories like flexible PE and PP. There are only three narrow exemptions—pharmaceuticals, medical devices, and infant formula. Food supplements, though their producers would love to feel like pharma companies, are not exempt and must comply.

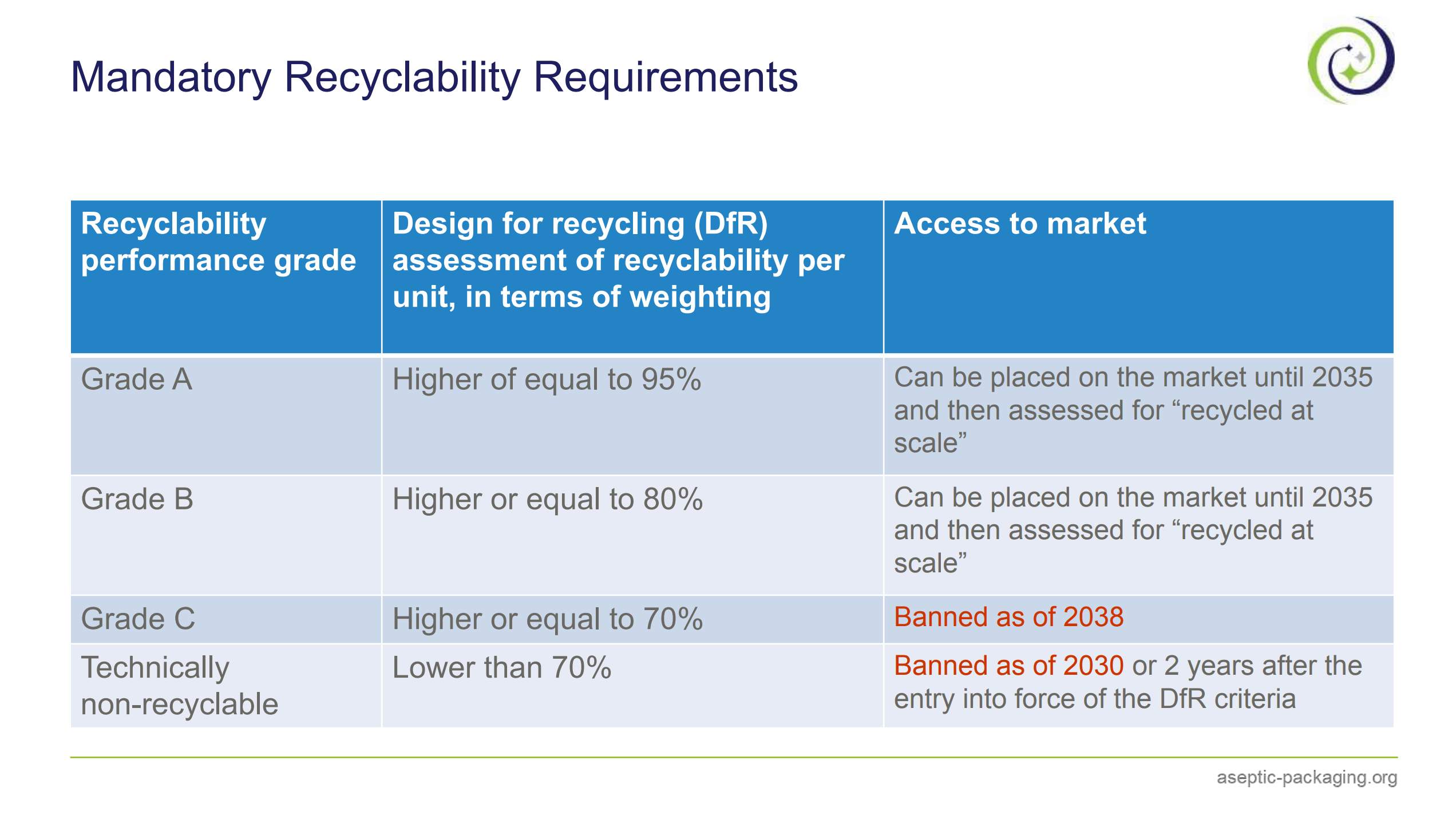

In practice, there are 4 grades for recyclability based on a weighting system, which gives the legislation some flexibility. For flexible packaging, this weighting is crucial because we are advocating to take adhesives and varnishes out of the weight calculation.

- Grades A, B, and C require a minimum threshold of 70% recyclability to maintain market access. If you are below 70%, your packaging is considered technically non-recyclable and you are completely out.

- By 2038, that minimum threshold rises to 80%.

Furthermore, this recyclability must be proven ‘at scale’ by 2035, meaning a minimum 55% recycling rate must be achieved in reality at the EU level. Think about the waste stream math: collection, sorting, and actual recycling are dependent on each other. To hit 55% overall, you need at least 82% efficiency in each of those three steps, because 82% * 82% * 82% = 55.1%. That is an incredible challenge.

Once you prove you are recyclable, you have to meet the next challenge: integrating recycled plastic content. For PE-based aseptic bags, the mandate is a minimum of 10% recycled content by 2030. And be careful—this must come from post-consumer recyclates (PCR), not pre-industrial scrap or industrial waste. The law says you only have to meet this if the material is available, and honestly, price won’t be the blocker—availability will be. Because our packaging touches food, we require food-grade recyclates, which is currently only feasible via chemical or advanced recycling, and the global capacity simply isn’t there yet.

Why Current Aseptic Bags are Facing a Total Ban

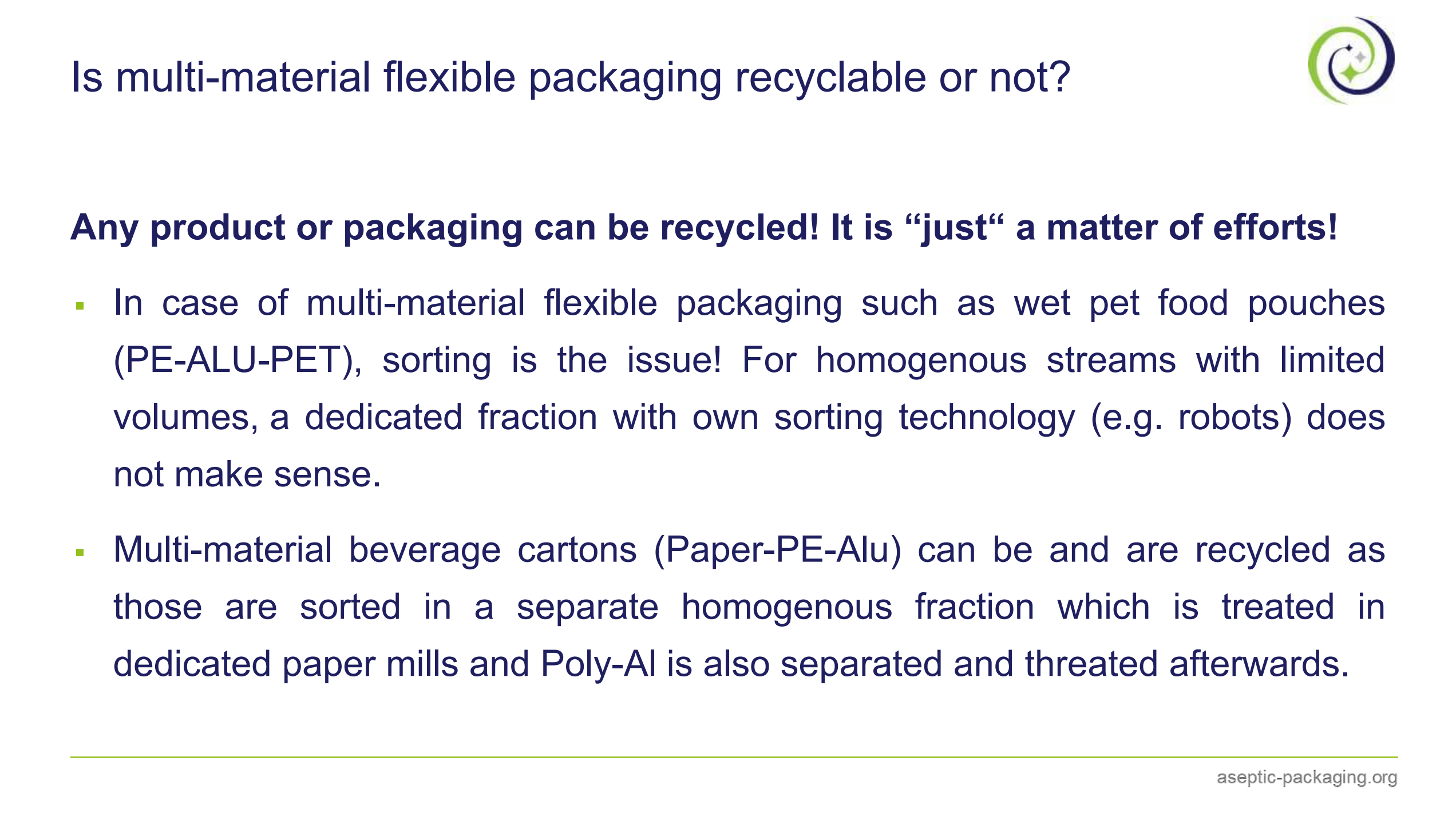

So, what does this mean for aseptic bags today? Is our material recyclable? Generally, everything is recyclable if you put enough effort and money into it. Look at two examples that look similar but have totally different results: Multi-material retail pouches (like wet pet food pouches made of PE-Alu-PET) are not considered recyclable because sorting centers don’t separate them out. They end up lost in the aluminum stream and fail the 70% threshold. On the other hand, beverage cartons (like Tetra Pak structures) are considered recyclable, not because of a magic material, but because sorting centers separate them into a dedicated section where specialized recycling technologies can be applied. It’s a matter of sortability, not just composition.

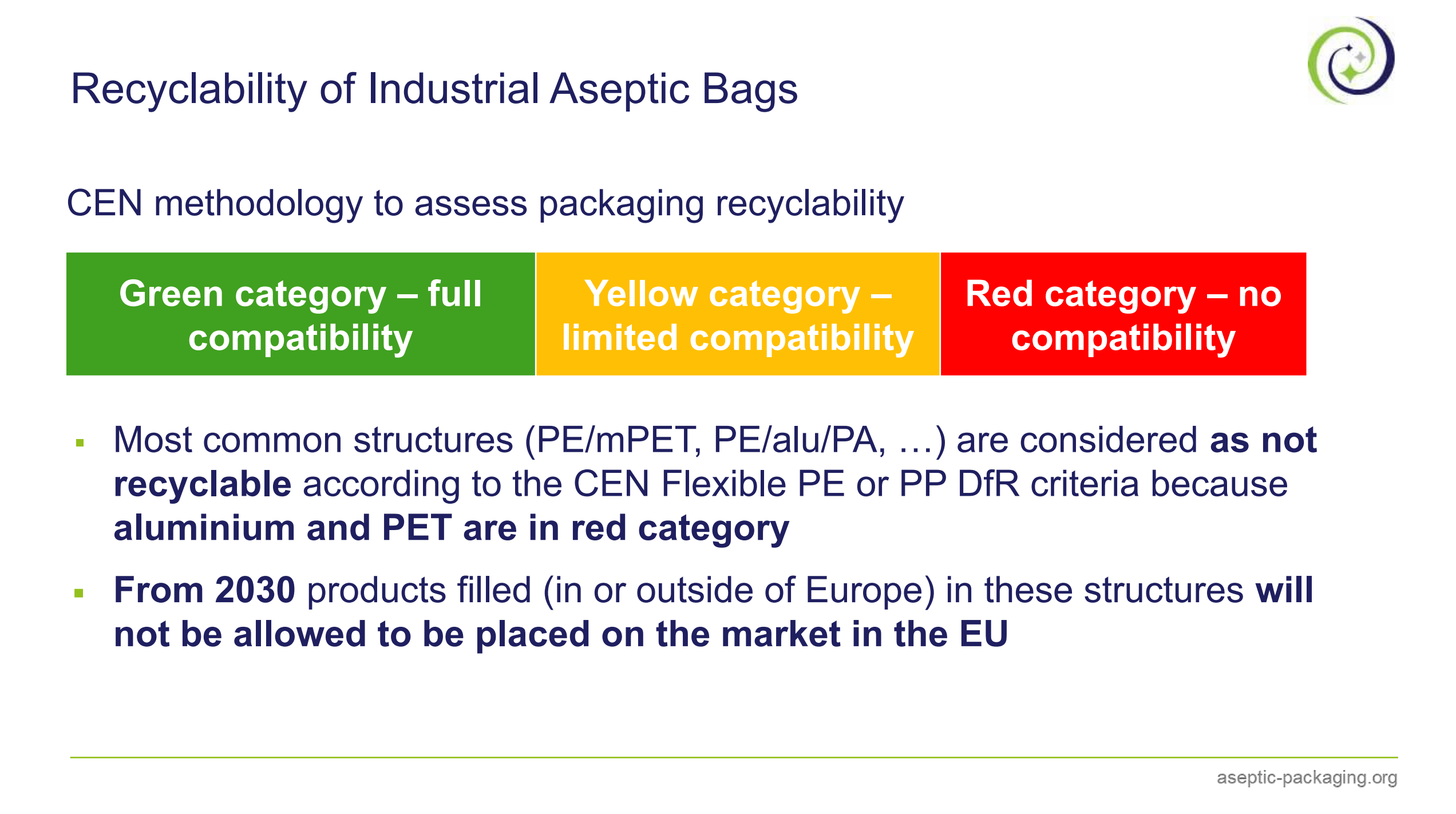

When the European standardization organizations looked at the common structures of today’s aseptic bags—which rely on polyester (mPET) or aluminum foils for barriers—they placed those materials squarely in the Red Category. Under the law, if your packaging contains even a single constituent in the Red Category, the entire structure is disqualified.

This means that the aseptic bags we use today, developed over decades, which everyone is happy with, cannot legally be placed on the EU market as of January 1, 2030. It doesn’t matter if it’s filled inside Europe or filled outside and imported; if it lands on EU territory, it is banned. The only exception is if you fill it in Europe and export it entirely outside the EU.

Now, some tomato processors are reacting to this by trying to ask for a legal exemption. In April, a famous letter was signed by 140 major companies asking the EU Commission to stop the clock and change the rules. But let me warn you: there is no such thing as a targeted, clean amendment for this kind of law. Asking for an exemption requires fully reopening the primary legislation, which is a total Pandora’s box. Instantly, everyone will bring their own wishes to the table, it will become a disaster, and it will open the door for the 27 member states to start issuing their own wild mix of national laws in the meantime.

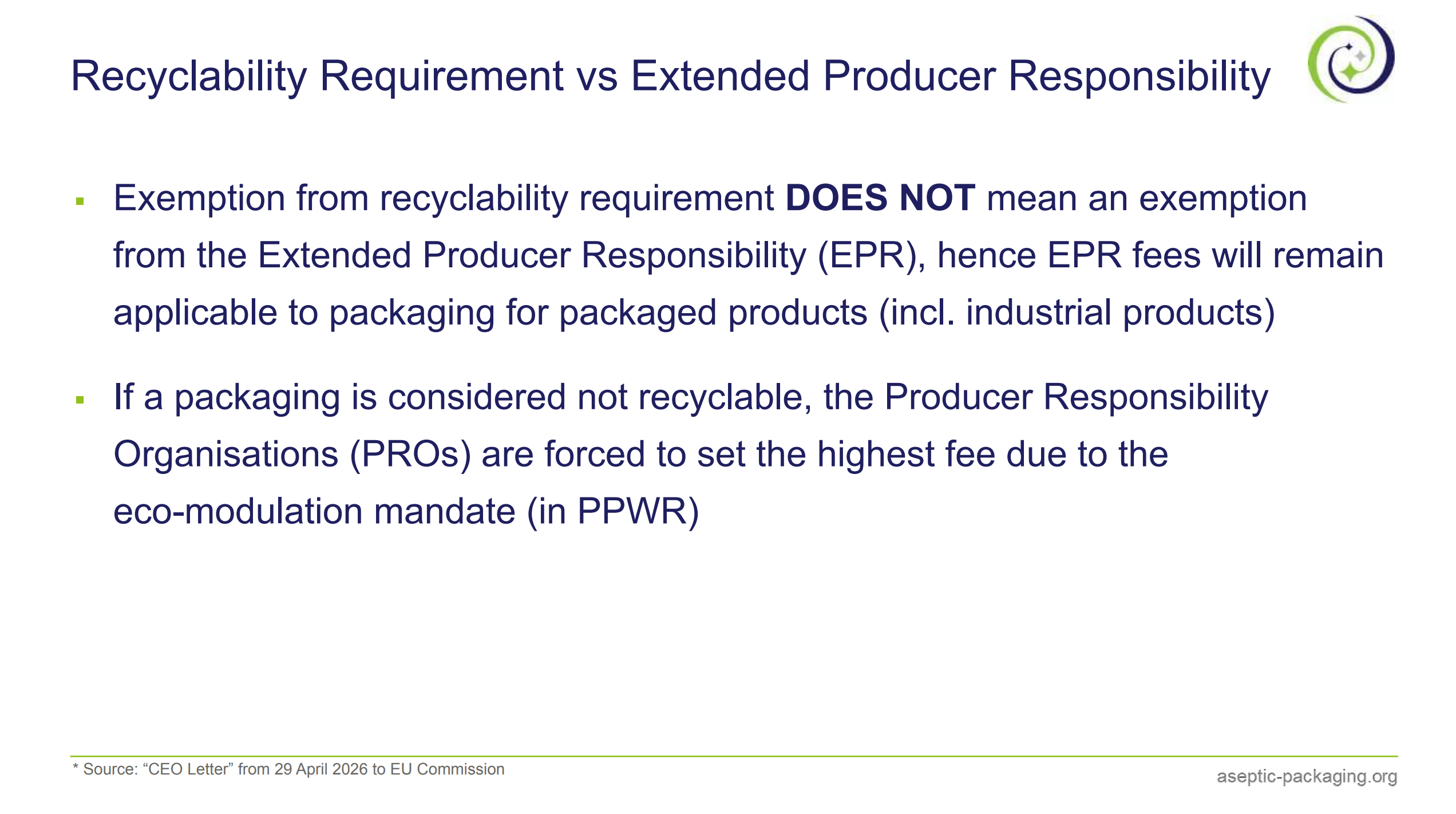

Worse yet, a recyclability exemption does not mean an exemption from Extended Producer Responsibility (EPR) fees. You will still have to pay. And if your packaging is labeled ‘not recyclable,’ the law mandates that the Producer Responsibility Organizations (PROs) must slap you with the highest possible financial penalty via eco-modulation. You will pay a massive ‘Malus’ fee, and still, nobody will want your waste.

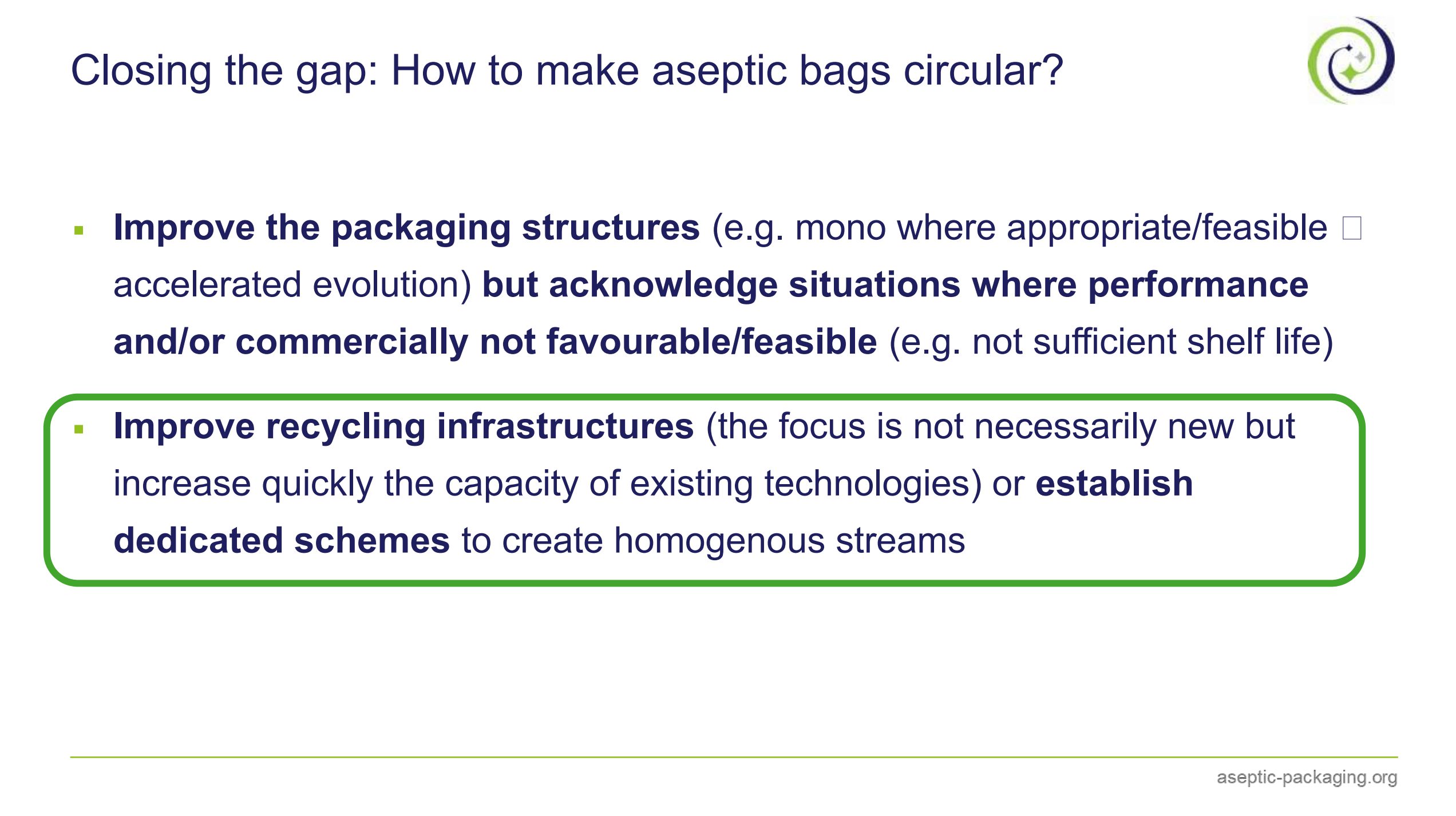

So how do we make an aseptic bag circular? One way is to change the material to mono-structures, but your barrier performance goes down massively. Instead of a 2-year shelf life, you might get 9 months, and it will be vastly more expensive.

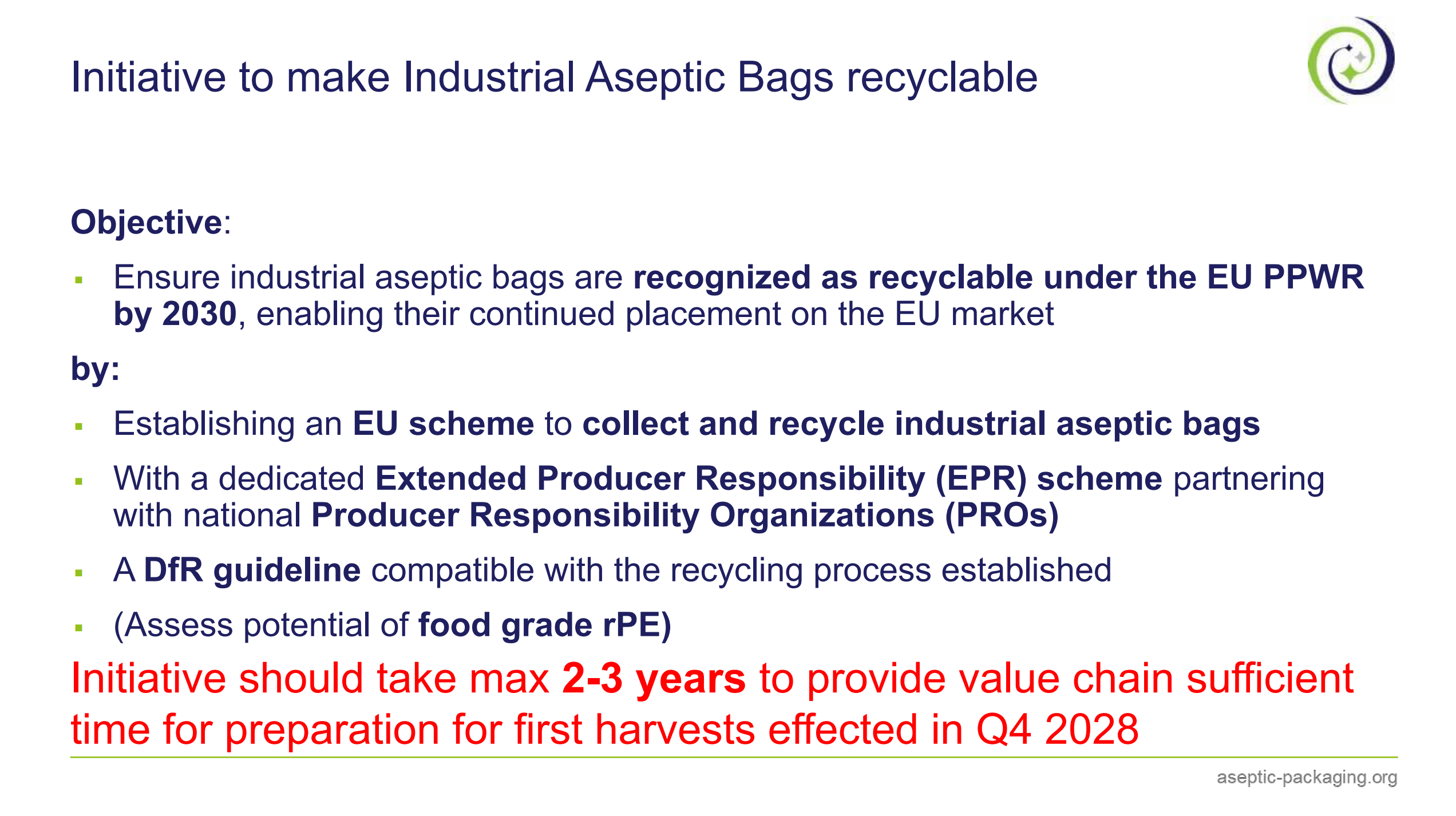

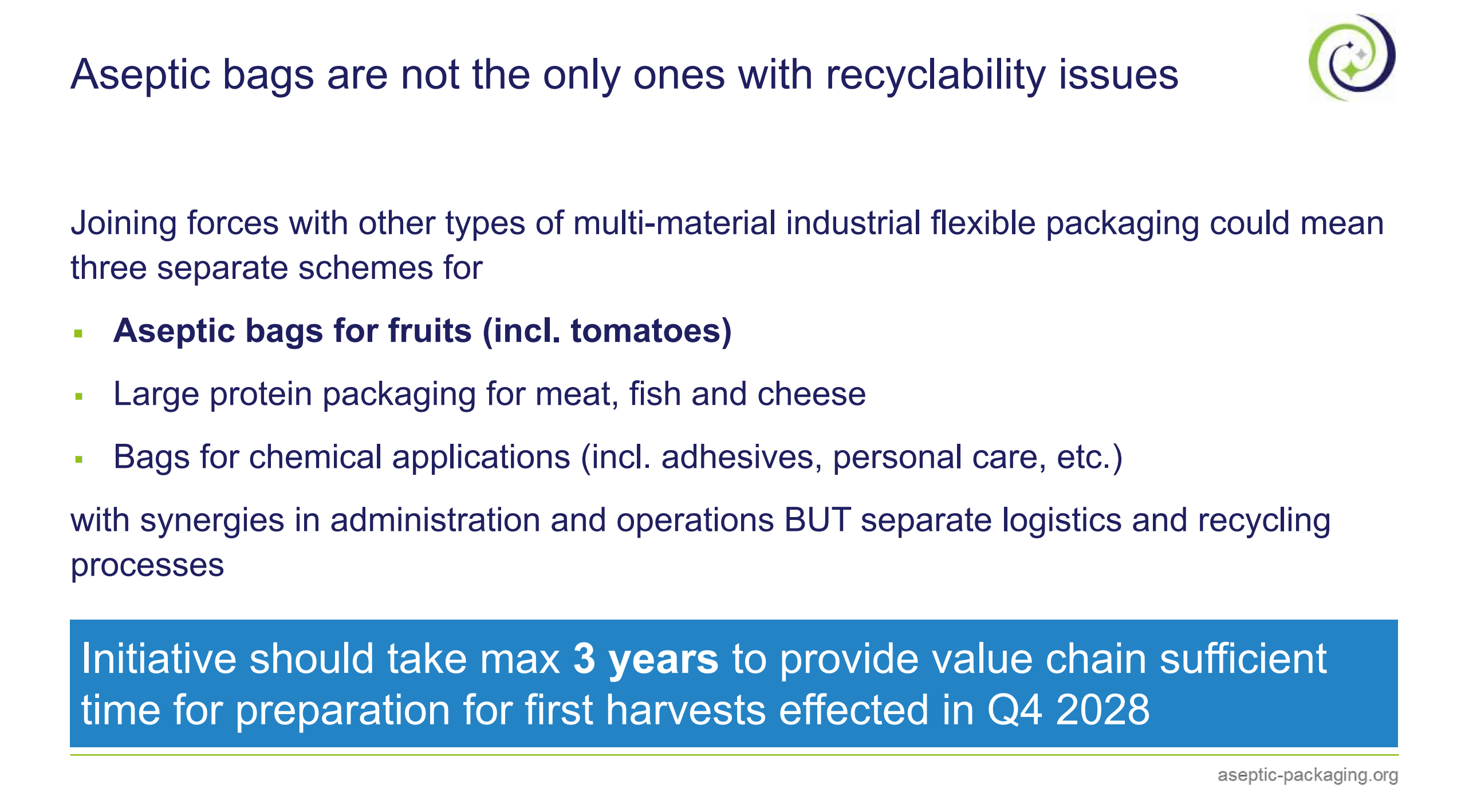

The better way is to fix the sorting and recycling scheme. Since the general waste stream doesn’t work for industrial bags, we at the ABMA are proposing a dedicated initiative to establish our own closed-loop scheme. The beauty of industrial aseptic bags is that they are only used in business-to-business industrial operations. There aren’t hundreds of thousands of ketchup factories across Europe; the number of collection points is very limited and highly controllable.

Our goal is to connect industrial bag users via a dedicated B2B EPR scheme, partnering with national waste organizations to develop our own official recycling guidelines. Because it’s a clean, controlled industrial stream, we are highly confident we can feed this waste into advanced chemical recycling to generate true, food-grade recycled plastics. But we need at least two to three years to complete this project, because the crop harvested in winter 2028/2029 will be the very first one hitting the market after the January 2030 deadline.

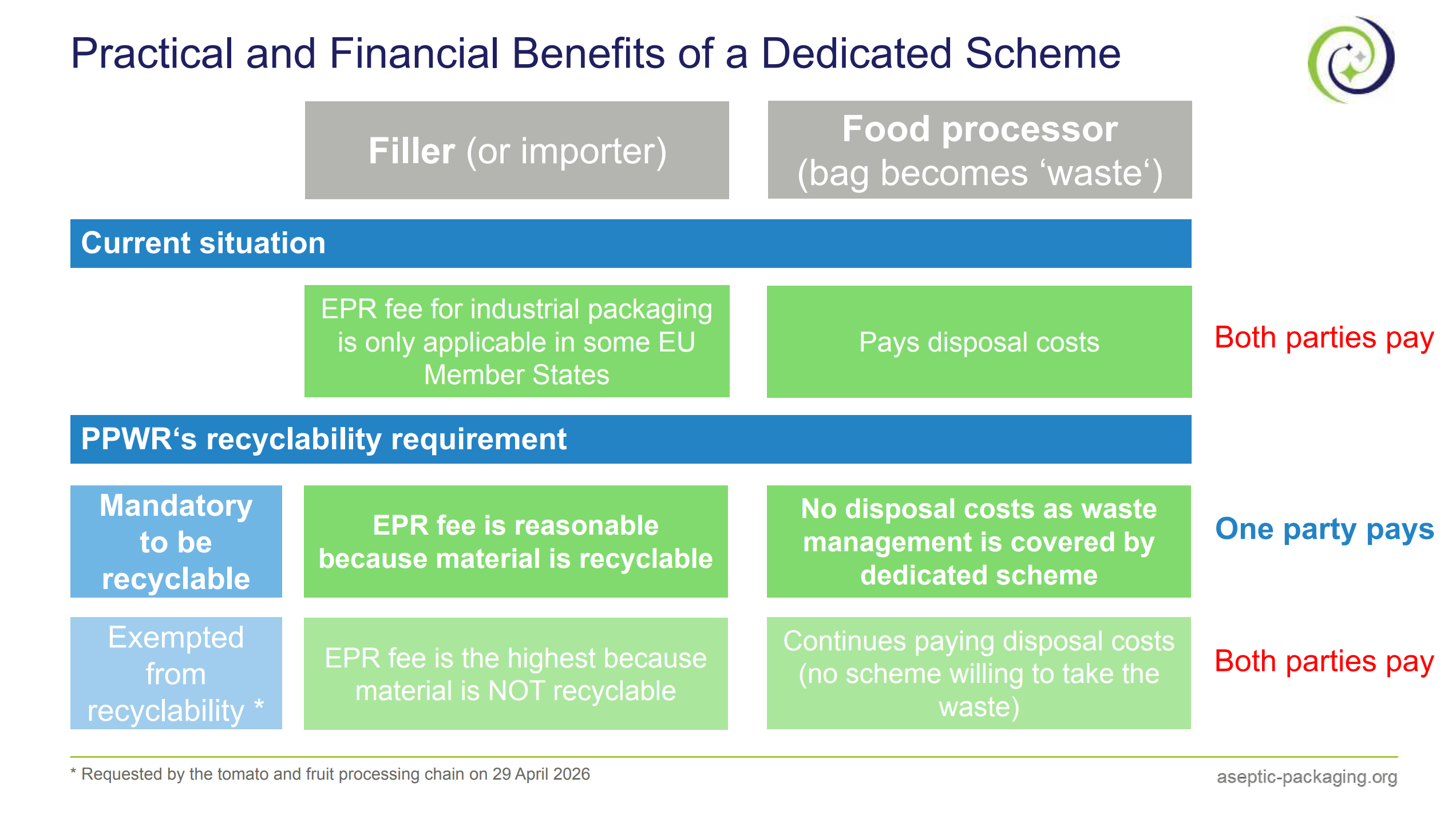

The practical and financial benefits of this dedicated scheme are massive. Today, both the filler and the end-user pay—the filler pays a small B2B fee in some countries, while the end-user pays heavy local disposal costs for a contaminated bag that just gets landfilled or burned.

Under our proposed recyclable scheme, only the filler pays a reasonable, clean EPR fee. Because a dedicated waste management system takes care of it, the customer faces zero disposal costs. When a factory doesn’t have to pay for waste disposal, they become incredibly motivated to separate that waste cleanly at the line. It allows everyone to keep operating exactly as they do now, preserves our vital 24-month shelf life, protects product quality, and removes the frantic R&D pressure to change our filling machines.

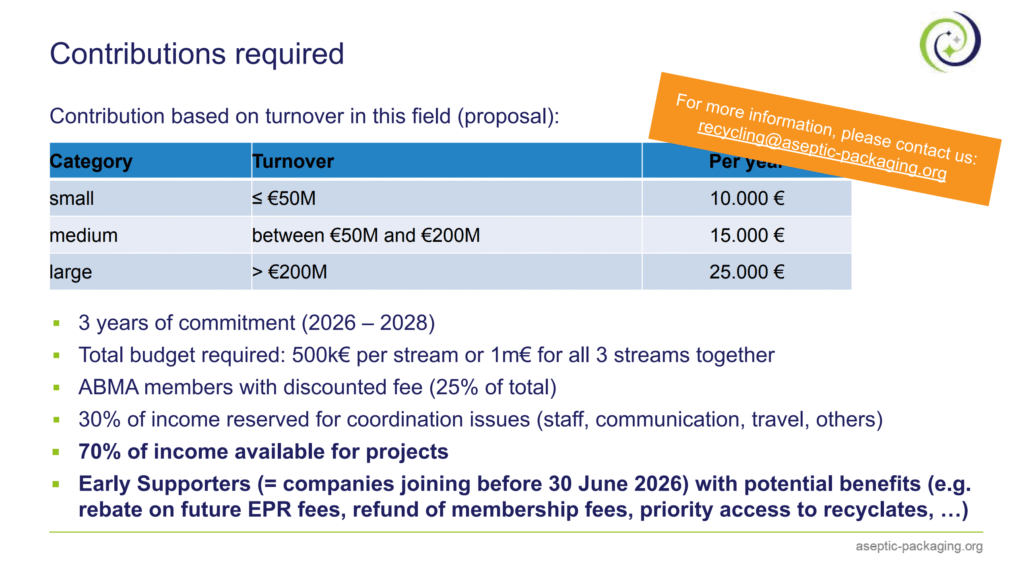

We are asking for a very small financial contribution from the value chain to get this off the ground—ranging from €10,000 to €25,000 a year based on company size—to build this proof of operational concept by 2028. Major players, including the largest ketchup manufacturer in the world, have already signed up because they know it’s the only way to protect their supply chain. This is our license to operate on EU territory, and the rest of the world is watching.

Source: ABMA

{kind=link}